- Moving the market

The major indexes received a boost early this morning from a better-than-expected Producer Price Index (PPI) report. Despite the tech sector suffering most of the losses yesterday and last week, it managed to advance today, although it dropped below its unchanged line by the close.

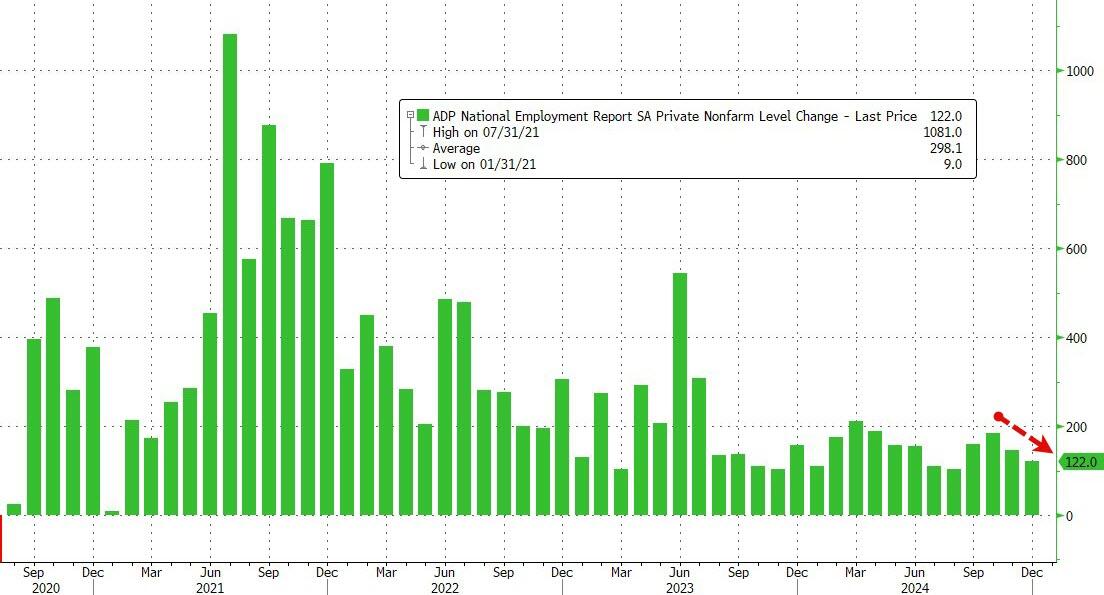

The PPI, which represents wholesale inflation, increased by 0.2% in December, compared to estimates of 0.4%. Year-over-year, the PPI surged from 3.0% to 3.3%. The Core PPI, which excludes food and energy, remained unchanged.

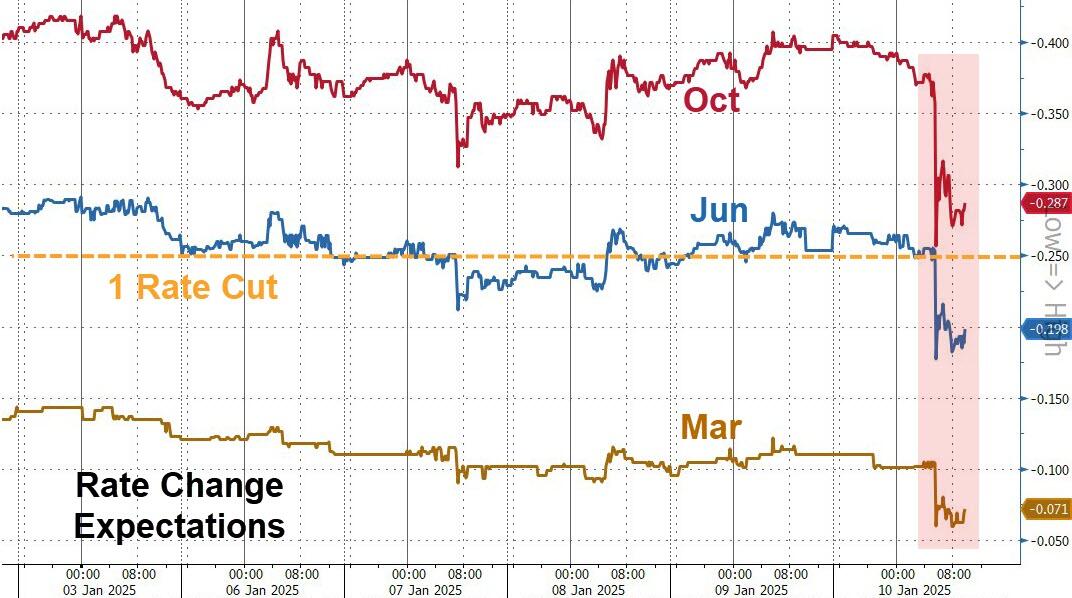

Tomorrow’s Consumer Price Index (CPI) reading is expected to have a more significant market impact. If the CPI comes in hotter than anticipated, the Federal Reserve may slow down any interest rate cuts, which typically does not bode well for stocks. Despite current conditions, there is a 78% chance that the Fed will maintain its current rate policy when they meet later this month.

