ETF Tracker StatSheet

You can view the latest version here.

TARIFF TRUCE AND SOFT INFLATION DATA SPARK MARKET REBOUND DESPITE CAUTION

- Moving the market

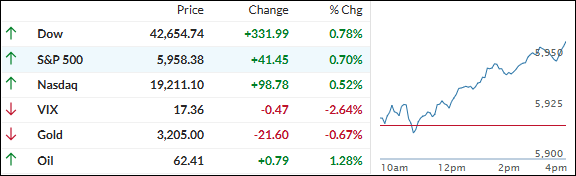

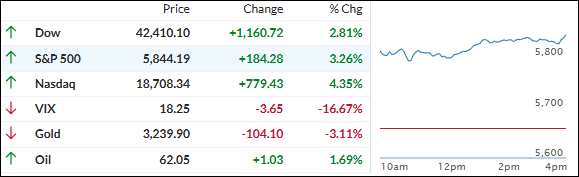

The markets began the day on a cautious note, with a disappointing consumer sentiment report halting the S&P 500’s four-day rally-a run that had been fueled by a temporary U.S./China tariff agreement and encouraging inflation data.

Despite the initial pause, the major indexes regained strength as the session progressed, buoyed by renewed optimism over global trade policy and softer-than-expected inflation figures.

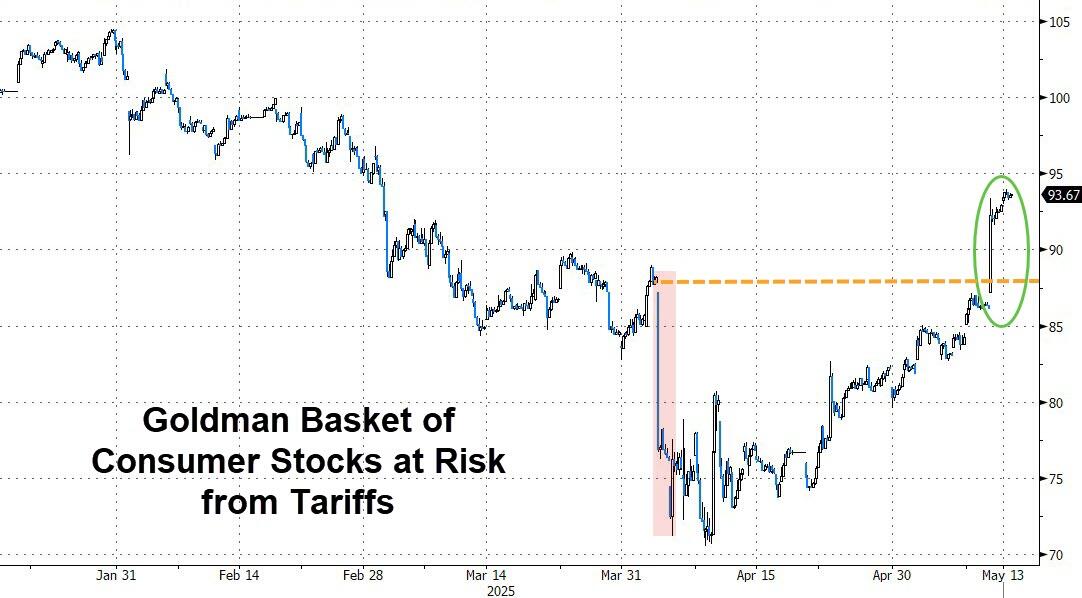

The S&P 500 has rebounded sharply since the announcement of the 90-day tariff truce, now breaking above its widely watched 200-day moving average-a technical milestone often interpreted as a bullish signal.

Our domestic TTI has mirrored this upward momentum, and unless there is a sudden reversal, I anticipate re-entering domestic equities by next week.

However, consumer sentiment weighed on traders’ enthusiasm early in the session. The latest reading fell to 50.8 in May from 52.2 in April, while inflation expectations for the coming year surged to 7.3% from 6.5%, reflecting growing concerns about the impact of Trump’s tariff policies.

