[Chart courtesy of MarketWatch.com]

- Moving the markets

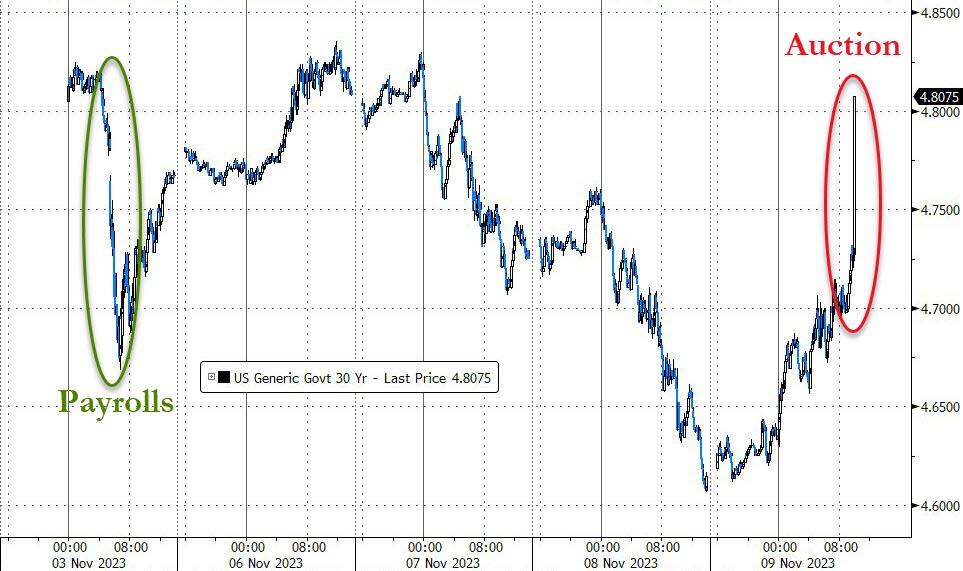

It was a bad day for the S&P 500, as the bond market threw a tantrum and spoiled the party. The trigger was a disastrous 30-year bond auction, which saw foreign buyers flee. This was not the first time this year that the bond market was disappointed, but it was the worst. Stocks and bonds both got clobbered.

{kind=link}

{kind=link}

{kind=link}

Fed chair Jerome Powell tried to calm the nerves, saying that inflation was slowing down, and more work was needed to tame it. But then he added this zinger:

{kind=link}

We are not sure if we have tightened the monetary policy enough to bring inflation down to 2 percent in the long run.

That did not help.

Regional banks tanked, as the dollar soared, and money dried up. I wonder what the Fed and the Treasury will do about this mess.

{kind=link}

{kind=link}

{kind=link}

Thorstein Polleit from the Mises Institute had this to say:

Investors are finally waking up to the huge debt problem in the US, which they have ignored for too long: The US government owes more than thirty-three trillion US dollars, which is about 123 percent of the US economy.

And it is only getting worse: by 2030, the debt could reach fifty trillion US dollars. The usual suspects who used to buy US debt—like Japan, China, Brazil, Russia, and Saudi Arabia—are not interested anymore. Who will fund the US government’s spending spree of 6 percent of the economy every year?

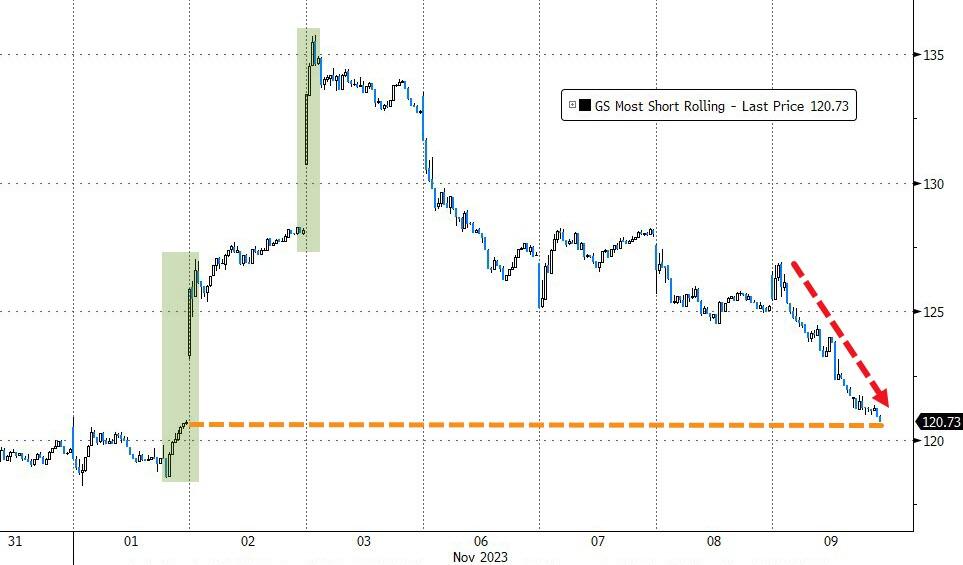

The most hated stocks also got smashed, as the bulls ran for the hills, while the 30-year yield had its biggest spike since the pandemic, and the 2-year yield breezed past 5 percent again.

{kind=link}

{kind=link}

{kind=link}

Gold was the only winner, as it rose despite the stronger dollar and higher bond yields. Is that a warning that things are about to get worse?

{kind=link}

2. “Buy” Cycle (12/1/22 to 9/21/2023)

The current Domestic Buy cycle began on December 1, 2022, and concluded on September 21, 2023, at which time we liquidated our holdings in “broadly diversified domestic ETFs and mutual funds”.

Our International TTI has now dipped firmly below its long-term trend line, thereby signaling the end of its current Buy cycle effective 10/3/23.

We have kept some selected sector funds. To make informed investment decisions based on your risk tolerance, you can refer to my Thursday StatSheet and Saturday’s “ETFs on the Cutline” report.

Considering the current turbulent times, it is prudent for conservative investors to remain in money market funds—not bond funds—on the sidelines.

3. Trend Tracking Indexes (TTIs)

The major indexes started the day flat, but soon plunged into negative territory. The reason was a sharp rise in bond yields, triggered by a dismal 30-year auction, that dampened the mood of traders and gave the bears a reason to celebrate.

Our TTIs also fell and remain below their trend lines, indicating a bearish market.

This is how we closed 11/09/2023:

Domestic TTI: -3.64% below its M/A (prior close -2.81%)—Sell signal effective 9/22/2023.

International TTI: -0.82% below its M/A (prior close -0.47%)—Sell signal effective 10/3/2023.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli