- Moving the markets

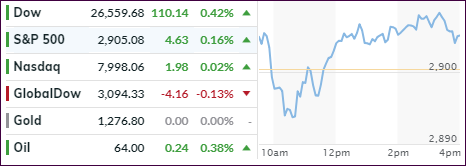

The major indexes, led by the Dow, made another attempt at breaking into record territory but failed with upward momentum lacking. Trading volume was the lowest in months meaning there was not much conviction to drive the markets higher. The theme was a repeat of what we’ve seen over the past five trading day with the direction being more sideways than up.

To wit, here’s what the S&P 500 did: 2,907, 2,906, 2,907, 2,900, 2,905.

That is not exactly a representation of a bullish market but more of one with questionable durability. Or, it could simply be a matter of Wall Street having the Easter Holiday blues. Be that as it may, next week all traders should be back on the job, and we will see if “buy” or “sell” buttons will be pushed.

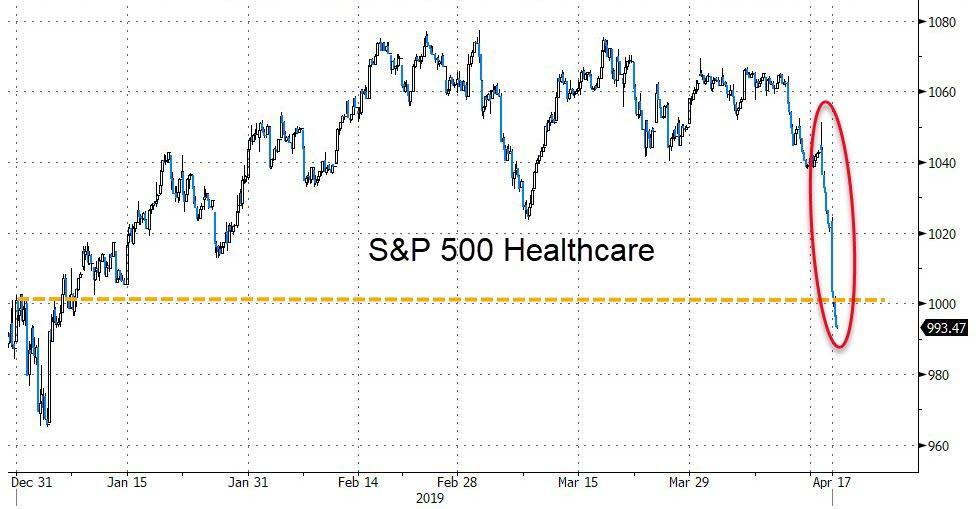

Healthcare and Small Caps suffered the most this week, while the tech sector continued its role as the best performer of the year. The only potential fly in the ointment is that tech has now reached 19.2 times forward 12-months earnings, a level that was last seen in 2007, as ZH pointed out.

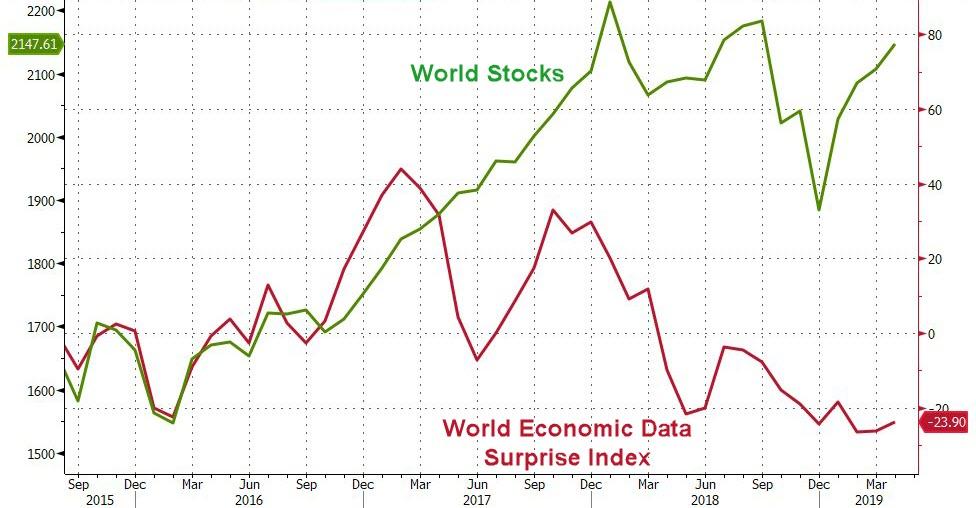

Looking at the big picture, I never get tired of looking at this chart, which demonstrates the discrepancy between the Economic Surprise Index and the S&P 500. Today, one line has been added, namely the Global Money Supply, which clearly shows who is behind the ferocious rebound from the December 2018 lows.

Makes you wonder how long this can go on, doesn’t it?

Enjoy the Easter weekend.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}