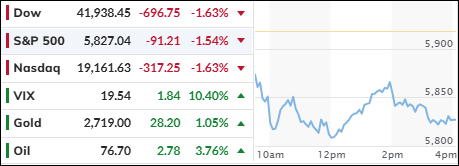

Today was another volatile day in the markets, with indexes fluctuating above and below their respective unchanged lines. Small Caps emerged as the top performers, while the Nasdaq lagged.

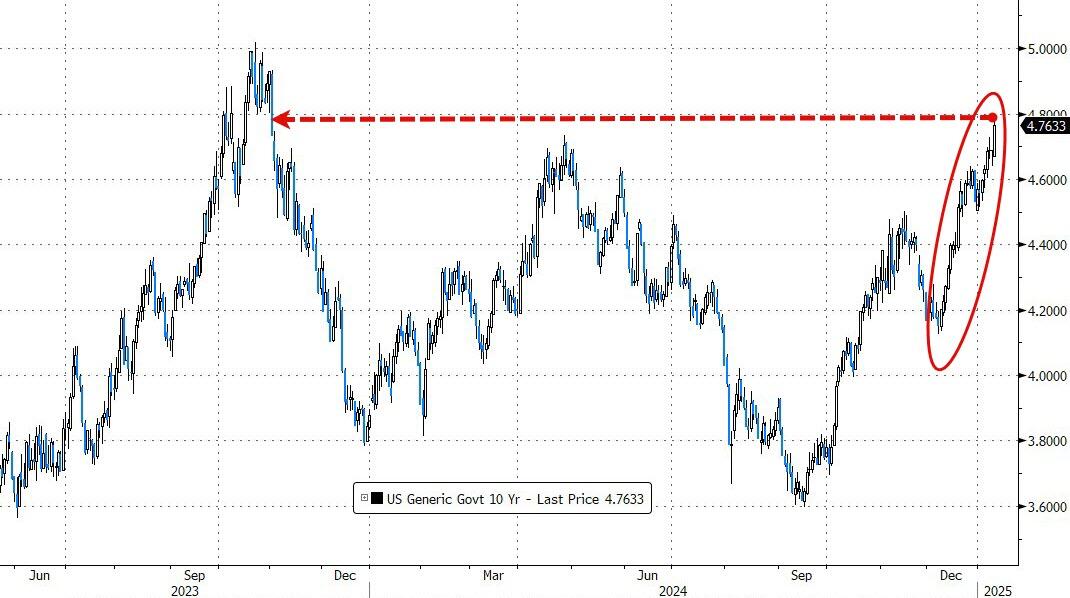

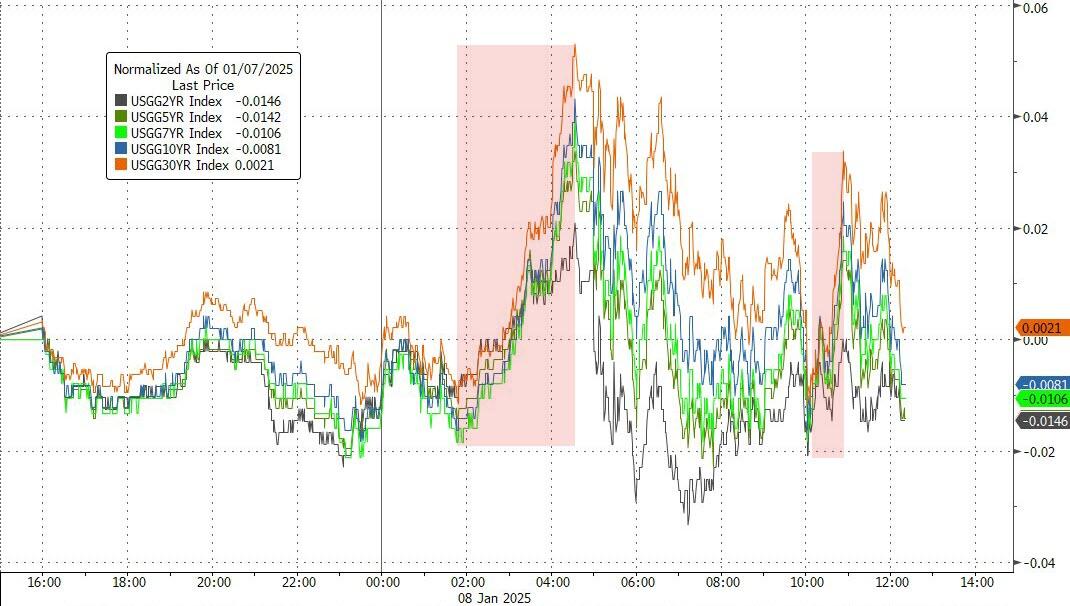

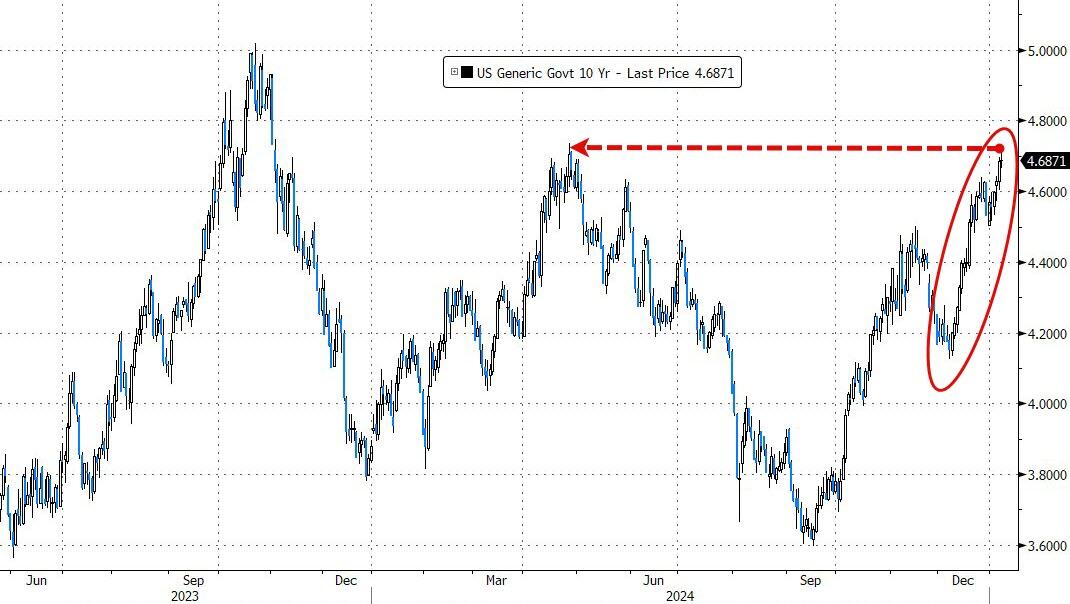

The S&P 500 hovered around its 100-day moving average, and Mega Caps dropped for the sixth consecutive day. Bond yields were mixed, with the 10-year yield eking out a small gain, while the 30-year yield crossed the 5% level to the upside for the first time since November 2023.

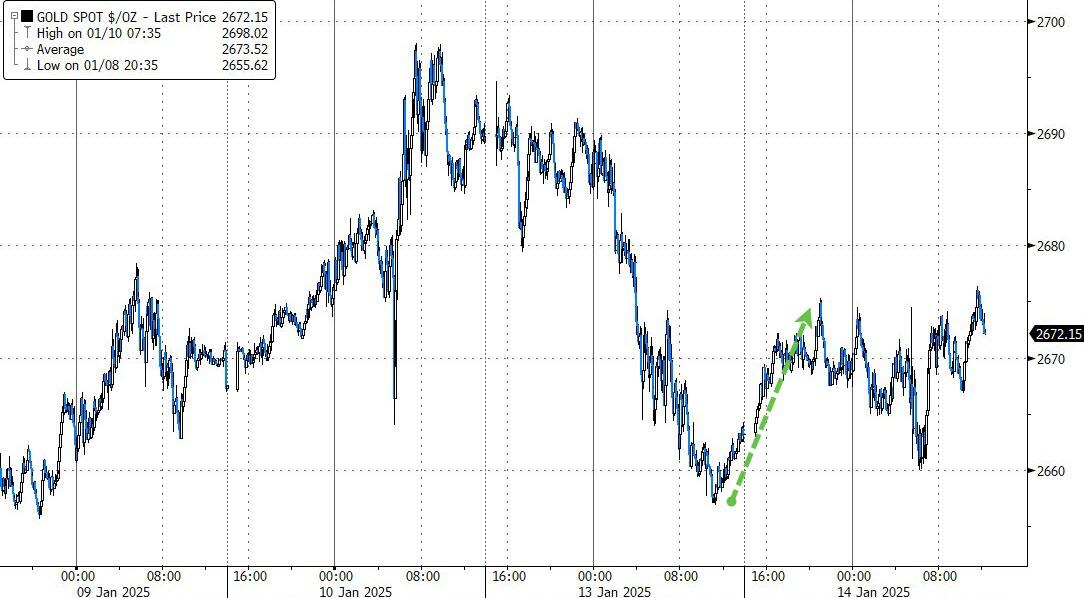

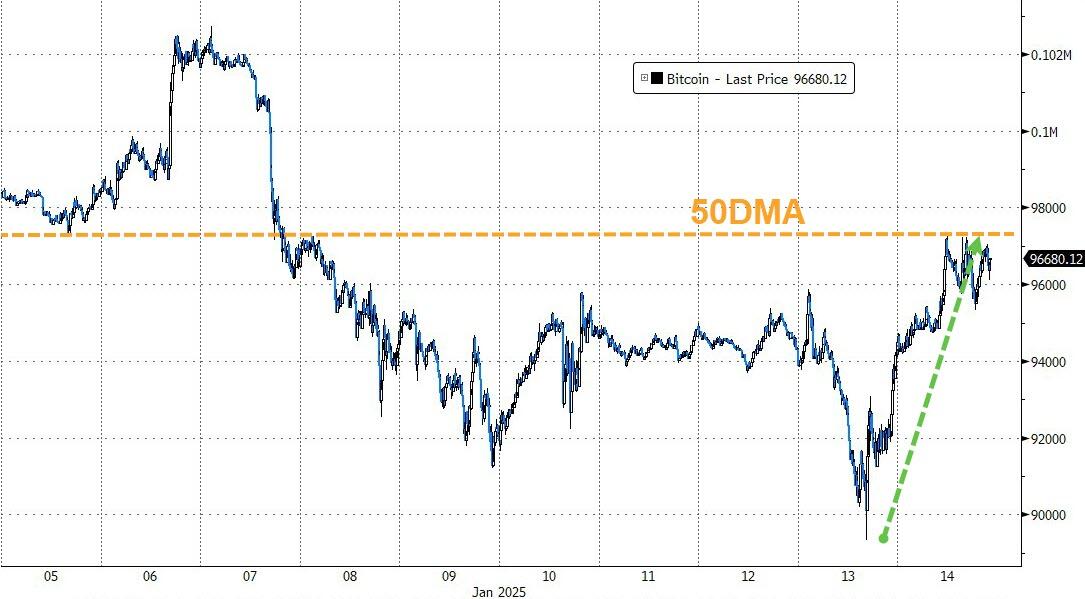

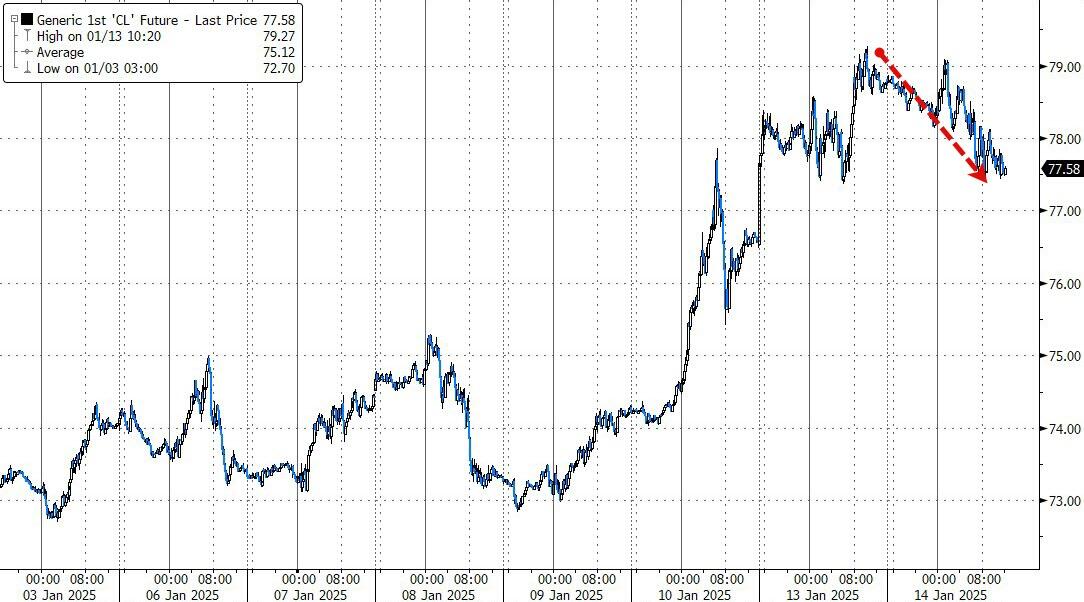

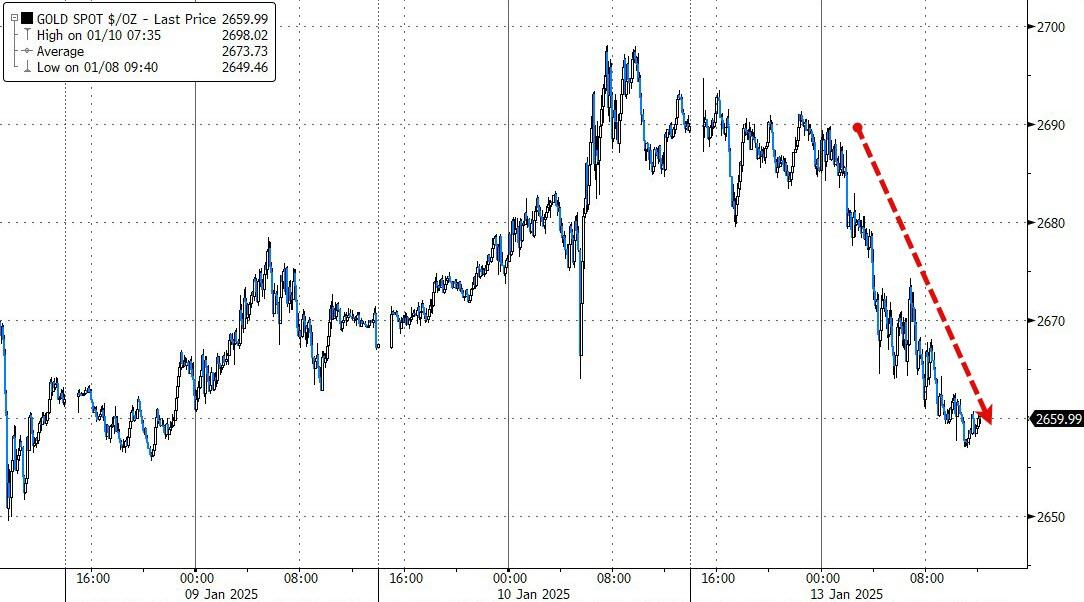

