- Moving the markets

The debt ceiling drama is far from over. Even though the two parties have reached a tentative deal, they still need to pass it in Congress by tomorrow. But many lawmakers are not in town, and some Republicans are not on board. This could spell trouble for the compromise bill.

The markets were optimistic at first, but then reality kicked in. Traders realized that the deal is not a done deal, and that the Fed is still looming large. The Fed’s Barkin admitted that inflation is not going away anytime soon, which raised fears of more rate hikes in June.

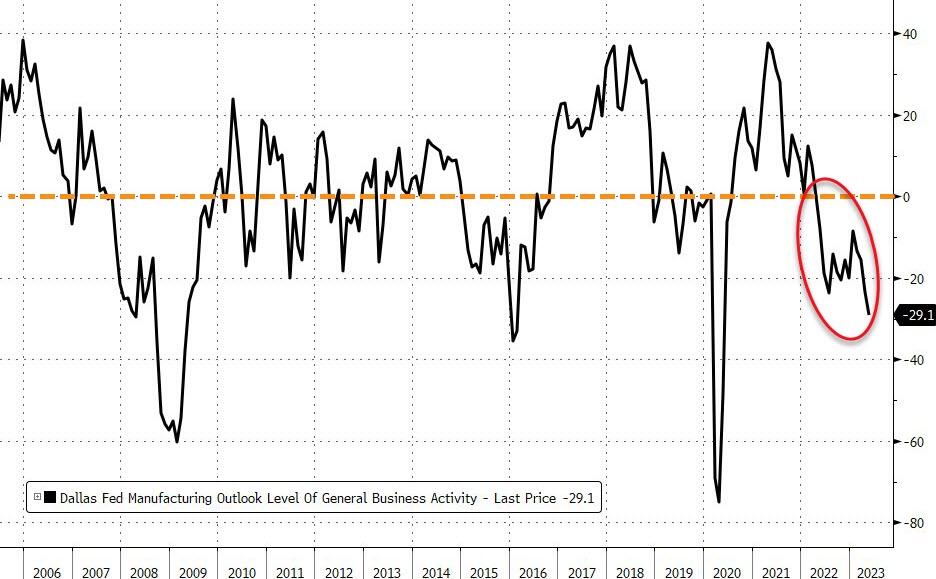

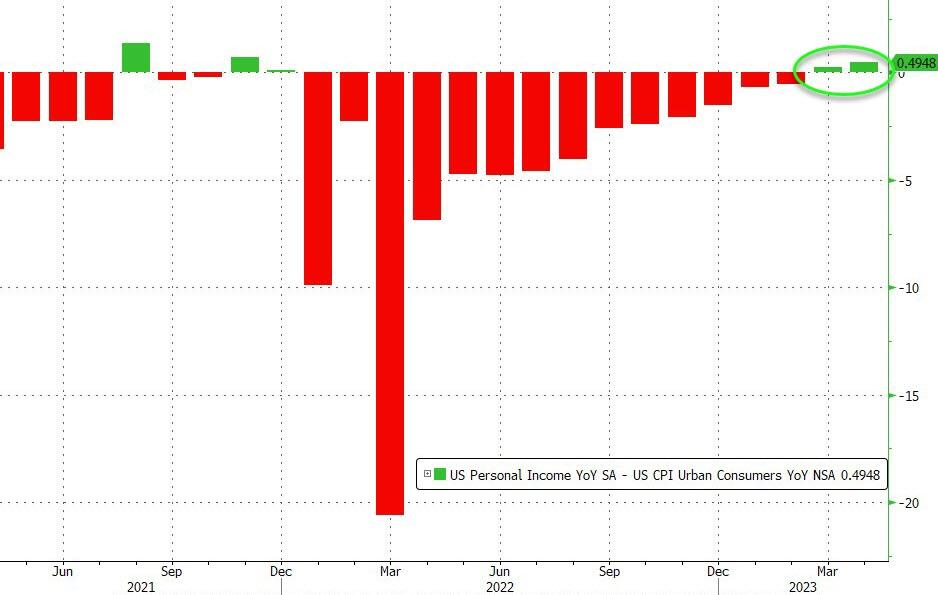

The economic data did not help either. The Dallas Fed Manufacturing Survey shrank for the 13th month in a row, consumer confidence fell to its lowest level since 2022, and home prices dropped for the first time in nine years. These are not signs of a strong economy.