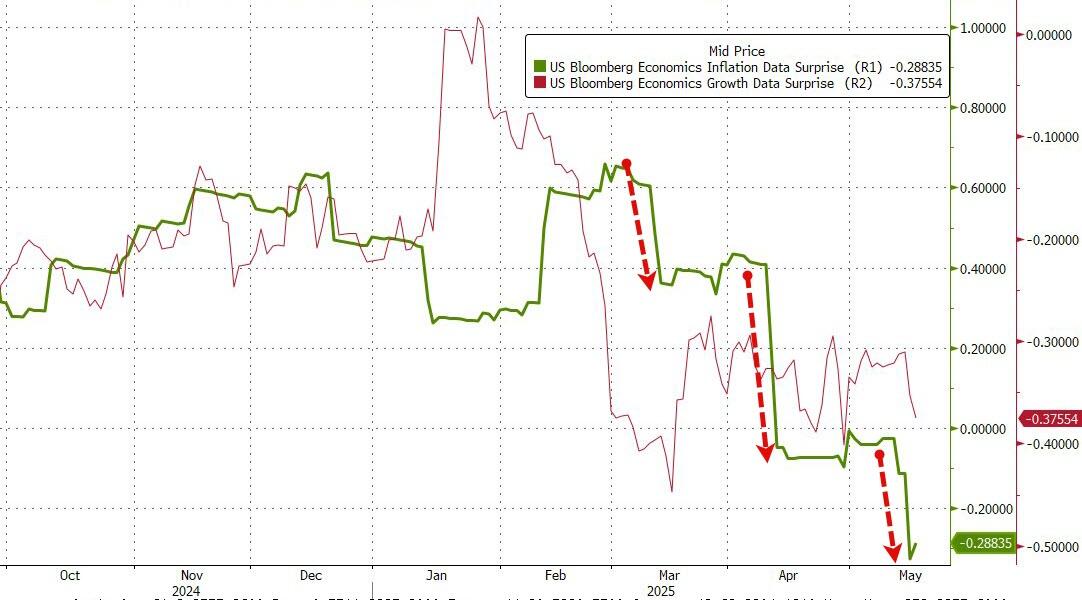

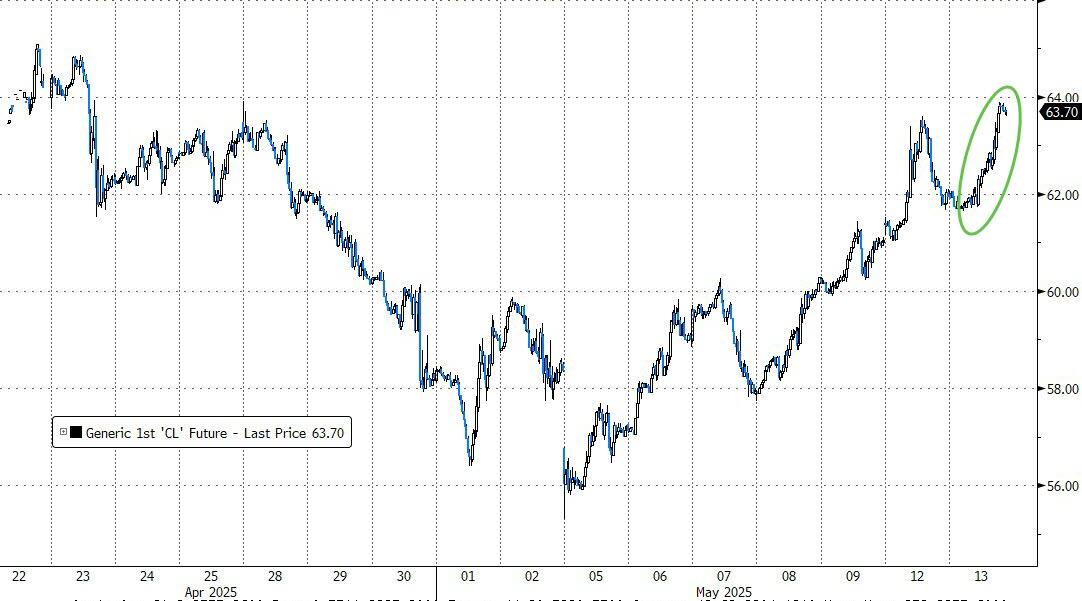

As the day unfolded, uncertainty over global trade policy eased and “soft” economic data improved, helping the major indexes stabilize and allowing bullish sentiment to return. Notably, inflation-related macroeconomic data continued to surprise to the downside, as highlighted by ZeroHedge.

