- Moving the market

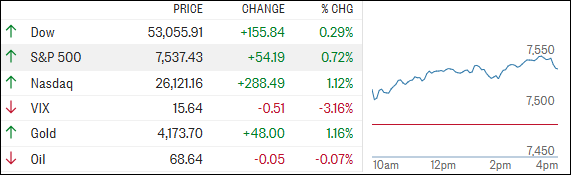

The S&P 500 and Nasdaq kept their positive momentum going early in the week, building on the strong gains posted during the previous week as technology stocks continued to attract buyers.

Interestingly, those advances came even as semiconductor stocks—the market’s leadership group for much of the year—remained under pressure.

Traders continued to trim positions in chipmakers and rotate into other areas of the market. The VanEck Semiconductor ETF (SMH) fell 3.2%, marking its second consecutive weekly decline.

That rotation may actually be a healthy development for the broader market. Financials, Healthcare, and Industrials all closed the week at fresh all-time highs, more than compensating for the recent consolidation in semiconductor stocks.

While the weakness in semis appears to be a short-term headwind, it has done little to derail the broader market’s advance.

Traders will also be paying close attention to the Federal Reserve this week, with minutes from the June meeting—the first chaired by Kevin Warsh—scheduled for release on Wednesday. Any clues about the future path of interest rates could influence market sentiment.

By day’s end, the major indexes delivered another impressive performance. The Dow shook off an early selloff and rallied to a new record high, surpassing the 53,000 mark for the first time.

Elsewhere, crude oil was little changed as shipping traffic through the Strait of Hormuz continued to recover, although volumes remain below historical norms.

