- Moving the markets

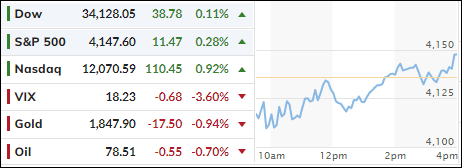

Yesterday’s hotter-than-expected CPI report could not keep the markets under water for any length of time. The same meme was at play today, after a stronger-than-expected retail sales report pushed equities into an early hole.

In an almost repeat performance, the major indexes battled back, reclaimed their unchanged lines and closed moderately in the green, with the Nasdaq scoring a 3-day win streak.

January retail sales rose 3%, which was a lot higher that analysts’ expectations of 1.9%. Traders interpreted that as an economy that is holding up well, despite the Fed’s aggressive rate hike policies.

This latest data point again confirms that the Fed is nowhere near pausing or pivoting its hawkish stance, and their mantra “higher for longer” appears to be the continued path for the remainder of 2023.

Hawkish Fed rate expectations are rising and so are stocks, which seems paradoxical. In other words, the tug-of-war between the Fed’s intention and the markets calling it a bluff continues in full swing. Right now, the markets are winning and, as is often the case, a well-timed short-squeeze gave the bulls a much-needed assist.

{kind=link}

{kind=link}

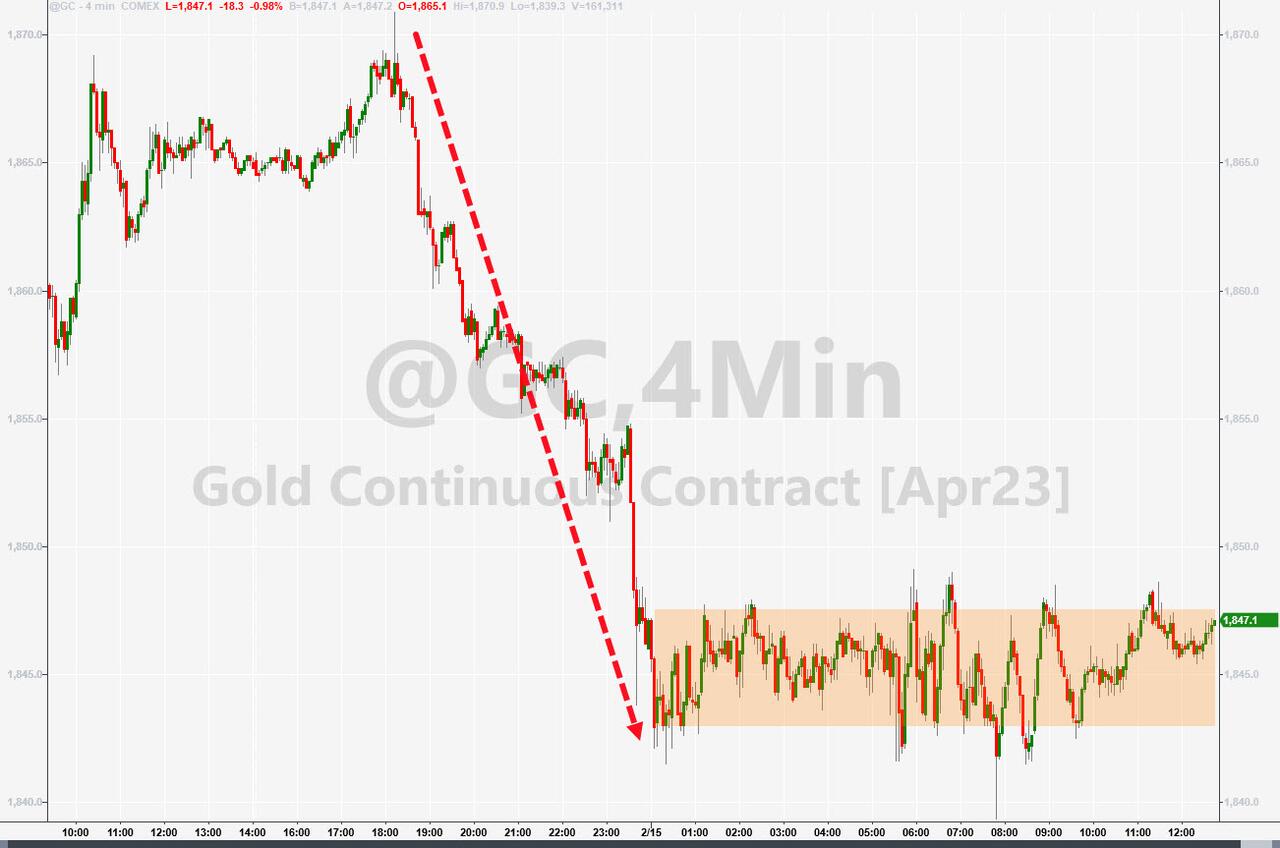

Even rising bond yields were not able to stop bullish sentiment, but they were able to propel the US Dollar higher, which hurt Gold, and the precious metal surrendered 0.9%.

{kind=link}

{kind=link}

{kind=link}

ZeroHedge summed it up succinctly in that stocks simply don’t care about opposing data points due to their long-term outlook:

Higher rates sooner ->>> recession sooner ->>> crash sooner ->>> emergency rate cuts sooner (goal accomplished).

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my most for ETFs selections. However, if you came on board later, you may want to look at the most current version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs again presented mixed results with the Domestic one gaining, while the International one sipped a tad.

This is how we closed 02/15/2023:

Domestic TTI: +8.44% above its M/A (prior close +7.93%)—Buy signal effective 12/1/2022.

International TTI: +9.96% above its M/A (prior close +10.00%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli