- Moving the market

The S&P 500 was pretty flat early on, as traders took a breather after hitting fresh all-time highs and kept an eye on the latest headlines around U.S.–Iran tensions—along with the usual moves in big tech.

Tech itself was a bit mixed. Alphabet slipped about 1%, but Nvidia helped pick up the slack, climbing 1% and keeping the sector from sliding.

The real standout, though, was Hewlett Packard Enterprise, which surged 26% after delivering a strong outlook and raising full-year guidance well above expectations.

Looking back, Monday’s record highs were largely driven by Nvidia and the ongoing enthusiasm around the AI trade. It’s been an incredible run for equities lately—fast and powerful.

Of course, those kinds of moves can sometimes unwind just as quickly, but for now, traders aren’t seeing red flags from their overbought/oversold indicators.

On the economic front, job openings jumped, giving the Macro Surprise index a boost, while the number of people quitting their jobs dropped sharply.

{kind=link}

Add in generally upbeat earnings, and that helped keep the market in positive territory—even as headlines about a potential U.S.–Iran deal remained mixed.

That said, there were a few signs under the surface worth noting. The S&P 500 didn’t quite confirm moves in crude oil or bond yields, small caps actually outperformed, and overall market breadth stayed weak—which can sometimes hint at a less healthy rally.