{kind=link}

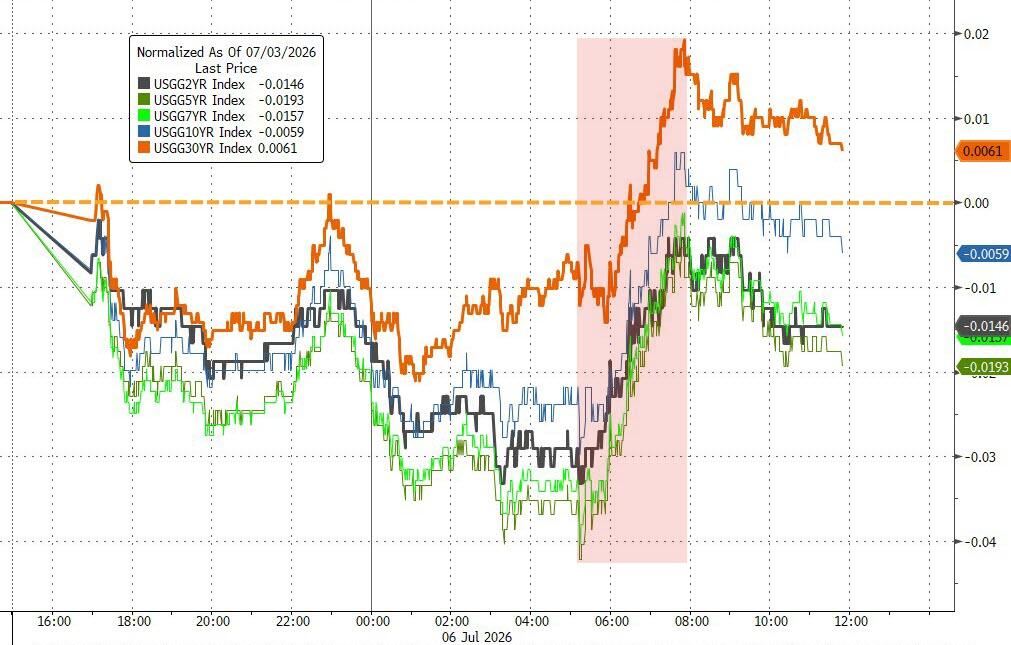

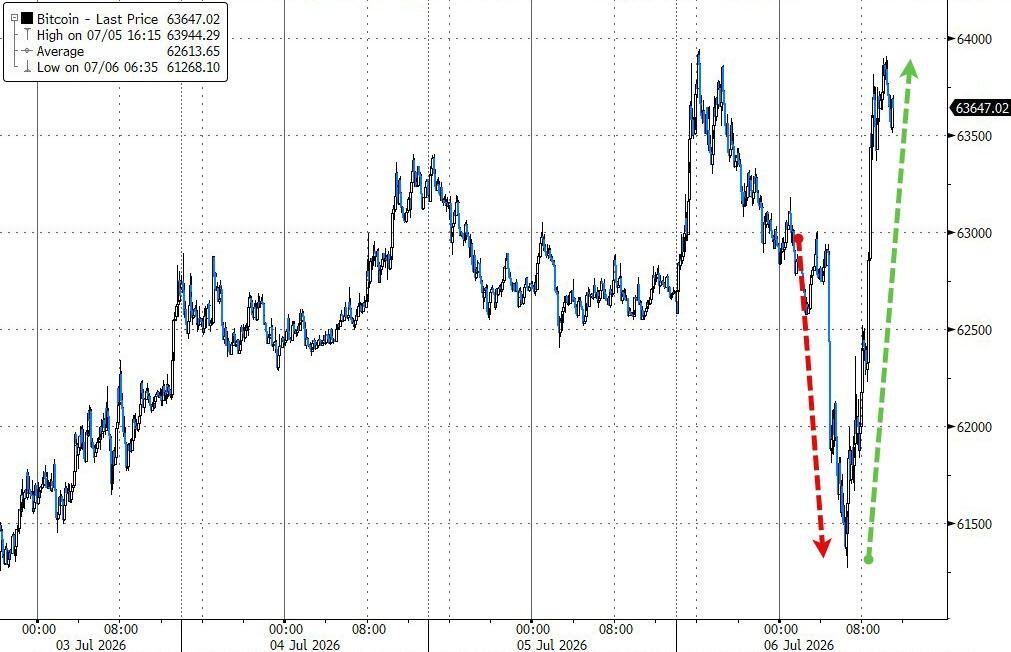

Bond yields finished mixed, and the dollar was essentially unchanged. Gold continued its climb toward the $4,200 level, while bitcoin rebounded sharply from an early dip after receiving a boost from President Trump’s renewed support for cryptocurrencies.

{kind=link}

{kind=link}

{kind=link}

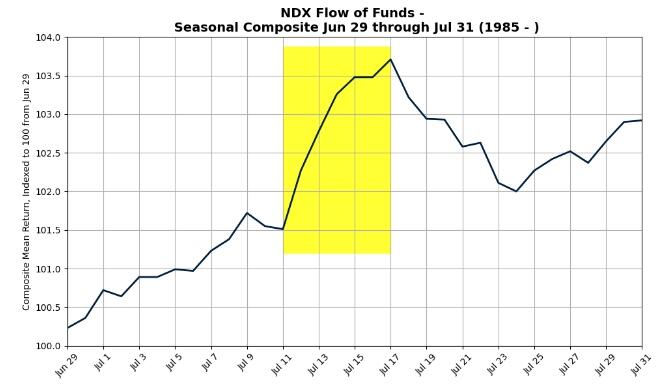

Historically, the market is entering one of its strongest seasonal periods of the year. The big question, however, is whether this year’s rally still has enough fuel left to follow the usual seasonal script—or will we be in for a surprise?

{kind=link}

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Despite a sluggish start, the Dow eventually joined the other major indexes in posting a strong rebound.

Technology stocks led the charge, but gains were also seen in precious metals and, even more notably, bitcoin.

Our TTIs trailed the broader market but still managed to move higher. The International TTI showed greater strength, outperforming its domestic counterpart.

This is how we closed 07/06/2026:

Domestic TTI: +9.39% above its M/A (prior close +9.35%)—Buy signal effective 5/20/25.

International TTI: +7.94% above its M/A (prior close +7.07%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli