In the ever-shifting landscape of the financial markets, the S&P 500 has managed to rip higher, finding stable ground after a tumultuous week. This resurgence was largely fueled by a rebound in tech shares and a de-escalation of tensions in the Middle East, with a notable short squeeze lending major support. As traders cast their gaze forward, the anticipation of major earnings releases hangs in the air, adding to the market’s buoyancy.

{kind=link}

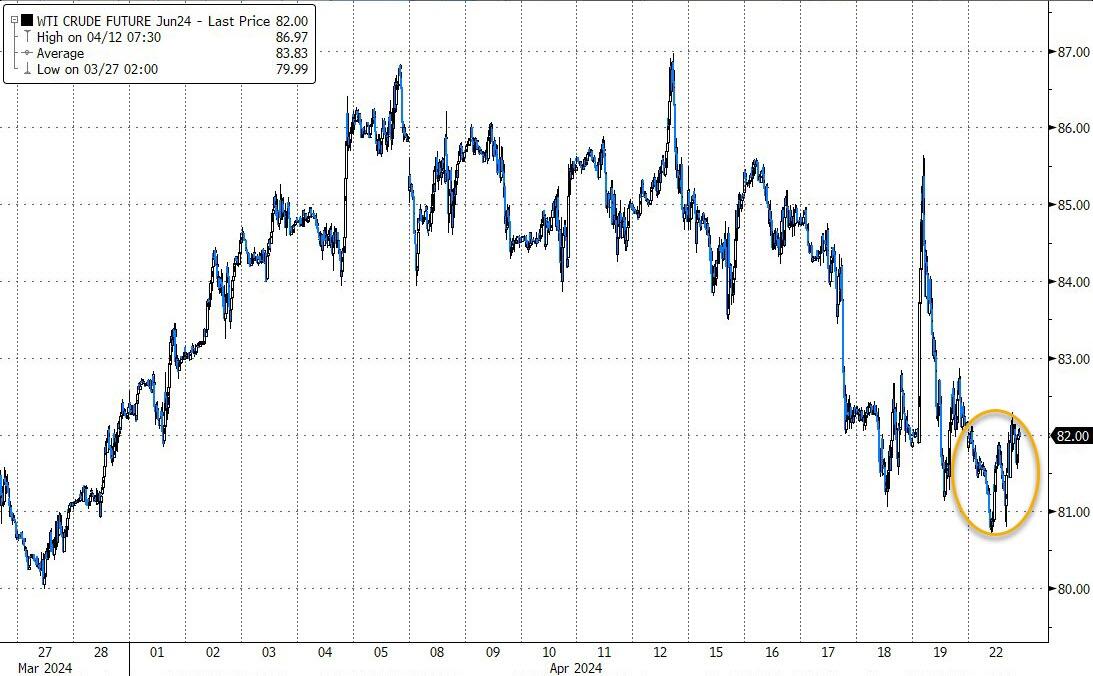

Simultaneously, U.S crude oil experienced a decline of more than 1% following Iran’s announcement that it would not escalate its conflict with Israel. This news brought a sigh of relief to investors who had been bracing for higher oil prices to contribute to inflation, potentially causing the Federal Reserve to pause on rate cuts—a move they are proceeding with regardless.

The market’s upward trajectory is set against the backdrop of a potentially significant week for earnings, particularly with the spotlight on the ‘Magnificent Seven’ tech companies. Nvidia, a favorite in the chipmaker and artificial intelligence sectors, saw over a 2% climb, recovering from last week’s nearly 14% selloff.

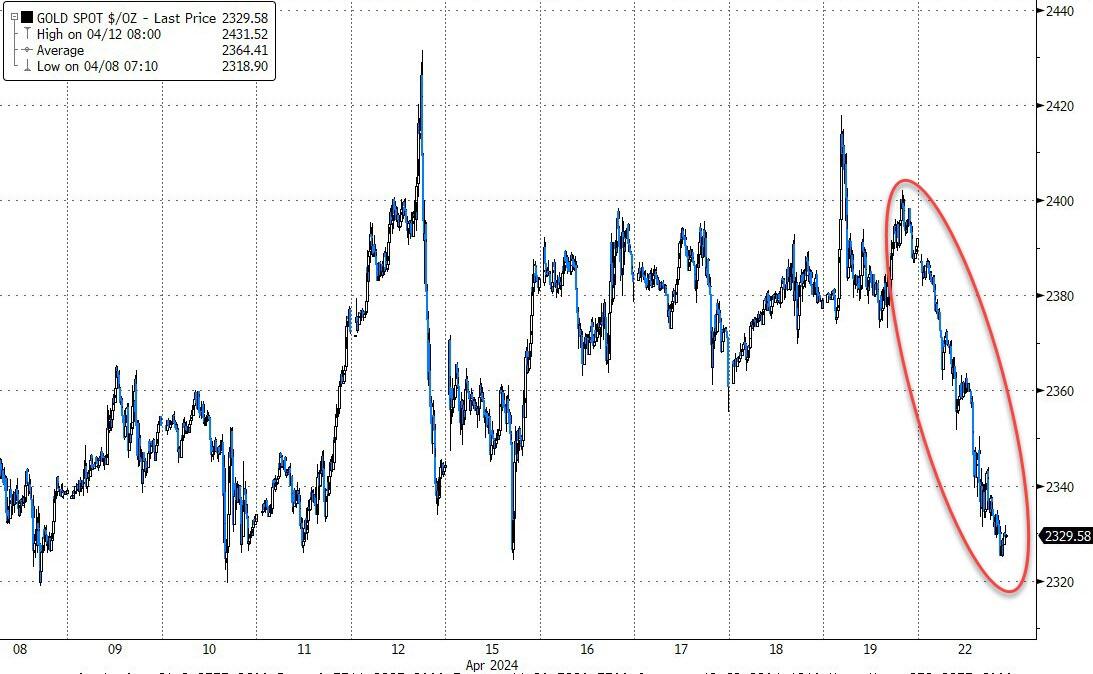

The improved tone in global stock markets can be attributed to two main dynamics: the decline in gold and oil prices, and the steadiness observed in the USD, rather than an increase. The fading concern over a potential regional war in the Middle East has likely contributed to the higher U.S. bond yields observed today.

As the week progresses, some potentially bigger news looms on the horizon. The GDP data due out on Thursday will offer insights into the economic trajectory, while a key inflation reading on Friday could shift perspectives significantly. The Commerce Department is set to report personal consumption expenditures price index data for March, with the PCE deflator being the Fed’s preferred inflation gauge.

In the bond market, yields were mixed with a tendency towards the lower end, as the 5% yield posed major resistance to the 2-year. The dollar experienced its own fluctuations but ultimately closed unchanged. Meanwhile, Bitcoin gained momentum over the weekend, moving towards the $67k mark.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Gold, which had been performing exceptionally well—rising for 13 out of the last 17 days and outperforming the S&P 500 by a considerable margin year-to-date—even after today’s sell-off, was ‘spanked’. Crude oil prices oscillated but ended the day unchanged as headlines of warmongering receded.

{kind=link}

{kind=link}

During these developments, one can’t help but wonder:

Is this period of relative calm merely the precursor to the next financial upheaval?

2. Current “Buy” Cycles (effective 11/21/2023)

Our Trend Tracking Indexes (TTIs) have both crossed their trend lines with enough strength to trigger new “Buy” signals. That means, Tuesday, 11/21/2023, was the official date for these signals.

If you want to follow our strategy, you should first decide how much you want to invest based on your risk tolerance (percentage of allocation). Then, you should check my Thursday StatSheet and Saturday’s “ETFs on the Cutline” report for suitable ETFs to buy.

3. Trend Tracking Indexes (TTIs)

After an initial reversal, today’s optimistic market mood took over, leading to a significant recovery of the major indexes. They experienced their most impressive rally in a month, bolstered by the largest short squeeze during this period.

Our TTIs also participated in the upward movement and ended the day with strong gains.

This is how we closed 4/22/2024:

Domestic TTI: +6.03% above its M/A (prior close +5.21%)—Buy signal effective 11/21/2023.

International TTI: +6.39% above its M/A (prior close +5.48%)—Buy signal effective 11/21/2023.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

—————————————————————-

Contact Ulli