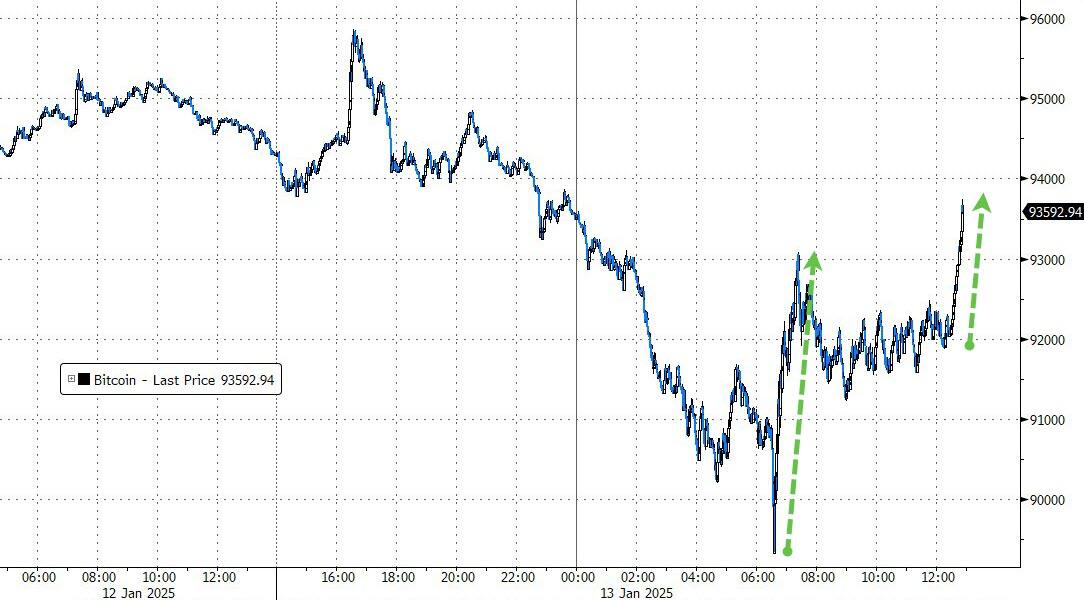

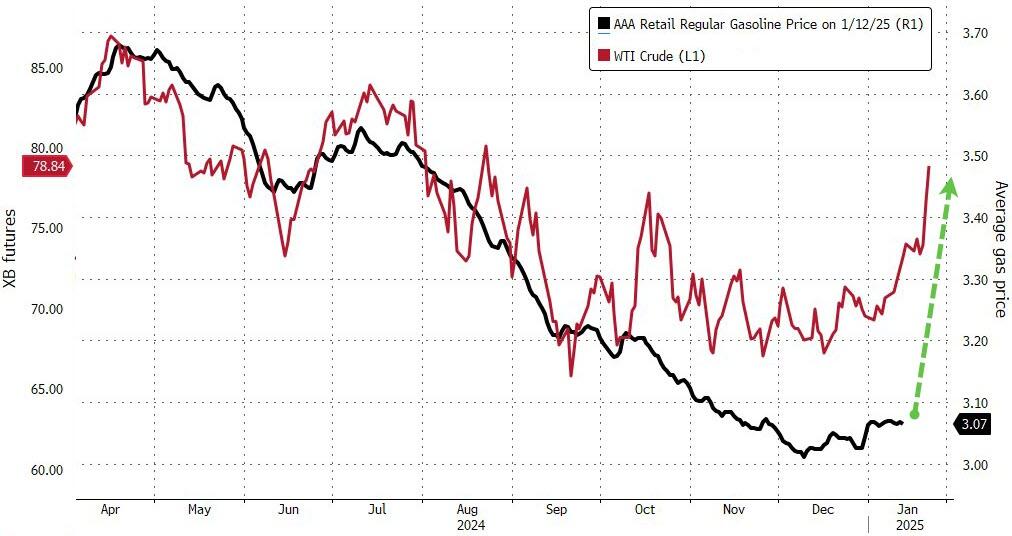

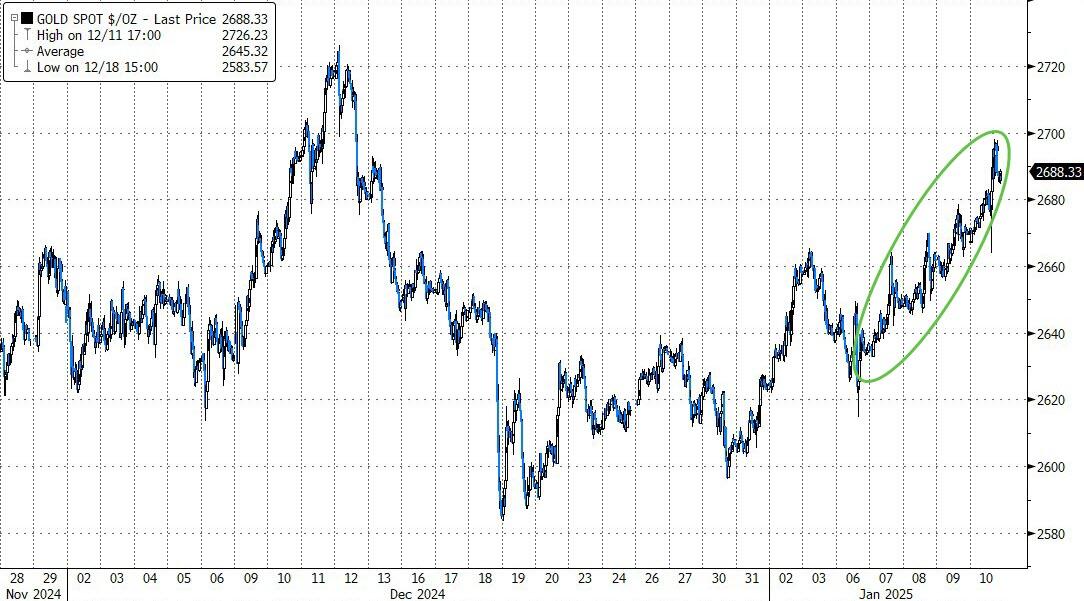

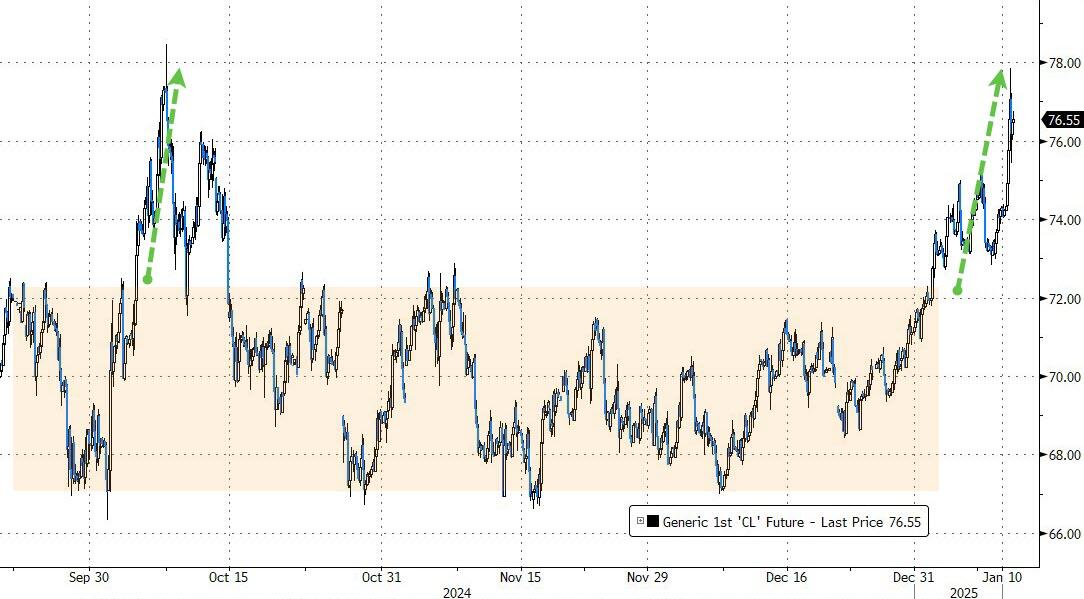

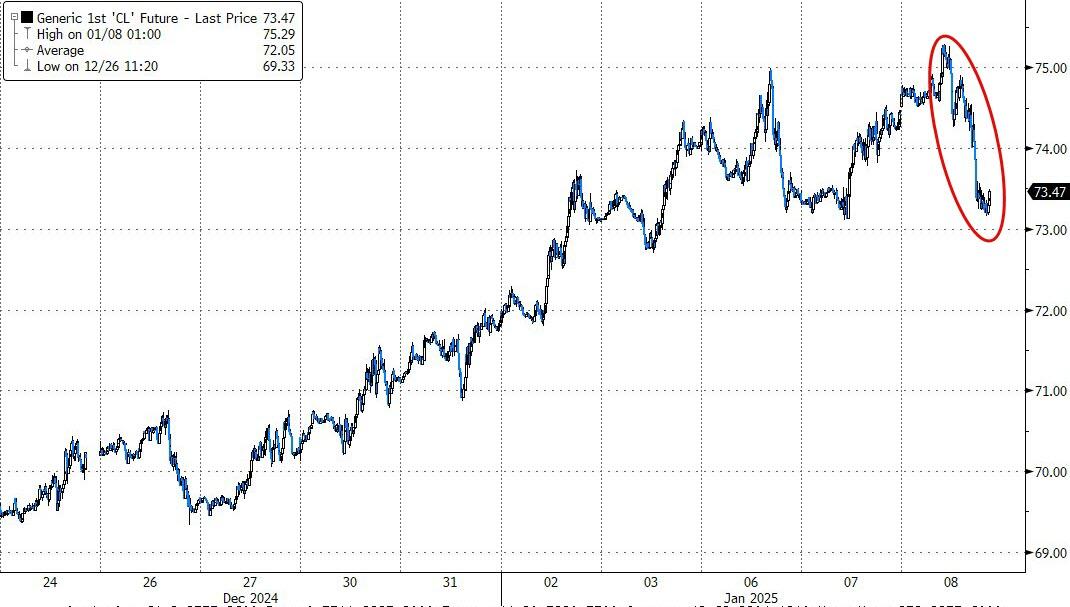

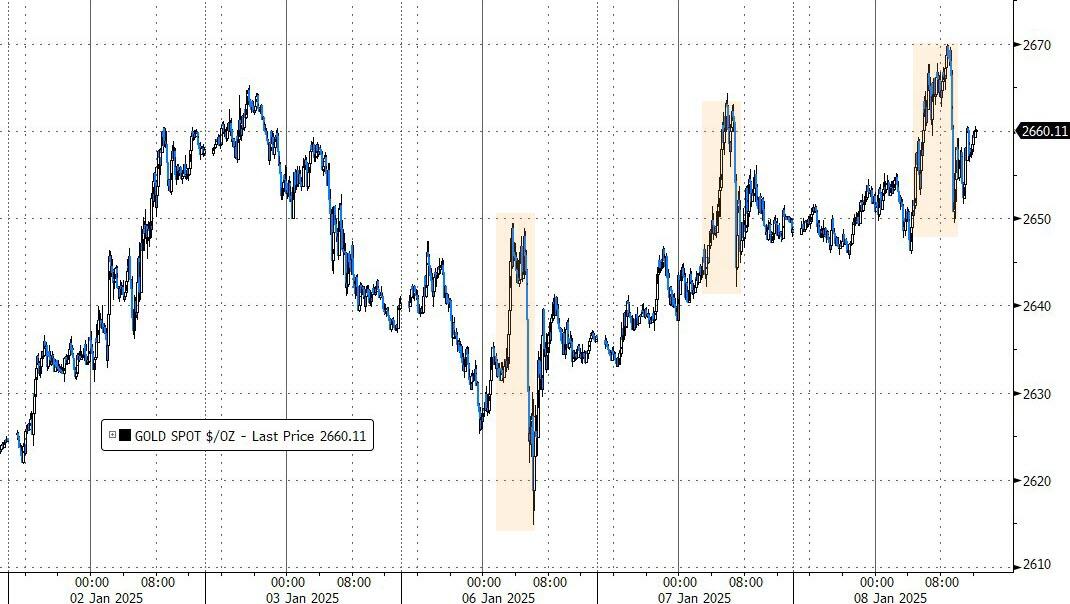

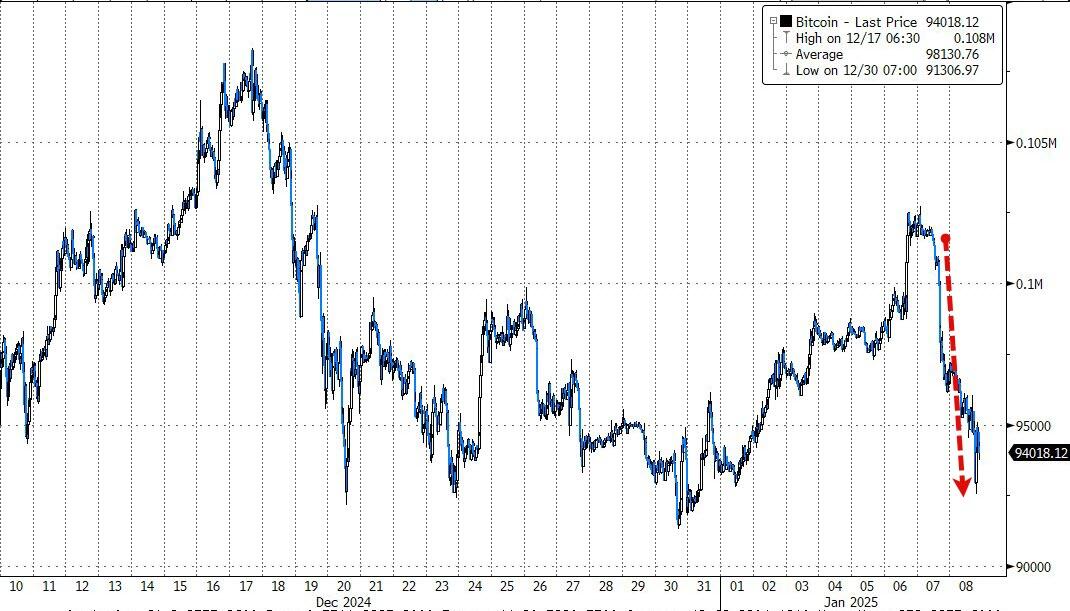

The dollar tumbled, which helped gold to achieve a modest advance of +0.44%. Bitcoin, after breaking below $90k yesterday, found some footing and surged towards $97k, while crude oil prices dipped below $78.

We witnessed wild swings throughout the session, with bulls and bears engaged in a tug-of-war. Will tomorrow’s crucial CPI report declare a winner?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}