ETF Tracker StatSheet

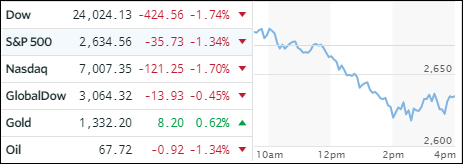

LACKLUSTER SESSION KEEPS INDEXES IN CHECK

- Moving the markets

A rising tide is supposed to lift all boats, but that was clearly not the case today. After yesterday’s strong earnings results from Amazon, Intel and Microsoft, you would have expected a follow through bullish day for the tech sector, which never happened.

After an early uptick, the markets vacillated around the unchanged line and ended up with the Dow in the red, the Nasdaq just about unchanged and the S&&P gaining a tad. It was dampened enthusiasm at its best despite the 3 players being involved representing some of the biggest and most influential companies in the world. Go figure…

Maybe Exxon’s tepid earnings report contributed to the lack of buying along with the latest GDP data. It showed that sharply slowing personal consumption had an effect as the Q4 2017 GDP number of 2.9% looks really good right now compared to the just released first quarter annualized GDP of 2.3%, which is the lowest in the past year.

None of these numbers confirm that the economy is rip-roaring but is decelerating with only some sectors showing strength. Even an assist in the form of the 10-year bond yield (2.96%) continuing to slide further away from the 3% marker had no influence on market behavior.

I think we are still stuck in a broad sideways pattern but we will, as is virtually a guarantee, break out at some point. The open ended question is whether it will be to the upside or to the downside. Only time will tell.