- Moving the market

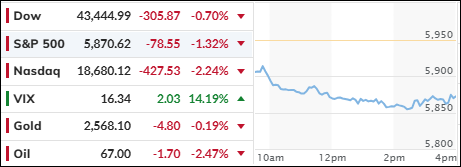

The markets opened in negative territory, with Nvidia’s stock slipping ahead of its highly anticipated earnings report. By the end of the session, the major indexes had recovered, closing near their starting points.

Traders view Nvidia’s upcoming report as a potential catalyst to invigorate the market for the rest of the year, especially after the recent pullback from the post-election rally that had propelled the indexes to new highs.

However, last week, Federal Reserve Chair Jerome Powell signaled that he is in no hurry to cut interest rates, which dampened bullish sentiment.

Retail stocks suffered significantly, with Target’s shares plummeting 20% following its largest earnings miss in two years and a reduction in its full-year guidance due to cost pressures and weakening discretionary demand.

This decline dragged down the major indexes, along with the retail ETF and other retail giants like Costco, Walmart, Dollar Tree, and Home Depot.

This situation reflects the challenges consumers face in an inflation-plagued environment. Given that consumer spending accounts for 67% of GDP, the markets may soon recognize that the economic data might be more hype than reality.

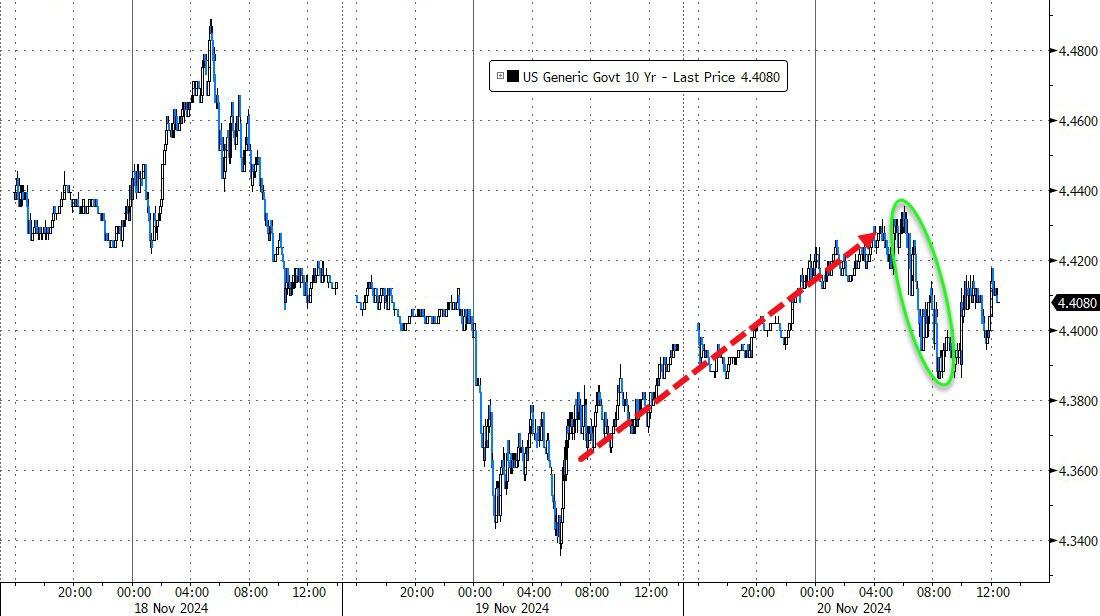

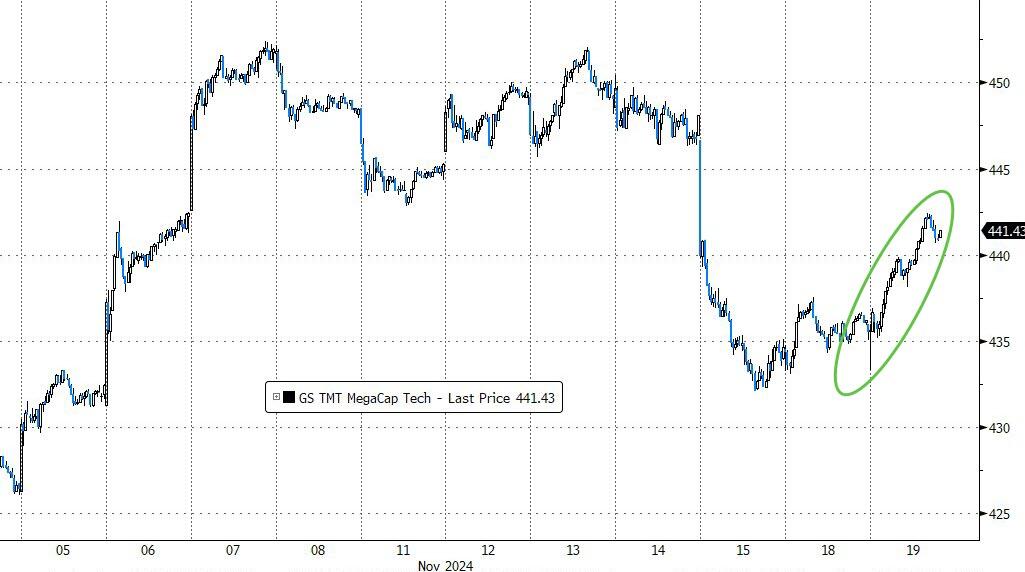

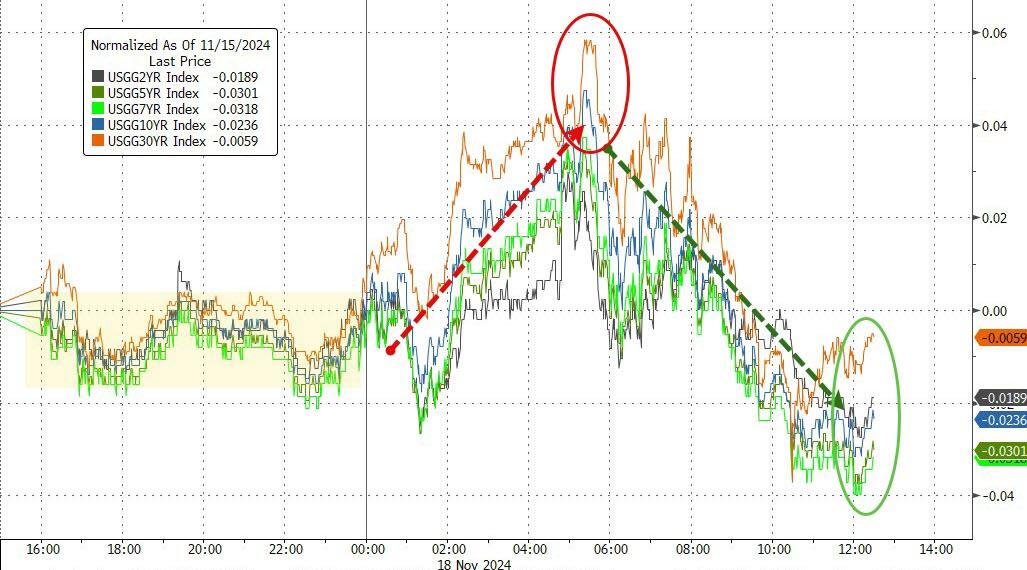

The Mega-Cap tech sector experienced a sharp decline but managed to rebound, mitigating early losses. Bond yields ended the day slightly higher but showed significant intra-day volatility.

