With no expectations of a rate-hike last week, and traders rapidly giving up on The Fed’s dream of a steadily higher rate trajectory, a funny thing happened in the markets…

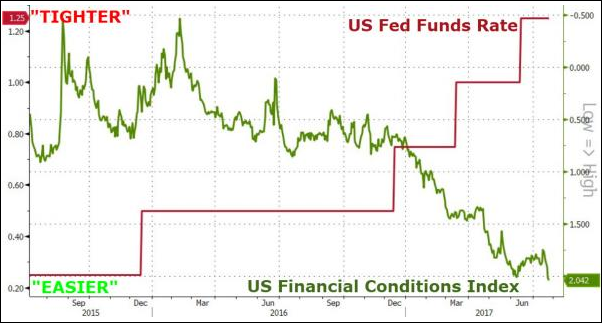

In the eyes of The Fed, their monetary policy has not been this ‘tight’ since October 2008.

However, in the eyes of the market, financial conditions just hit their easiest level in history (easier than the September 2005 previous record easiness level).

This is what happens when you constantly flip-flop, constantly miss forecasts, and constantly lie.

Simply put, this is the death cross of Federal Reserve Credibility.

Picking up on the dramatic divergence, Bloomberg’s Cameron ‘MacroMan’ Crise has some advice for The Fed “Throw Us A Little Vol Here Please!”

Wednesday sees the latest installment of the Fed laying the groundwork for a shift in its balance sheet policy, probably in September. Although the Fed continues to miss its arbitrarily defined inflation target, the Bloomberg financial conditions index is now at easiest level in a decade. That era ended rather badly, and the Fed would do well to inject a little volatility into proceedings before the market does it for them.

The Fed’s halting journey toward balance sheet normalization makes Odysseus’s trip home seem like a speedy jaunt on the hyperloop in comparison. A desire to avoid shaking up the Treasury market appears to be driving this deliberate approach. An apparently heightened concern over low inflation figures has spurred the latest easing in U.S. financial conditions as the market assumes that the Fed will do much less tightening than envisaged by the dot plot. We’re now at the easiest level of financial conditions since May 2007. There is nothing wrong a priori with easy conditions and low volatility. However, the degree to which conditions have eased even as the Fed has normalized policy is unprecedented. R* says that policy rates are close to neutral. Financial markets are saying that they are very easy indeed.

The transmission mechanism of monetary policy is such that the Fed and other central banks have a lot more direct influence over financial markets than they do over inflation.

The last two economic growth cycles ended as a result of malinvestment gone awry. Overly easy policy was at least partially to blame in both instances.

As discussed earlier, low volatility tends to cluster and feed on itself. Barring a shock or other catalyst, it can continue for longer than is sensible.

The Fed has two choices: a little volatility now (via a controlled experiment to keep normalizing policy despite tepid inflation) or a lot of volatility later (when the current regime goes awry, as all economic and market cycles eventually do).

For the long-term health of both the economy and the market, let’s hope they eventually choose the first of these two options.

We suspect they won’t.

Contact Ulli