ETF/No Load Fund Tracker Newsletter For Friday, April 5, 2013

ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

https://theetfbully.com/2013/04/weekly-statsheet-for-the-etfno-load-fund-tracker-newsletter-updated-through-04042013/

————————————————————

Market Commentary

Friday, April 5, 2013

SUBPAR JOBS REPORT PUNISHES US INDEXES; EUROPEAN STOCKS TRACK LOWER

US index ETFs slumped Friday, capping the biggest weekly decline for the S&P 500 Index, after a government report showed less than half of estimated Americans found jobs in March. Though the wheels didn’t fall of the economy as one month doesn’t make a trend, expectations were certainly tempered as investors became concerned about the pace of the economy’s recovery.

Payrolls rose by 88,000 in March, the smallest in nine months, following an upwardly revised gain of 268,000 in February. Economists had projected an advance of 190,000.

The unemployment rate dropped to a four-year low of 7.6 percent from 7.7 percent in the previous month. However, that was hardly any consolation as 500,000 discouraged workers dropped out of the labor force. The labor force participation rate, a gauge that tracks the number of people employed or looking for jobs, slipped to 63.3 percent, the lowest since May 1979.

After sinking 171 points, the Dow Jones Industrial Average (DJIA) reclaimed most of its losses to end at 14,565, down 0.3 percent on the day and 0.1 percent for the week.

The day’s sell-off was broad-based with 18 of the blue-chip index’s 30 components ending in the red.

The S&P 500 Index (SPX) shed 7 points to 1,553 with technology companies fronting the losses and utilities faring the best among its 10 business groups. The benchmark index is down 1 percent for the week, its biggest decline since December.

Treasury prices surged, pushing 10-year note yields to the lowest level in almost four months after the sorely disappointing jobs report spurred speculation the world’s largest economy is slowing.

The US dollar eased up against most of its major trading peers Friday as the surprisingly weak jobs report raised hopes the Federal Reserve will not taper its assets purchase program anytime soon.

European stock markets posted their biggest weekly decline since late October as US March employment data fell well short of expectations, while the European Central Bank said downside risks remain to the region’s recovery.

The Stoxx Europe 600 index tripped 1.6 percent, the lowest in more than one month. With this week’s decline, the benchmark index completed its longest string of losses in 10 months and pared the gauge’s advance so far this year to 2.7 percent.

The DAX 30 index fell 2 percent in Frankfurt, sending it lower by 1.8 percent for the week.

The CAC 40 index slipped 1.7 percent in Paris, capping the weekly loss at 1.8 percent while the FTSE 100 index trimmed 1.5 percent in London.

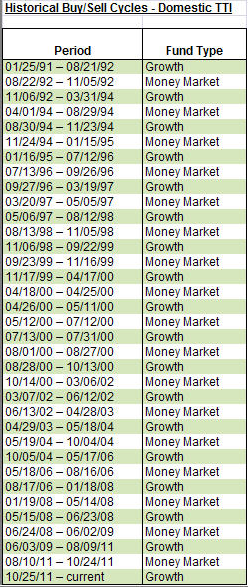

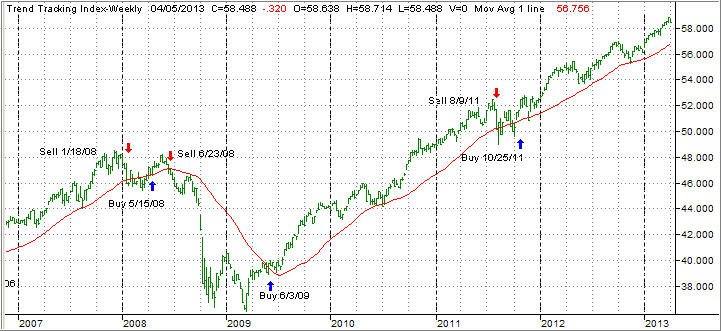

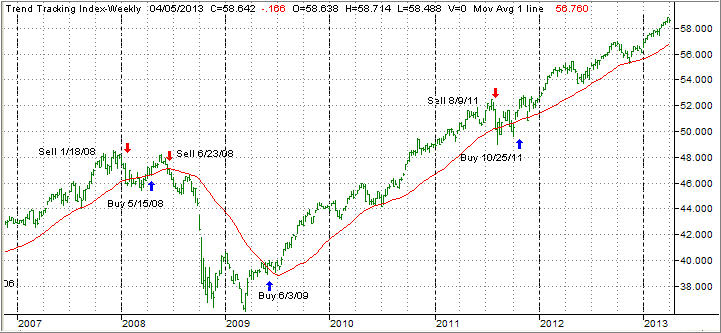

Our Trend Tracking Indexes (TTIs) headed south as well, but remain on the bullish side of their respective trend lines.

Again, as I have repeatedly posted, the international TTI has been slipping sharply and, as is no surprise, I do not recommend any holdings in Europe given their political disarray and worsening economic data points.

For the week, the TTIs ended as follows:

Domestic TTI: +3.16% (last week +3.96%)

International TTI: +5.93% (last week +8.13%)

Again, we will hold all equity ETF positions until our exit strategy signals otherwise.

Have a great week.

Ulli…

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

http://www.successful-investment.com/q&a.php

A note from reader Doug:

Q: Ulli: I read in your material that you have exited some bond ETF positions because of sell signals in that area. Did that activity supersede the 7% stop that you had on those bond positions? In other words, did something other than the 7% decline in share price cause you to exit the positions? If so, what was it?

A: Doug: For bond ETFs, I use a 5% trailing stop loss, but overriding was the fact that some of our holdings BND, TIP, TLH had not only broken below their long term trend lines but were showing poor performance. While some did recover, I found better opportunities elsewhere, like in low volatility equity ETFs.

Again, in regards to stop losses, for broadly diversified domestic/international funds/ETFs, I use 7%, for bonds, I use 5% and for sector and country ETFs, I use 10%.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at:

https://theetfbully.com/newsletter-archives/

The latest nonfarm payroll report shows the US economy created 88,000 jobs in March following a revised 268,000 gain in February though the jobless rate slumped to a four-year low of 7.6 percent due to a decline in the size of the labor force and participation rate.

The latest nonfarm payroll report shows the US economy created 88,000 jobs in March following a revised 268,000 gain in February though the jobless rate slumped to a four-year low of 7.6 percent due to a decline in the size of the labor force and participation rate.