- Moving the market

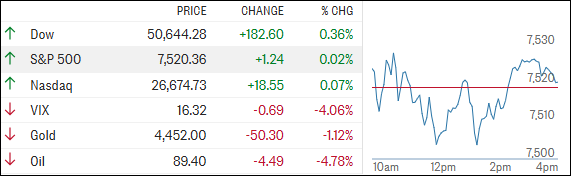

The Dow came out of the gate strong today, jumping nearly 300 points and even tagging a fresh record high early on.

A big help came from falling oil prices—down almost 5%—and a solid bounce in Procter & Gamble, which climbed more than 3% and helped lift the index.

Micron kept its momentum going too. After its massive 19% surge yesterday, that pushed it past the $1 trillion mark, the stock added another 4% today. That rally was fueled by a bullish UBS call suggesting Micron could have a lot more upside, thanks to long-term deals tied to the ongoing AI boom.

Lately, traders seem to be gravitating toward memory chip names as their preferred way to play AI.

On the macro front, traders found some encouragement in comments from President Trump, who said talks with Iran to end the conflict were “proceeding nicely.” That optimism, combined with a strong earnings season, has helped drive stocks higher this month.

That said, not everyone is convinced there’s much gas left in the tank. One strategist is calling for only a modest move higher in the S&P 500—around 2% by year-end—citing concerns over rising bond yields and inflation expectations.

Others are more optimistic, pointing to continued earnings strength and even floating targets as high as 8,000 for the index.

By the close, most of the early excitement had faded. The major indexes finished mostly flat, though the Dow did manage to hold on to a modest gain.

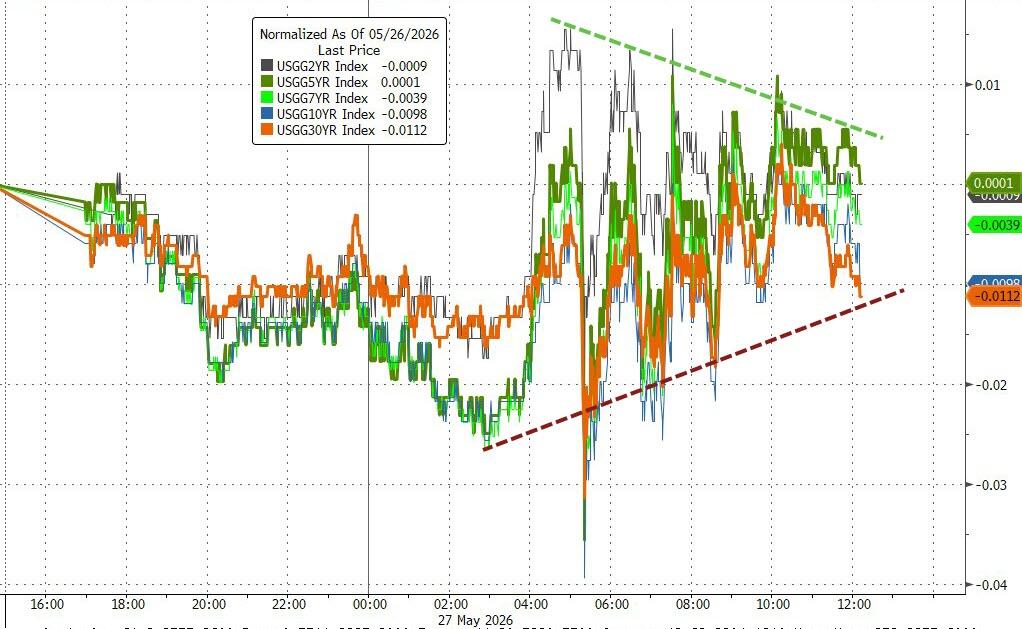

Bond yields ended little changed after initially rising, as reports suggested Iran peace talks might not be going as smoothly as hoped.

{kind=link}

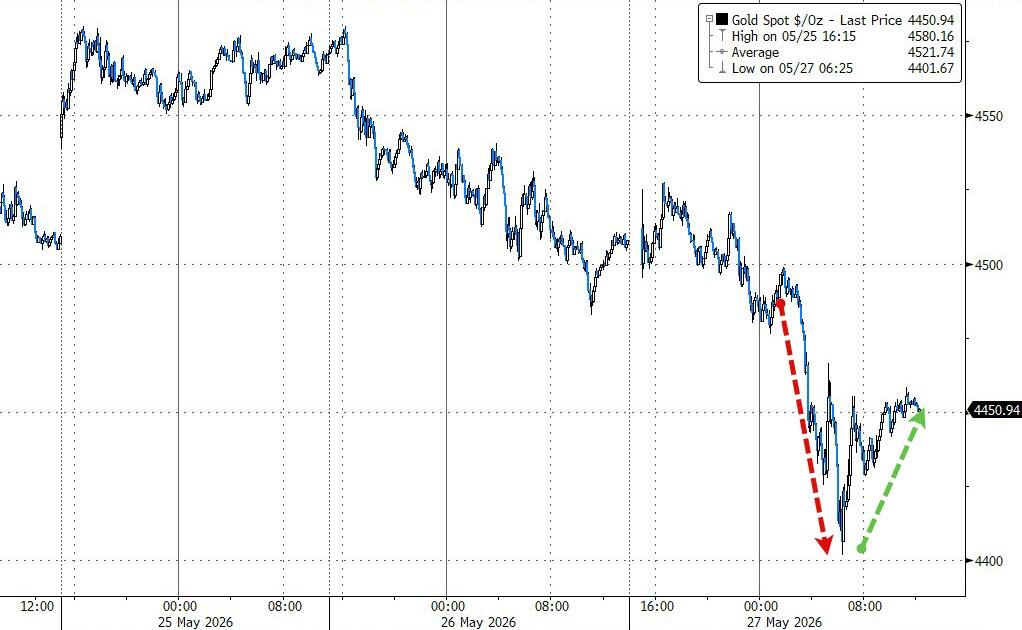

Elsewhere, the dollar spiked, gold briefly lost the $4,500 level before bouncing off $4,400, and Bitcoin extended its recent slide.

{kind=link}

{kind=link}

{kind=link}

All in all, uncertainty was the main theme of the day, with mixed signals and ongoing geopolitical chatter leaving markets searching for a clear sense of direction.

So, the question is—are we just pausing before the next leg higher, or starting to run out of steam?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The Dow managed to hang on to some of its early, modest gains, but the rest of the market didn’t do much of anything.

Overall, it felt like everything was just treading water as investors dealt with ongoing uncertainty.

Even metals and Bitcoin were stuck in the same holding pattern. The only real standout was the Value ETF (VLUE), which slightly outperformed the Dow and managed to post a decent gain.

Our TTIs were just as quiet—no meaningful movement in either direction, leaving the broader market trend essentially unchanged.

This is how we closed 05/27/2026:

Domestic TTI: +7.15% above its M/A (prior close +7.22%)—Buy signal effective 5/20/25.

International TTI: +9.77% above its M/A (prior close +10.02%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli