- Moving the Markets

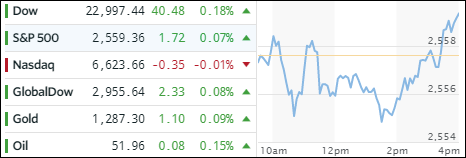

Early morning selling pressure, possibly related to the 30th anniversary of the 1987 crash, pushed the major indexes lower, with the S&P 500 being down a non-newsworthy -0.33%, before starting the long climb towards the unchanged line.

Other reports were mixed with earnings being robust while political tensions in Europe and questionable economic data out of China underpinned the early negativity. In the end, two of the three major indexes managed to close in the green with the Nasdaq trailing and closing in the red, in part due to Apple (AAPL) having a really bad day (-3.78%).

A spike in the VIX to 11 caused the markets to show the early weakness, but manipulating this index off the highs and pushing it sharply lower contributed to today’s rebound. Still, the recovery was not much to brag about, as most ETFs closed on a mixed note. On the upside, we saw Dividend ETFs (SCHD) leading with a gain of +0.23% with MidCaps (SCHM) occupying second place (+0.10%). Heading up the losers were Emerging Markets (SCHE) and International SmallCaps (SCHC), which retreated -0.83% and -0.63% respectively.

In the interest rate arena, the yield on the 10-year bond dropped 1 basis point to 2.33% helping the 20-year bond price (TLT) to squeeze out a +0.18% gain. Gold pushed towards its $1,300 level again, while oil slipped -1.23%. The US dollar (UUP) followed suit by gapping down and losing -0.25%.