[Chart courtesy of MarketWatch.com]

- Moving the markets

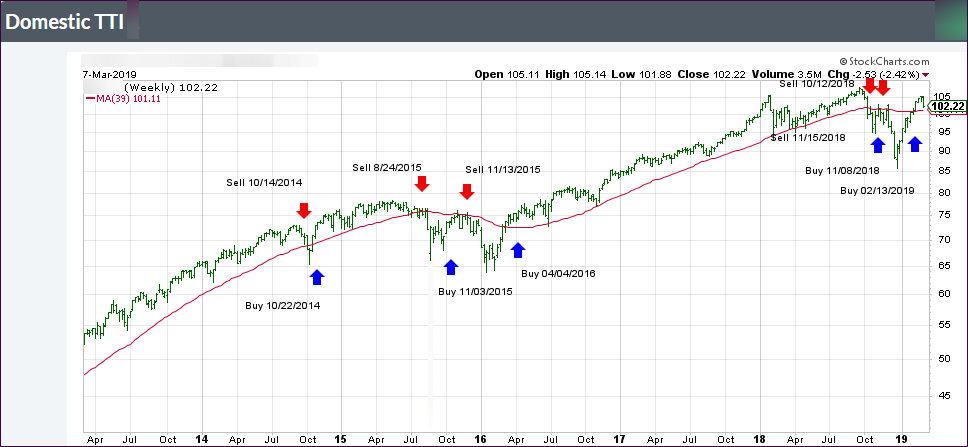

The major indexes were unable to touch the plus side of the unchanged line, as the historic Christmas rebound struggled for the second day with the S&P 500 not being able to decisively cross above its apparent glass ceiling, namely the 2,800 level.

Global markets slipped as well with investors waiting for new catalysts either from the trade arena or dovish comments from the monetary authorities. Neither was forthcoming throughout the session, so we traveled the path of least resistance, which was lower.

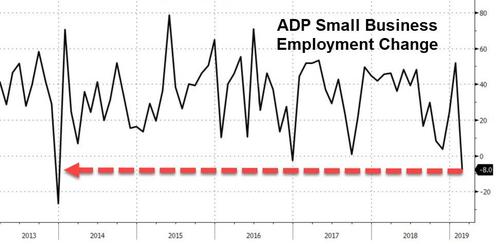

Regarding economic data, ADP reported dramatically slowing employment gains for February with the print coming in at 183k, which was slightly below the expected 190k. However, January’s gains were upwardly revised to 300k, which make the February reading even more disappointing. Small businesses noted the biggest drop in jobs since 2013.

We also saw the US trade deficit soar to $621 billion, which was its highest since 2008 and is not exactly a positive for the pending U.S.-China trade negotiations. To add insult to injury, Chines equities are soaring while U.S. markets are not.

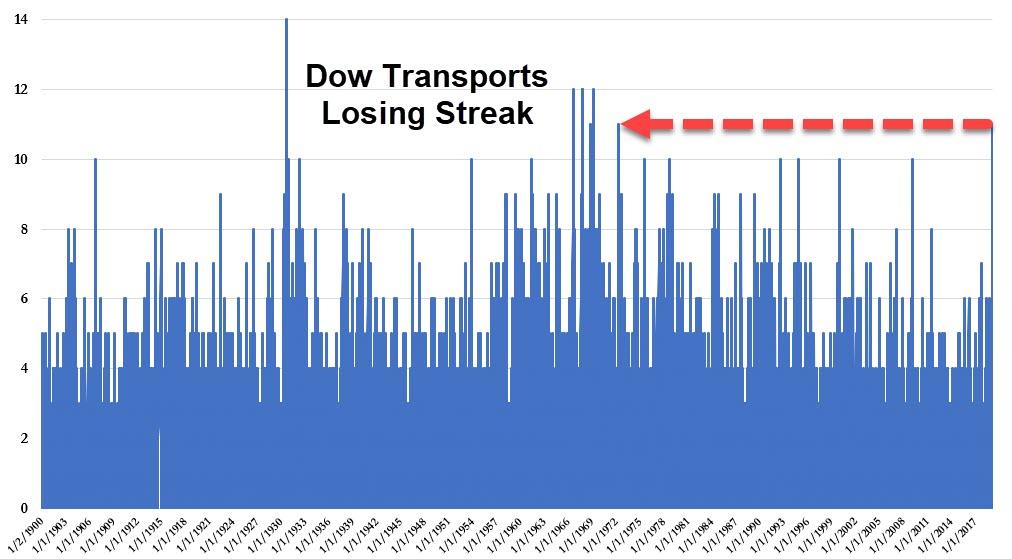

SmallCaps got spanked (3% this week) and dropped below its 200-day M/A, while Transportations were down the 9th day in a row making it its longest losing streak since February 2009. High yield credit (HYG) has dropped 5 days in a row, meaning that rates have been rising.

On the other hand, 10-year bond yields have been doing an about face by fading after last week’s sharp rally, but there has been no positive fallout for the stock market.

Things appear a little topsy-turvy right now, and we’ll have to wait and see which way this will play out. However, could it possibly be that global money supply, which has started to roll over, is the real culprit for this weakness in equities?

If that trend continues, watch out below.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}