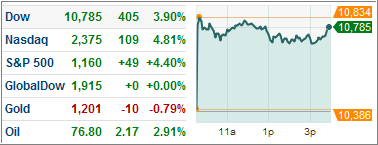

Much has been and more will be written about last Thursday’s market debacle during which at one point the Dow had plunged almost 1,000 points, its worst intra-day point pullback ever.

Much has been and more will be written about last Thursday’s market debacle during which at one point the Dow had plunged almost 1,000 points, its worst intra-day point pullback ever.

With the Greece debt crisis having been the main cause of the turmoil, is there more downside risk and if so, how much? For some views, let’s listen in to “Citi sees up to 20% correction over Greece:”

Just hours after one of the most bruising sessions for Wall Street, strategists in Europe on Friday painted a poor outlook for rebound prospects in the near term.

Citigroup got things off to a bearish start with a prediction that fears of sovereign debt contagion over Greece could trigger a near-term correction of up to 20%.

They said that while there have been financial crises with international implications in the recent past — Northern Europe in 1992, Southeast Asia and South Korea in 1997 — the Greek crisis is “graver than these were.”

Global stock markets have perhaps rallied too far, too fast since the March low of 2009 to the April 2010 high, Tsutomu Fujita, an analyst at Citi, commented.

“With global equities having rallied 79.9% in a scant 13 months through April, we feel it would be only natural to go through a correction of around 10% or 20% over two or three months,” Fujita wrote in a research note.

From the April high to the May 6 low, Japanese stocks are down 4.2%, the U.S. has dropped 7.6%, and Europe has fallen 9.5%.

While Fujita said global stocks should resume their “upward trajectory in June,” the period in between could be dicey.

…

Although a trading error is being blamed for the dramatic falls, anxiety about Europe gets much of the blame for the loss of investor confidence that erupted on Thursday.

And plenty of criticism was being fired at Europe’s central bank president, Jean-Claude Trichet, who missed a vital opportunity on Thursday to calm market nerves at the Lisbon central bank meeting.

…

“Most markets expected Trichet to come out and calm down markets yesterday. He didn’t say anything…what politicians are so afraid of among the euro zone is to say countries in trouble need to bite the bullet, there is no other way around it,” said Hellerup, Denmark -based Blaabjerg.

“They can’t continue to bail everyone out. You just move money from one balance sheet to another…that is simply not a solution, and markets realize this.”

Hellerup parts ways with the Citi view of markets reversing by 10% to 20%, at least with regards to the S&P; 500, where he sees maybe a 5% pullback, but the level won’t dip below 1,110 he predicts.

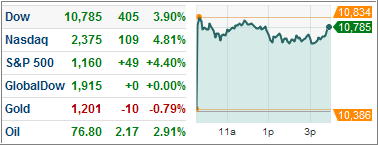

Well, as of Friday, we closed at the 1,111 level and barring a huge rebound on Monday, we may very well sink below that number quickly.

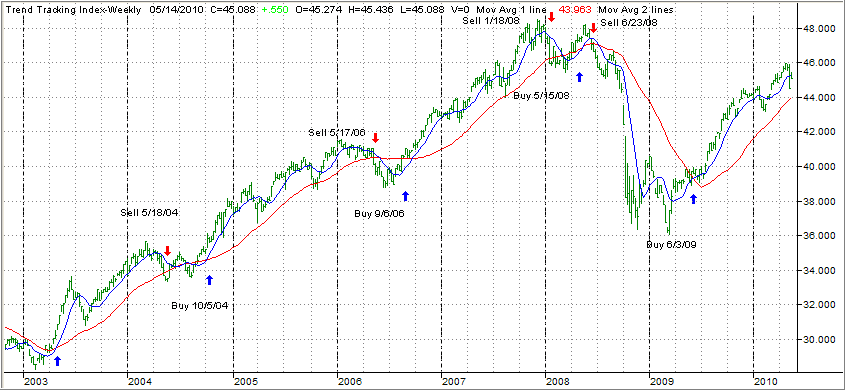

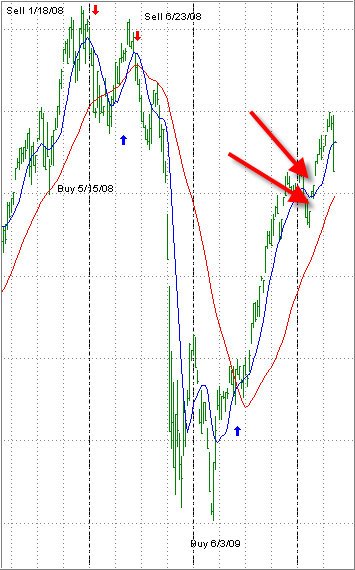

As you know from my writings, I don’t think much of most forecasts, but I do read and occasionally share some of them to see how others interpret current events. To me, after last year’s rally, the risk of a sharp downside correction has clearly increased.

We may have seen all of it last week, or just the beginning. If our domestic TTI remains above its trend line, I can see this pullback being of a more a modest nature. If we break below the line, we will have officially entered bear market territory again, at least according to my definition.

Fundamentally, the ball is still in the court of the Europeans, who have shown anything but a unified front and leadership during the Greek crisis. If there is more useless jawboning and lack of coordinated action to solve the issues at hand, the markets will not like this uncertainty and more sell offs are a possibility.

The potential spillover effect into the other Club Med countries has been well documented and if the Eurozone as a whole, being a major trading partner to the rest of the world, slips back into a recession, all economies and stock markets will suffer.

It’s too early to tell how this will play out, but with last week’s action, I am glad that we have lightened up on our positions, which will enable us to better whether out the current uncertainties.

{kind=link}