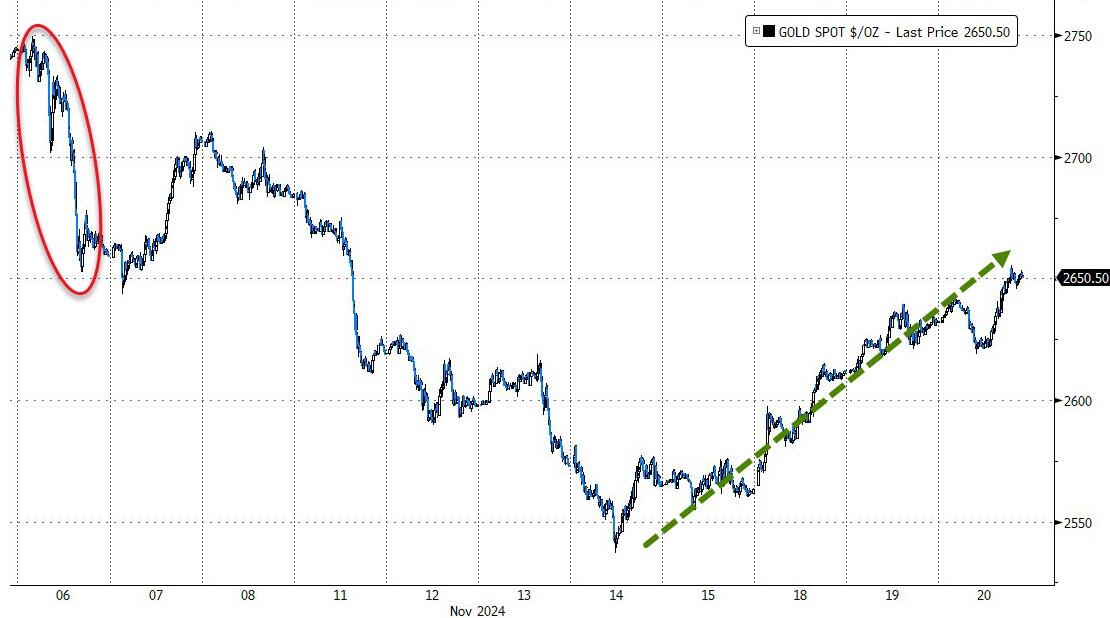

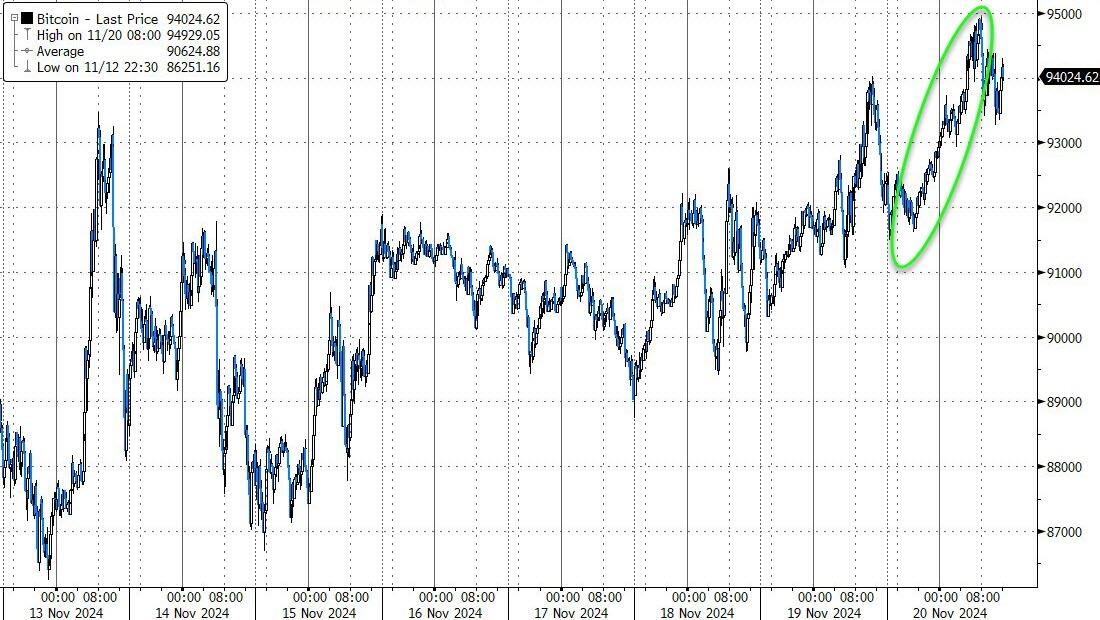

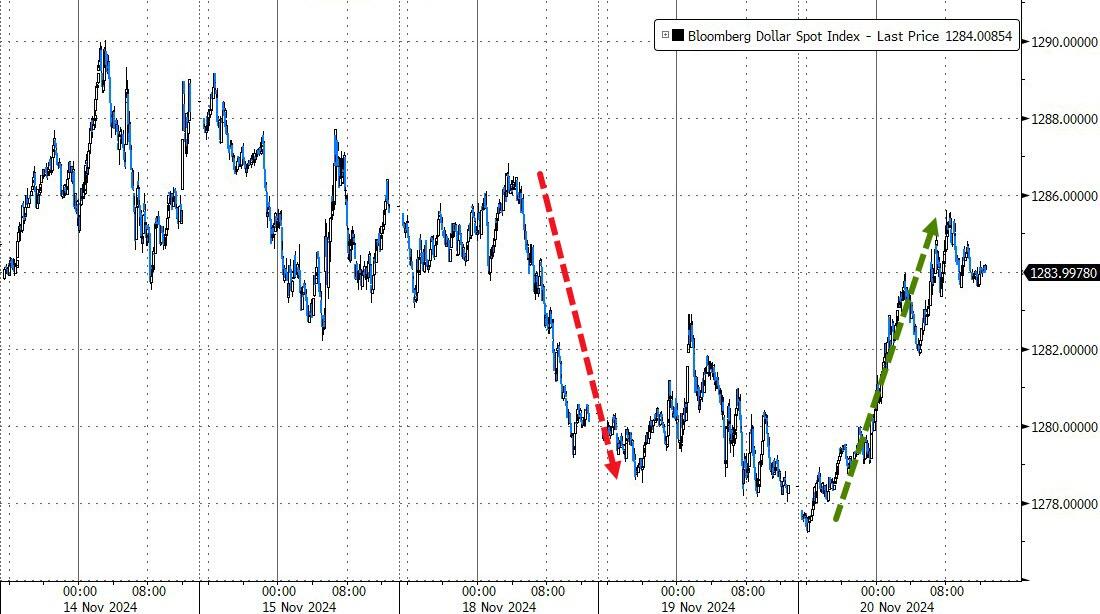

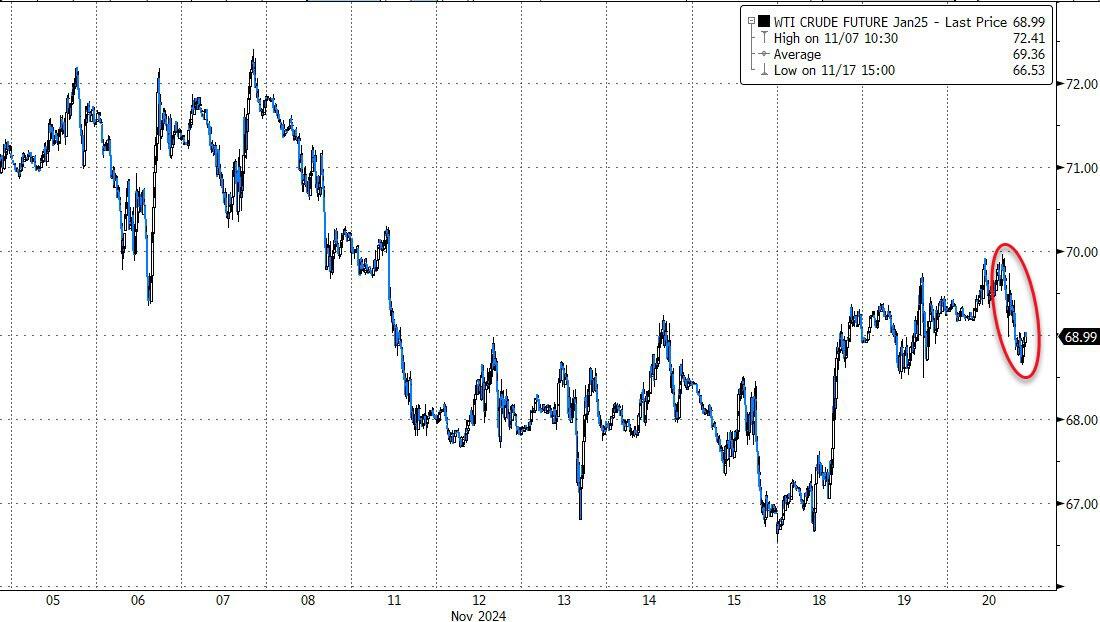

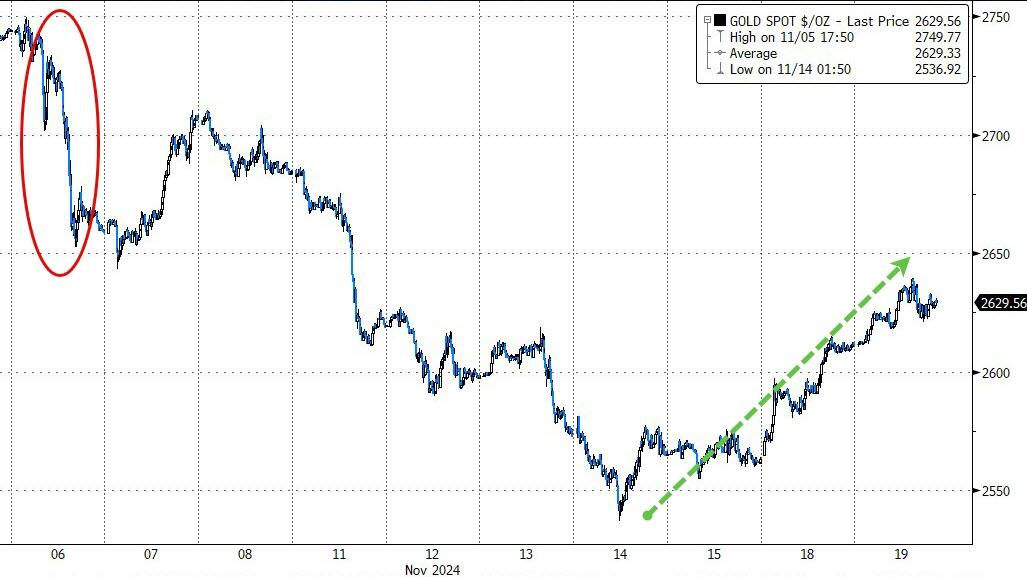

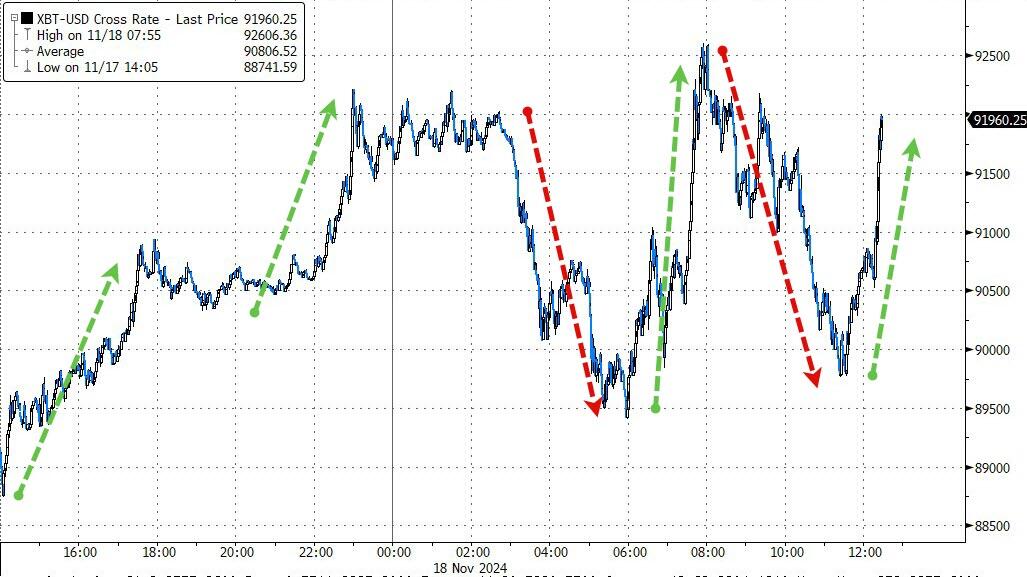

