ETF/No Load Fund Tracker Newsletter For Friday, May 10, 2013

ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

————————————————————

Market Commentary

Friday, May 10, 2013

THE WEEK OF RECORDS

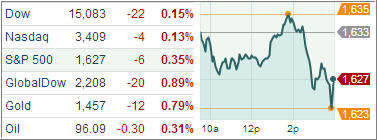

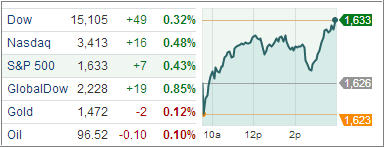

After enduring a choppy session, stocks settled higher to end the week with a gain despite a surge in the U.S. dollar and Federal Reserve Chairman Ben Bernanke’s speech offering no new revelations on the end date of the Fed’s asset purchase program.

The Dow Jones Industrial Average closed higher by 36 points (0.2%) at 15,118, the Standard & Poor’s 500 Index increased 7 points (0.4%) to 1,634, and the Nasdaq Composite ascended 22 points (0.8%) to 3,437. In light volume, almost 5.7 billion shares traded hands on U.S. exchanges today, or 9 percent below the three-month average.

The market rallied for a third straight week, amid optimism that the U.S. economy is improving caused by central-bank monetary stimulus. Without any major economic releases, traders and investors paid some attention to Fed Chairman Ben Bernanke’s speech to the Chicago Fed’s annual conference on bank structure and competition.

During his remarks, Bernanke mentioned that U.S. economy has not yet fully regained the jobs lost in the recession, and the financial system—despite significant healing over the past four years—continues to struggle with the economic, legal, and reputational consequences of the events of 2007 to 2009. The Fed Chief ensured that the Central Bank would continue to work toward improving its ability to detect and address vulnerabilities in our financial system. However, he did not offer any insight into the topic of the Fed tapering off its assets purchases, which speculation surrounding the idea has gained steam as of late and boosted the US dollar.

Oil prices tumbled as the U.S. dollar hit a four and a half year high against the yen and the dollar index was on track for its strongest week against other major currencies in 10 months. A strong dollar makes commodities priced such as gold and oil more expensive for foreign investors, pressuring shares of energy and basic materials companies.

The Dow and S&P 500 ended at record highs on Friday as a rise in Google and other technology shares offset a slide in energy stocks. For the week, the Dow rose 1 percent, the S&P 500 1.2 percent and the Nasdaq 1.7 percent.

With no domestic economic news of note, the markets relied on international events for directions. Positive monetary policy coming from Europe, along with a wider-than-expected trade surplus from China, stocks ended higher four out of five sessions this week. The S&P 500 climbed to new record highs in all four sessions, and the Dow broke through 15,000 for the first time. With U.S. consumer and China data to headline next week, it’ll be interesting to see if the Bull Run can continue?

Our Trend Tracking Indexes (TTIs) headed higher with the market indexes and closed the week as follows:

Domestic TTI: +4.56% (last week +4.30%)

International TTI: +9.30% (last week +8.62%)

Have a great week.

Ulli…

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

http://www.successful-investment.com/q&a.php

A note from reader Ed:

Q: Ulli: What are your thoughts on the PRPFX Fund with gold having dropped so fast??

A: Ed: I don’t own it, since it is hovering below its long-term trend line. There are far better opportunities in low volatility ETFs.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at: