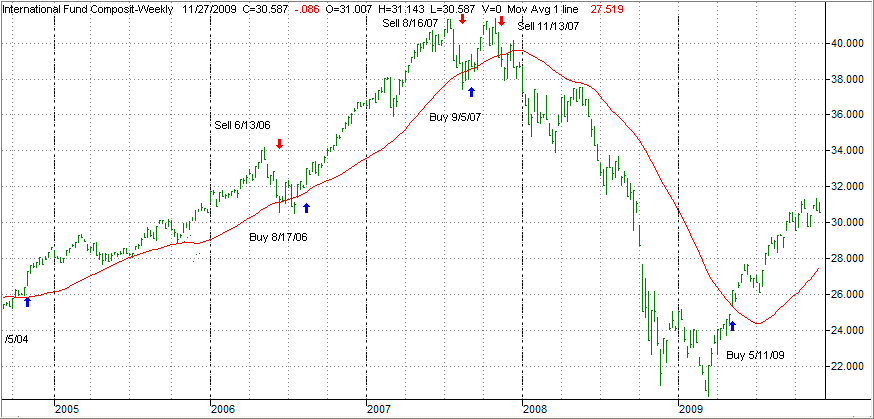

I have talked about the importance of only using ETFS with high volume to be sure that you can enter and exit at a moment’s notice. One reader had this experience:

I have talked about the importance of only using ETFS with high volume to be sure that you can enter and exit at a moment’s notice. One reader had this experience:

I have a comment and question about the Nov.2 column about sell stops.

The comment: I ran into a different kind of problem recently with sell stops. I had bought a relatively low volume ETF (from a sort of tout list, I’m ashamed to say, it looked ok when I researched it– but, since I’m an amateur, I hadn’t realized the volume was low.) So when the sell stop kicked in, I was selling and it seemed nobody was buying, the sell price spiked way down before all of the position was liquidated by the automatic sell request. After this, I divided my sell stop into halves for awhile, but this was tedious so I just tried not to buy into a low volume ETF that I’d never really heard of before.

Q1: Any comments on my problem? What kind of volume would you consider necessary?

Regarding stops:

Q2: I wanted to confirm: Are you suggesting to “utilize” a stop in tracking one’s holdings, but not place it officially until you use it? Or should you actually have it in place at all time officially with your broker?

The reason I like stops is it lowers my stress. I have a tough job and am often on the road where I may not get time to log on every evening. I’ve tried to do more short-term trades but that doesn’t work for me. The stop lets me sleep peacefully.

For the most part, volume tends to increase with the size of an ETF. Generally speaking, you want an ETF with at least $50 million in assets. If you were to place a $100k order, you’d want average daily volume to be at least $2 million—more would be even better.

A real liquid ETF like QQQQ, for example, currently sports a daily average volume (according to Yahoo) of over $4 billion, which represents almost $99 million shares. Buying or selling millions of dollars of holdings in such a liquid environment is no problem at all, as I have found out in the past.

While not every ETF offers such liquidity, many have average volume in excess of $4 million traded every day, which will be sufficient for most investors.

To confirm your second question, I never enter a sell stop ahead of time. I look at my spreadsheet reflecting the day-ending prices and, if a stop has been triggered, only then will I enter my sell order the next day.

Disclosure: We currently have holdings in QQQQ.