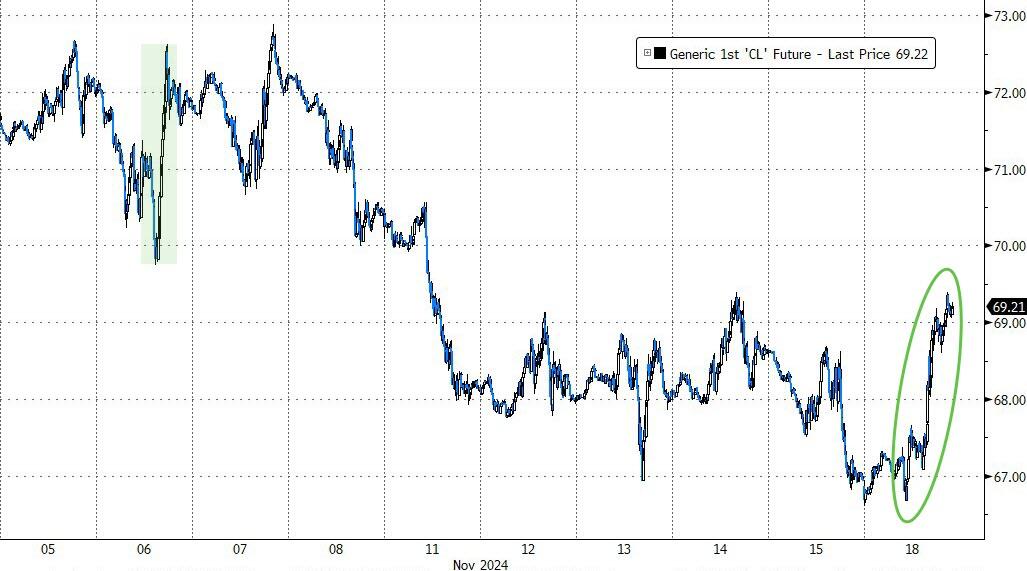

Gold prices rose for the third consecutive day, while Bitcoin hit another record high close to $95,000 before pulling back slightly at the end of trading. The dollar rebounded from Monday’s losses, and crude oil prices slipped in afternoon trading.

All eyes are now on Nvidia’s earnings report, due out this afternoon, which many traders consider the most crucial announcement for the remainder of the year.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}