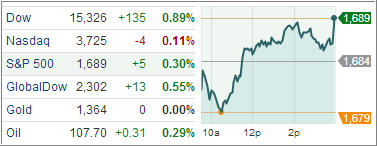

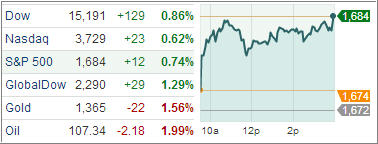

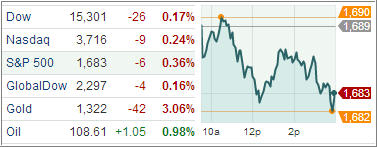

The U.S. Federal Reserve was back in the spotlight again as traders worried that the Fed would begin to scale back its monetary stimulus when it meets on Tuesday and Wednesday next week. U.S. equity averages fell, halting a seven-day win streak for the Standard & Poor’s 500 Index as materials producers slid amid growing concern over Syria.

Economic data showed first-time weekly claims for state unemployment benefits, the last major reading on the labor market before the Fed’s meeting, fell to the lowest level since 2006, but the picture was incomplete because two states did not process all their claims.

Nine of ten S&P 500 industry sectors ended in the red. After posting gains in each of the past seven sessions, several of this month’s top performers fell victim to some profit-taking. Financials, industrials, and materials led to the downside with losses ranging between 0.5% and 1.0%. The financial sector was pressured by the underperformance of most large banks as investors attempted to gauge the impact of a slowdown in the mortgage industry.