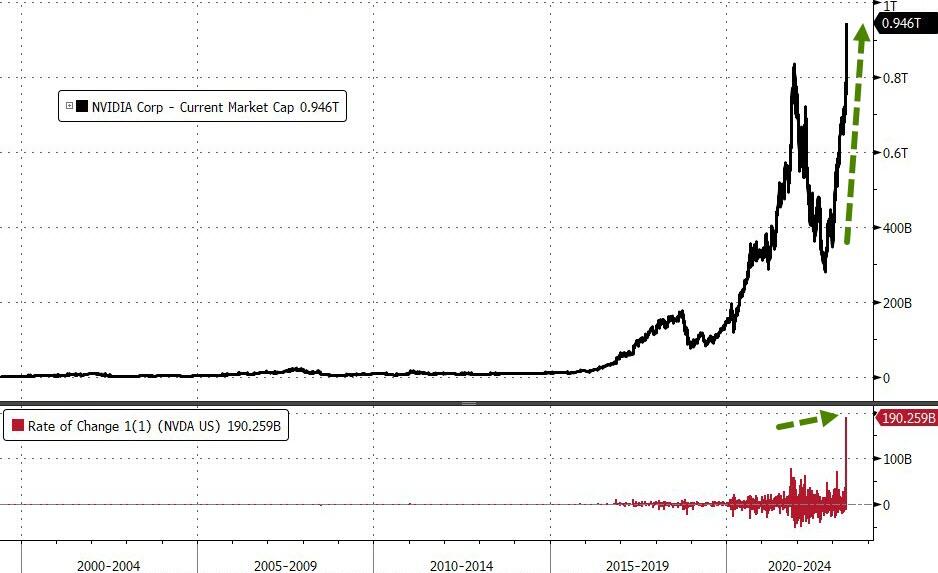

The only bright spot was the tech sector, especially the artificial intelligence (AI) stocks. Nvidia became the seventh company to join the $1 trillion club, thanks to its booming chip business.

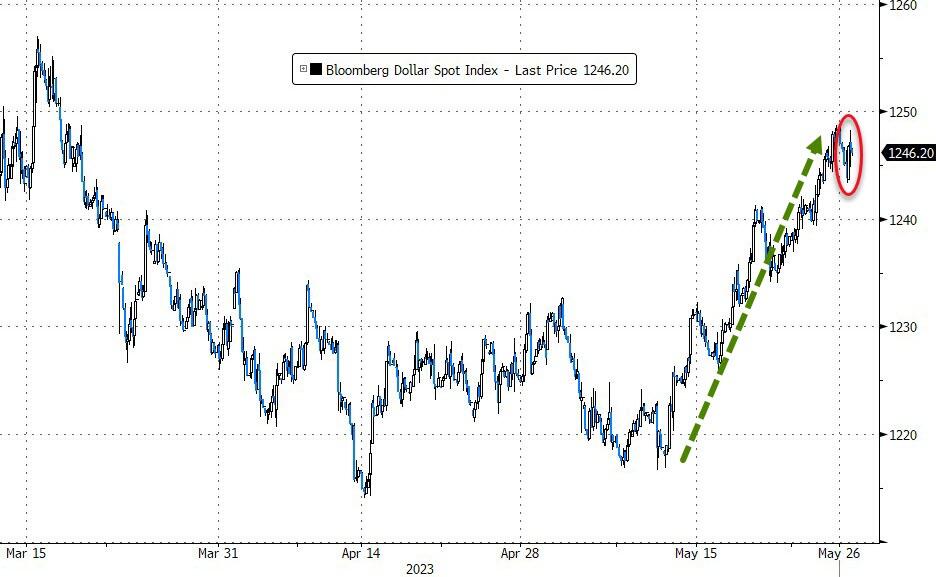

Bond yields fell, while the dollar wobbled. Gold finally got some love.

So, what’s next for the markets? It all depends on whether the debt ceiling deal gets done, and what the Fed does next. All investors should brace for more volatility and uncertainty in the coming days. Stay tuned for more updates.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}