{kind=link}

{kind=link}

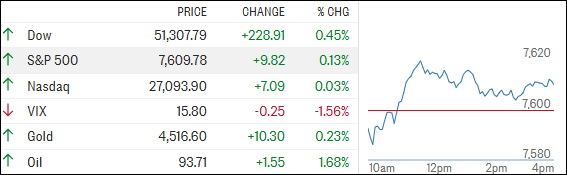

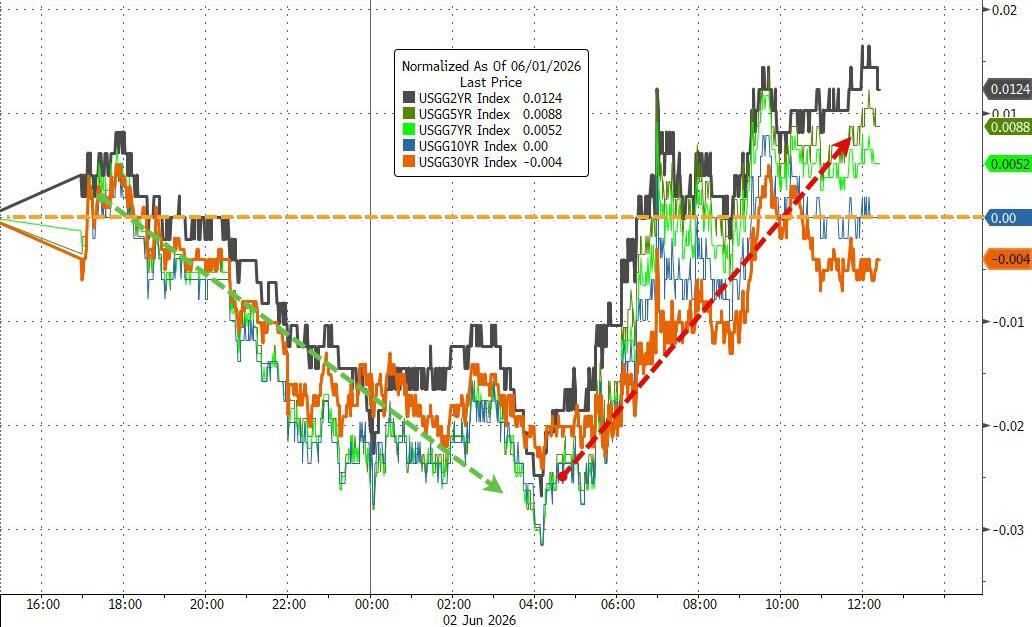

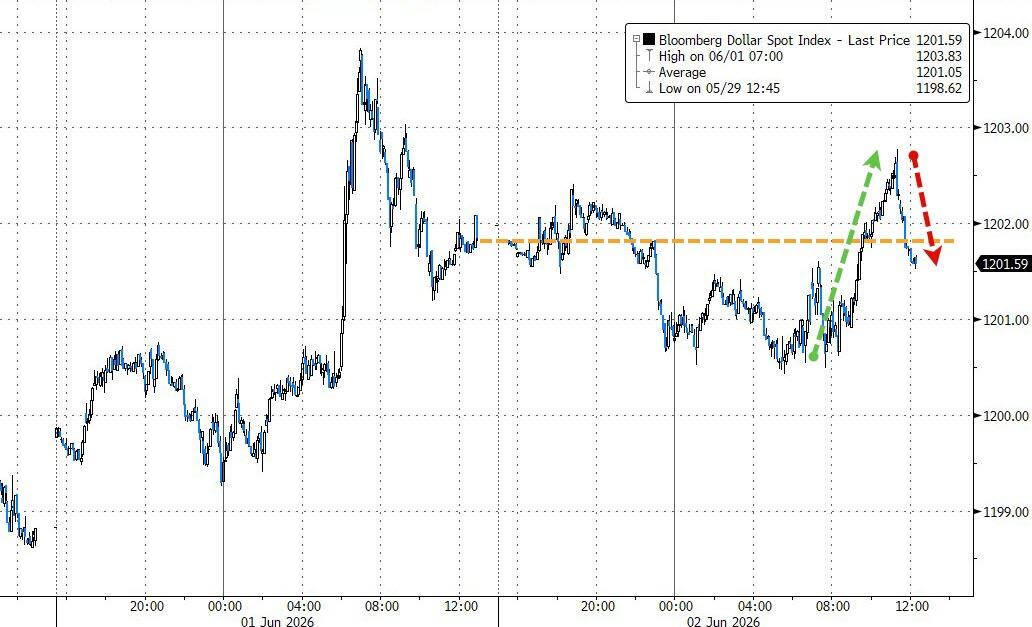

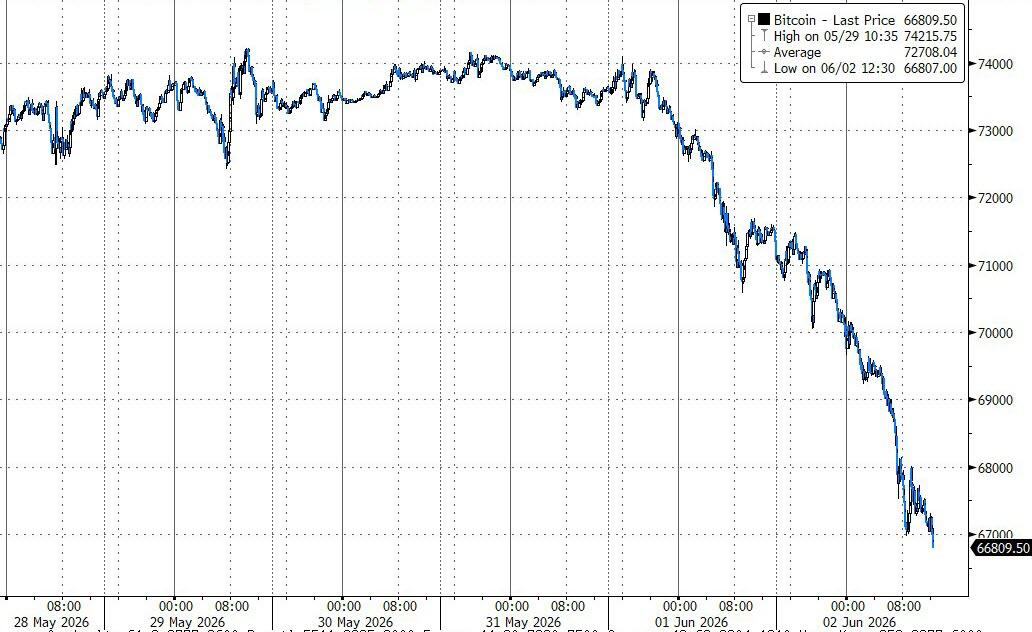

Elsewhere, bond yields were mixed, the dollar edged a bit lower, and gold gave back its overnight gains but still managed to finish slightly higher. Bitcoin, meanwhile, lost momentum and tested the $66K level, hitting two-month lows.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Oil has been especially volatile, swinging on uncertainty around the ceasefire and concerns over shipping through the Strait of Hormuz. Prices had dropped last month on hopes for a deal, but the outlook now feels a lot less clear.

Adding to the confusion, recent comments from Trump and Israeli Prime Minister Netanyahu didn’t exactly line up, leaving traders with more questions than answers.

With all this crosscurrent of strong momentum, weak breadth, and geopolitical uncertainty—how long can the market keep pushing higher without a clearer direction?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The markets bounced back nicely after a soft start, with the major indexes holding their ground and squeezing out another modest gain by the close.

Metals were a bit mixed overall, but copper stood out, showing the most strength as the session wrapped up.

Meanwhile, our TTIs moved higher and continue to hold firmly above their trend lines, reinforcing their positive momentum.

This is how we closed 06/02/2026:

Domestic TTI: +8.14% above its M/A (prior close +7.71%)—Buy signal effective 5/20/25.

International TTI: +10.47% above its M/A (prior close +9.84%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli