- Moving the markets

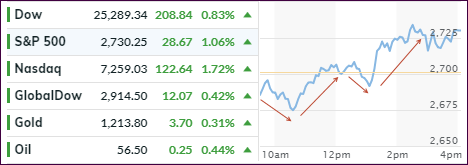

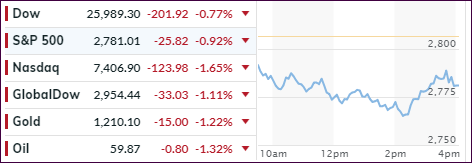

Equities headed south in early trading, which was the validation confirming yesterday’s “Sell” signal for “broadly diversified domestic equity ETFs.” The markets dumped at first then see-sawed higher in what can be considered a drop, pop, drop and pop kind of session, during which all 3 major indexes ended in the green for a change ending a skid of 5 consecutive losing days for the S&P 500.

Our main directional indicator, the Domestic TTI, recovered a bit but remains stuck on the bearish side of its trend line. This will keep us on the sidelines until the TTI breaks back above it and shows some staying power at the same time. With the current wild swings in the market, and a projected year-end rally, we may find ourselves back in sooner rather than later.

Today’s roller-coaster was all about the latest version of the trade headlines. First, there was news of a trade truce causing a market bounce, then a drop, as the trade truce was denied, followed by a rally on news that next batch of tariffs have been shelved for the time being.

This back and forth surrounding one event make it questionable whether this late rebound will have legs or falter again, as we’ve seen in the recent past. Additionally, there is ongoing tightness of financial conditions which, if not resolved, may have a negative effect on equities, if this chart forecast is correct.

{kind=link}

{kind=link}