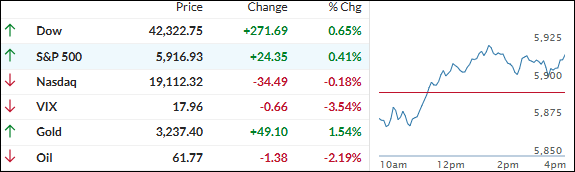

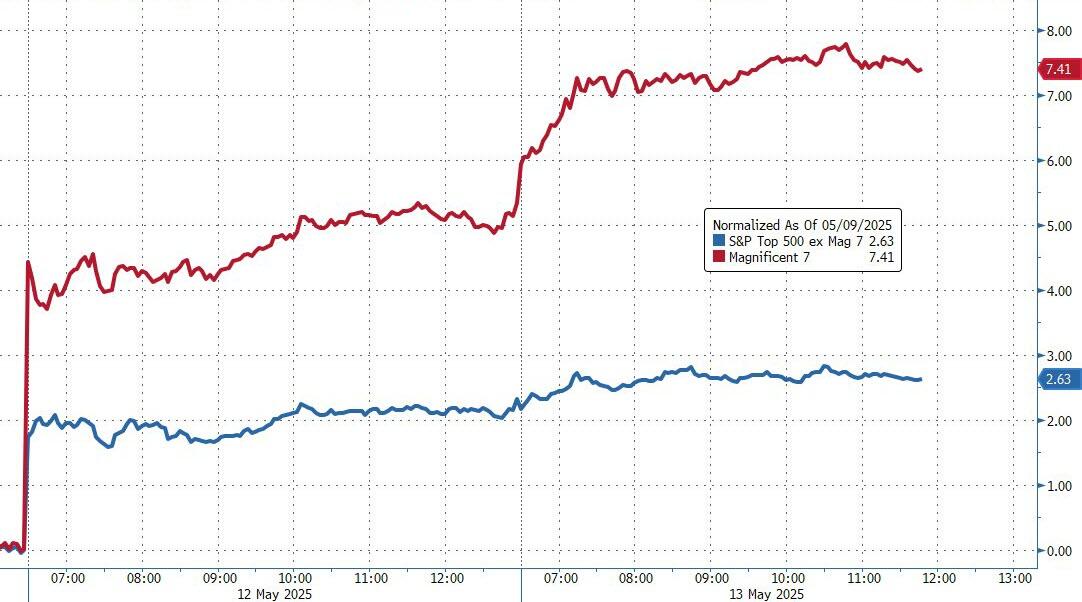

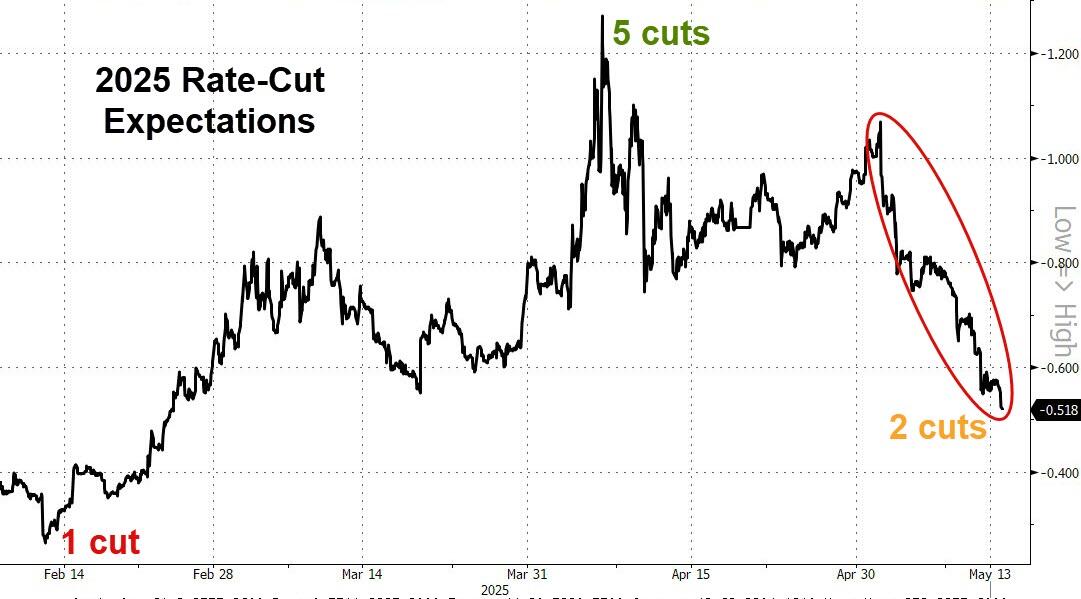

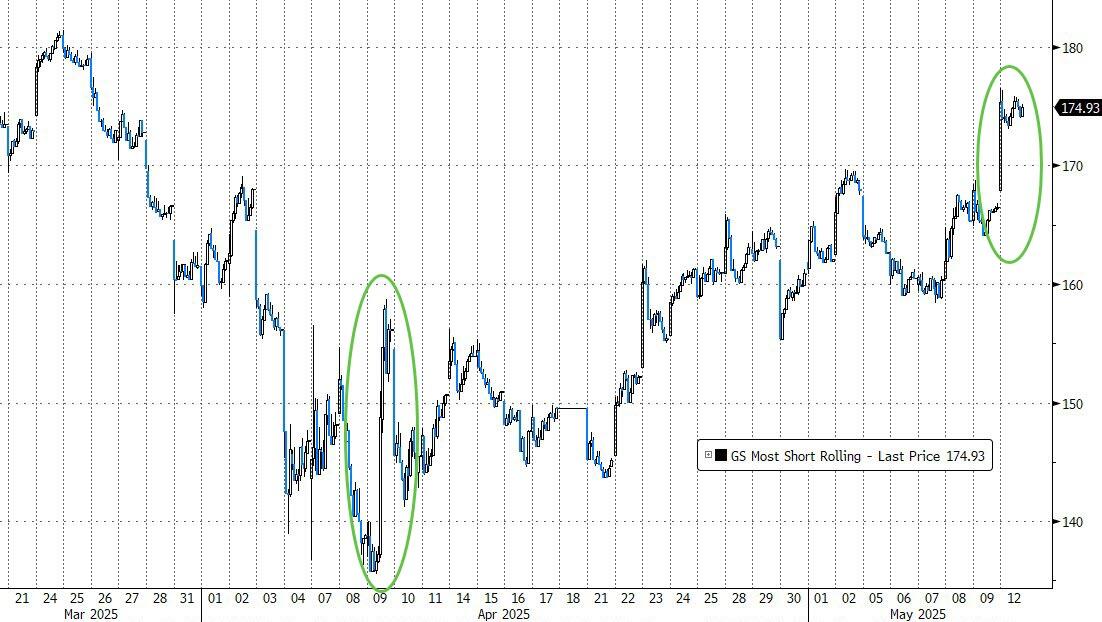

This week also saw the largest short squeeze since last Thanksgiving, driving the Mag7 basket to continue its impressive rebound. Bond yields climbed for the third consecutive week, yet this rise did not negatively impact equities—a divergence from typical market behavior.

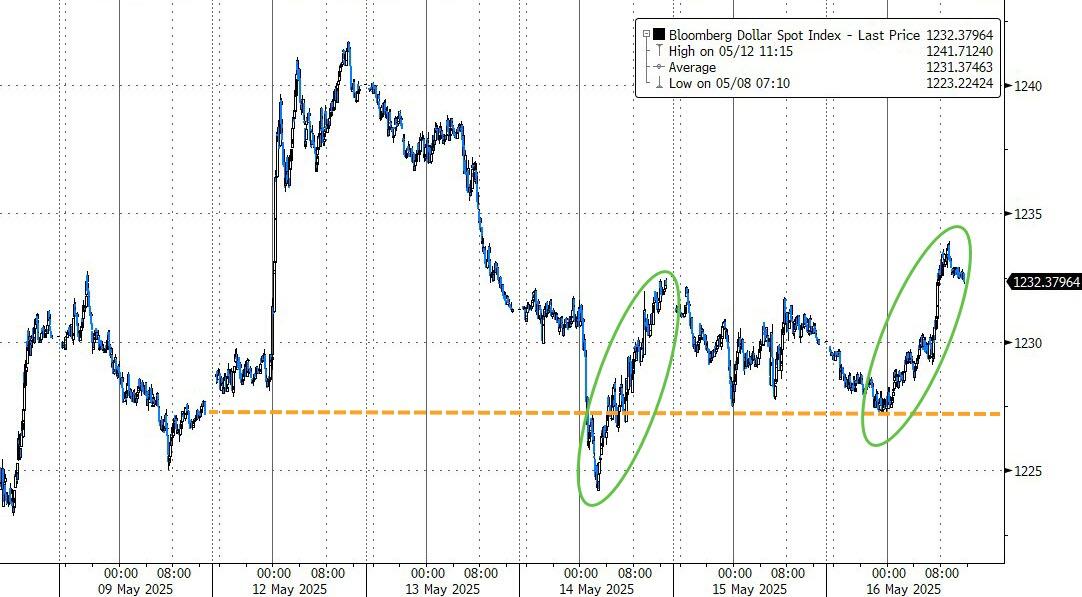

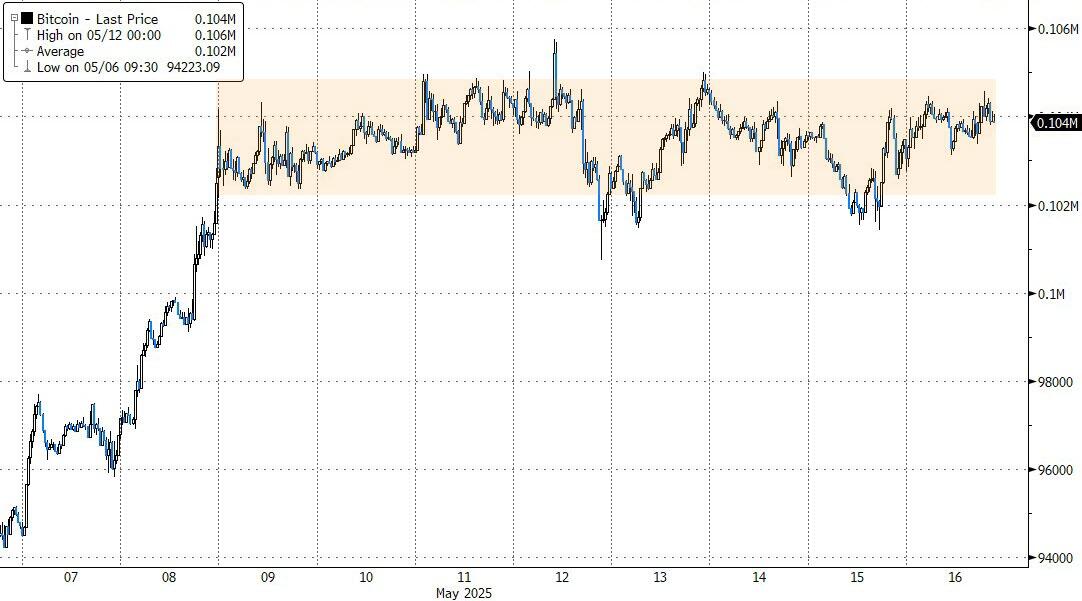

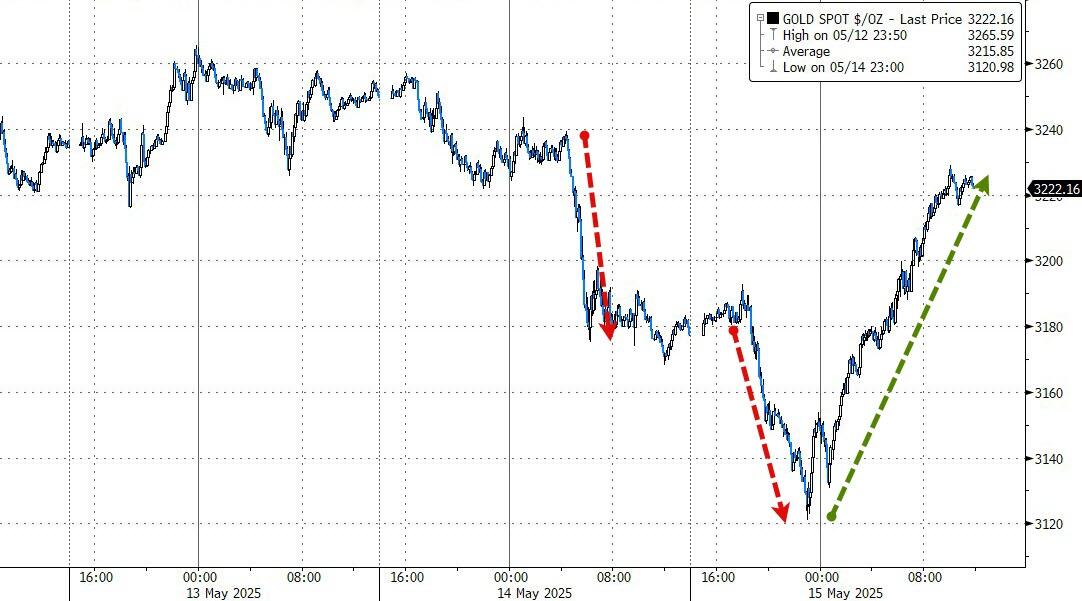

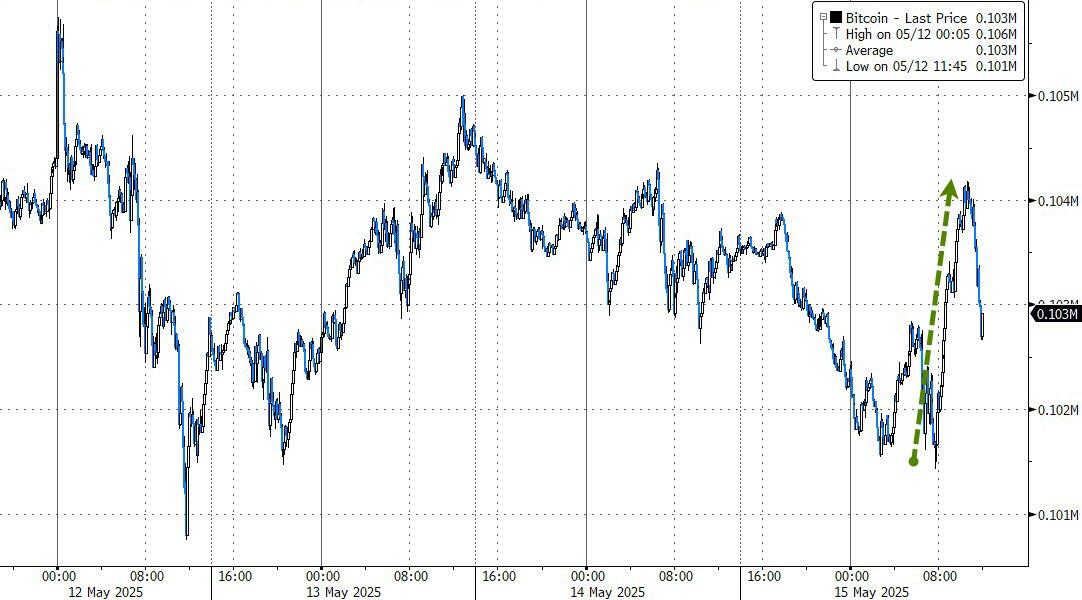

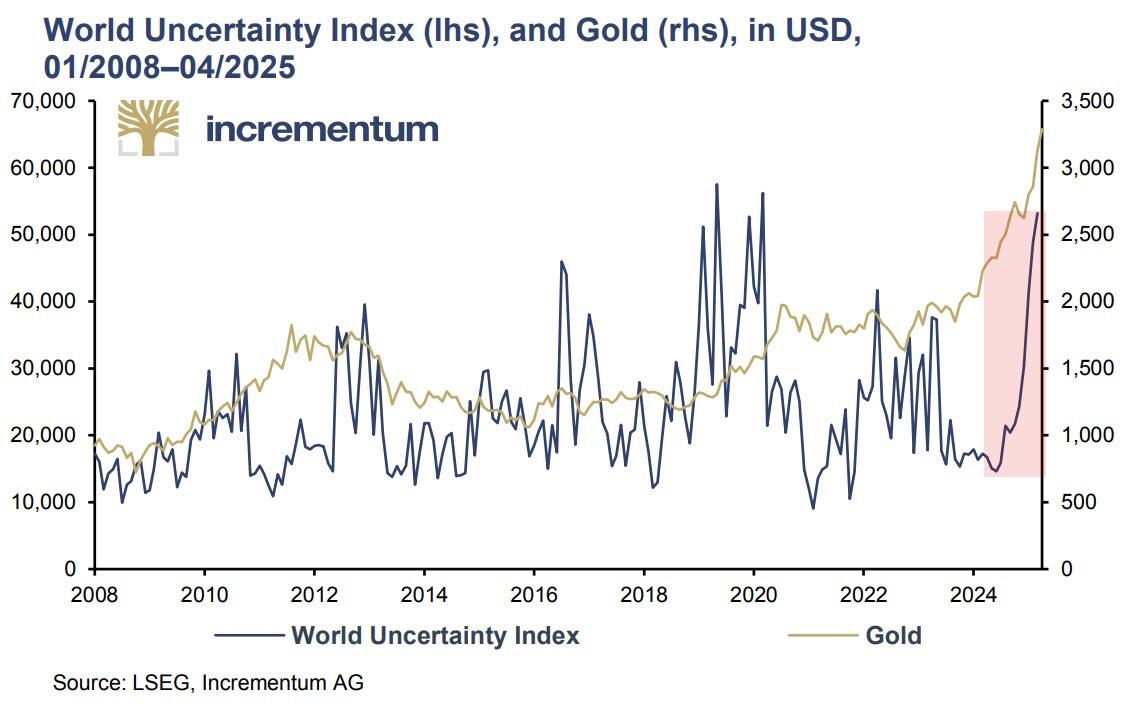

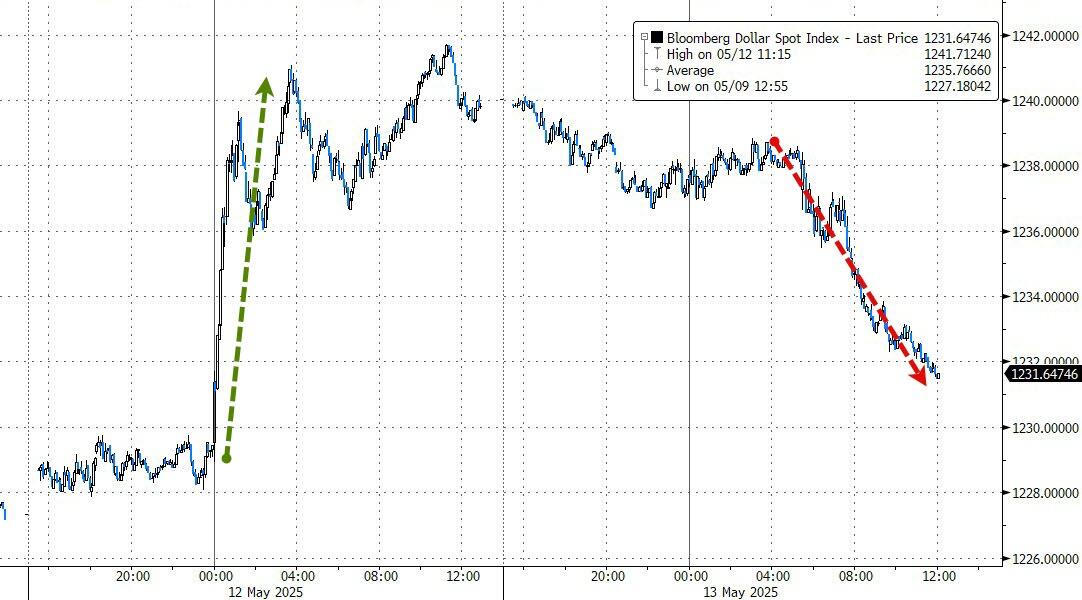

Meanwhile, the dollar strengthened for a second week, pressuring gold prices lower as some market uncertainties subsided. Bitcoin, after five weeks of gains, ended the week unchanged.

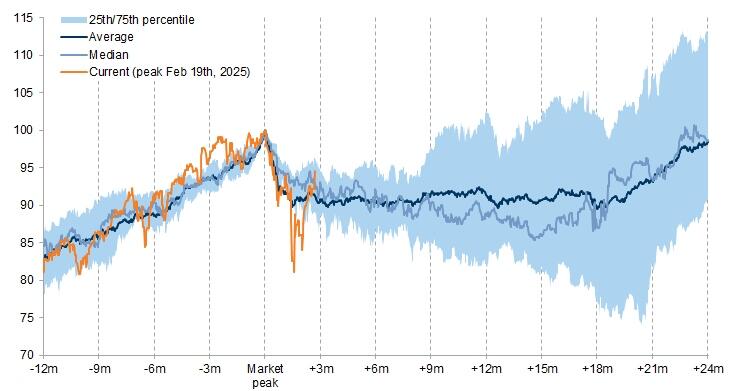

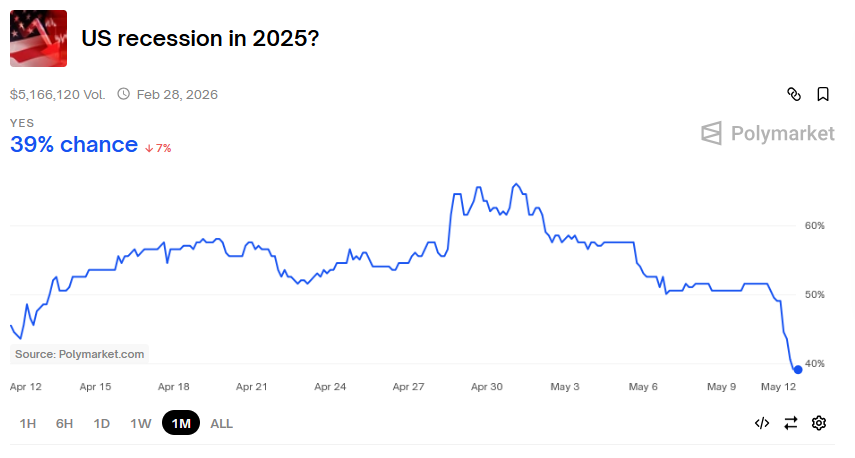

It’s worth noting that equities have just experienced one of the sharpest drawdowns in the past 75 years but have managed a swift recovery. Still, historical patterns suggest that the path for further gains may be challenging from here.

Regardless, we will continue to follow our TTIs, with a new “Buy” signal likely to be confirmed on Monday.

Still, the question remains: With markets at a crossroads, will the recent rebound prove sustainable, or will historical trends reassert themselves and cap further gains?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}