- Moving the markets

While the major indexes closed in the green to start the week, the gains were minor despite the Nasdaq scoring back to back record closes. The S&P 500 managed to notch a new intra-day high but slipped into the close barely finding support above the unchanged line.

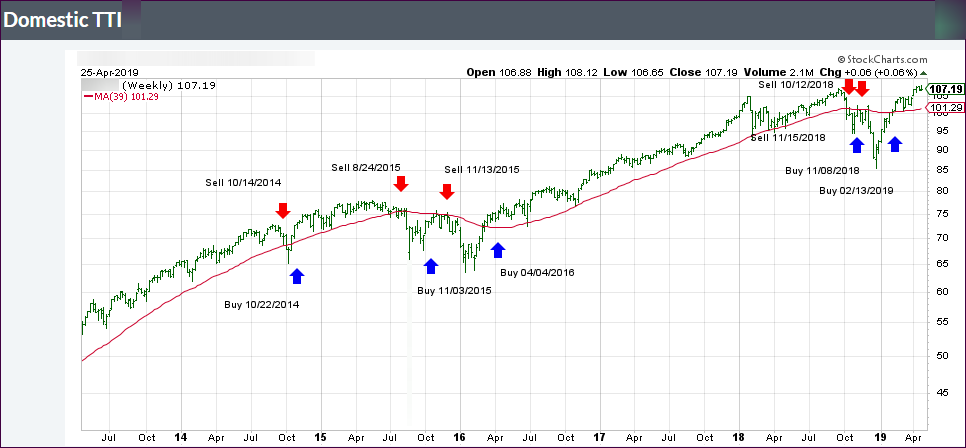

The index has now reached an extremely overbought level, the most since January 2018, which was a moment in time that signaled an upcoming sudden and sharp correction. Complacency is high with VIX showing record short positions, which means traders are betting on a continued stream of low volatility. That is absolute insane and will not end well, as markets can turn suddenly and violently when extreme levels are reached.

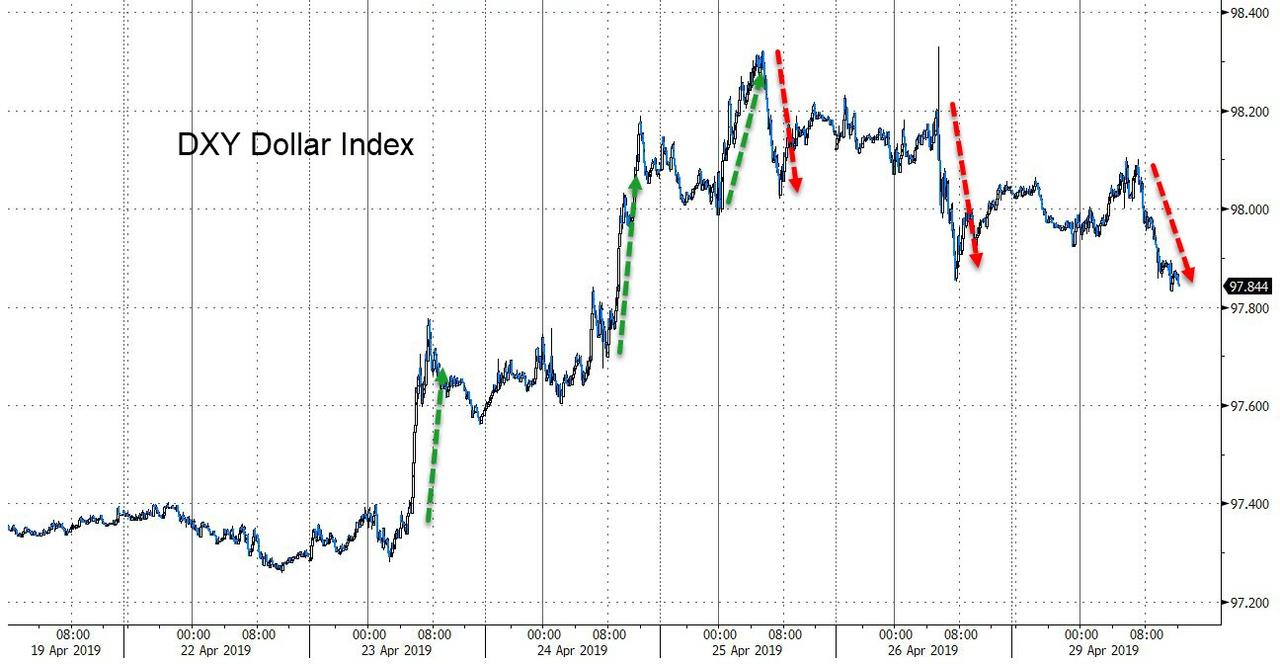

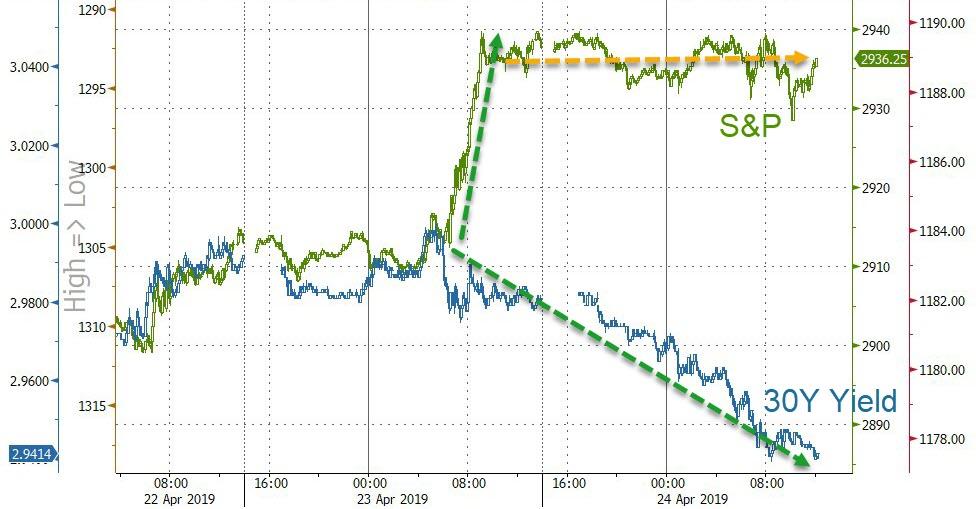

Rising rates pulled interest rate sensitive sectors, such as low volatility equity and Real Estate ETFs a little lower, with the US Dollar joining the party and losing some of its luster as well, although the slide was modest.

On the economic front, we saw that consumer spending jumped 0.9% in March, its largest monthly gain in almost 10 years. Allegedly, core inflation weakened, leading traders to conclude that the Fed will not yet be motivated to change its interest rate policy.

Yet, at the same time, the US savings rate plunged, while YoY spending has accelerated beyond income growth. Yes, that is only possible because of the never-ending use of credit.

Go figure…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}