Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 157 (last week 199)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

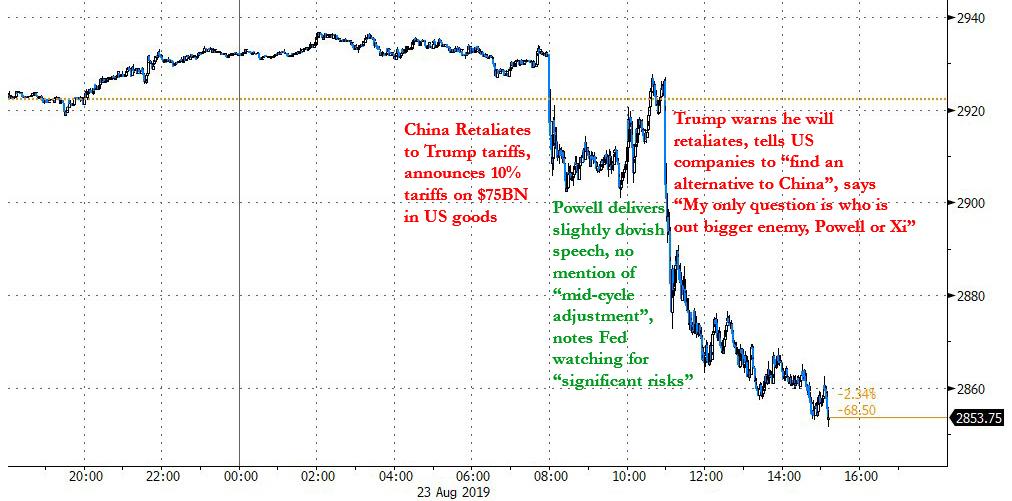

To be fair, it wasn’t just Fed chief Powell’s

Jackson Hole speech that put the markets in a sour mood. The hammer came down hard,

after Trump unleashed a verbal tirade, first towards the Fed:

As usual, the Fed did NOTHING! It is

incredible that they can “speak” without knowing or asking what I am doing,

which will be announced shortly. We have a very strong dollar and a very weak

Fed. I will work “brilliantly” with both, and the U.S. will do great. My only

question is, who is our bigger enemy, Jay Powel or Chairman Xi?”

If that was not enough, he upped

the ante in response to China’s threat to levy new tariffs on the US:

“We don’t need China and, frankly, would

be far better off without them“, and ordered “Our great

American companies… to immediately start looking for an alternative to China,

including bringing your companies HOME and making your products in the

USA.”

“I will be responding to China’s Tariffs this

afternoon.”

Not much else was needed to shift the

computer algos and traders into selling mode and down we went. There was no looking

back with all major indexes closing deeply in the red, and that reaction did not

even include Trump’s mystery “afternoon” announcement.

The war of words can’t get much uglier, and

we may see more fallout next week when the rhetoric is sure to continue. In the

meantime, the G-7 meeting is on deck for this weekend in France. Last time, the

get-together was such a disaster that the seven nations could not even agree on

a common communique. I don’t expect much more this time.

This week’s wild swings in the market have left

their mark on our Trend Tracking Indexes (TTIs). As posted, the International

one headed into bear market territory on 8/15/19, while the Domestic one bounced

off its trend line and has held steady until today.

The Domestic TTI has now slipped slightly

below its long-term trend line (see section 3) and may very well signal a move to

the sidelines next week. We are also approaching the notoriously volatile month

of the September, where anything is possible.

ETF Data

updated through Thursday, August 22, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

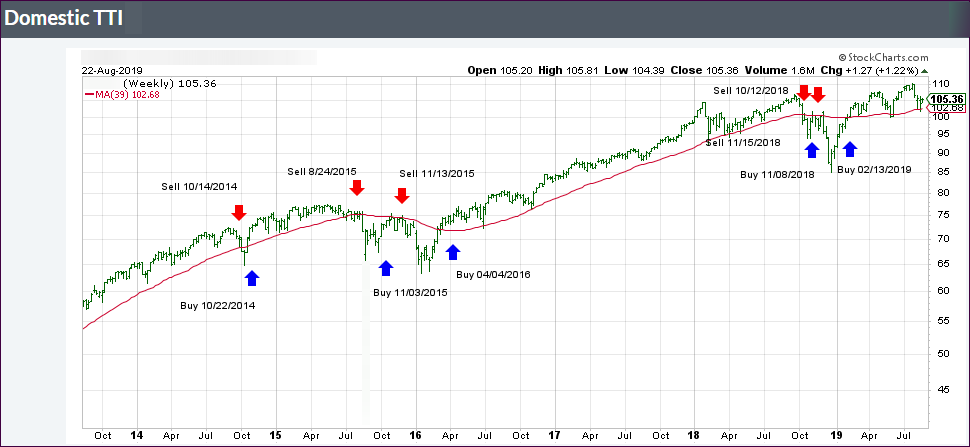

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +2.83% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

An early rally fizzled, as

uncertainty over the outlook of interest rates kept traders on edge, especially

due to the upcoming Fed statement regarding the Jackson Hole meetings. I think

Fed head Powell’s position on rates is well known, and his upcoming speech on

Friday is likely to disappoint those hoping for more dovishness.

Not helping the markets was

an announcement by the German Bundesbank proclaiming that “they don’t see a

need right now for fiscal stimulus at this time, even though they expect the

economy to shrink again this quarter.”

That was totally opposite of

what was expected, and markets started to sag. Then another hawkish nightmare

appeared out of nowhere when the Fed’s Patrick Harker opined in an interview

that “he doesn’t see any need for further stimulus at the moment.”

Some of his soundbites included:

“Yield

curve is only one of many signals.”

“Trade

issue makes business decisions difficult.”

“Growth

now is exactly what we had anticipated last year.”

“No

need for another rate cut, central bank should stay here for a while.”

“Trade

resolution would boost growth.”

Ouch. That was not exactly

what traders had hoped for, so the markets continued riding the range but

managed to eradicate some of the early session losses.

Nevertheless, Fed chair

Powell is set to deliver a speech tomorrow, during which investors will be eagerly

looking for clues as to whether another rate cut will be on deck for September.

Good earnings by consumer

heavyweights Target, Lowe’s and Home Depot set the bullish mood early on and pushed

equities up to a level that they sustained throughout the session. All of yesterday’s

losses were wiped out with the S&P 500 closing exactly at Monday’s price.

The Fed minutes did not

offer any earthshaking news other than to confirm that the July rate cut was simply

insurance for growth and inflation and considered to be a mid-cycle adjustment.

It’s supposed to help counter the effects of weak global growth and trade

uncertainty.

Good economic news came from

housing sector, as we learned that Existing Home Sales rose YoY

and thereby breaking a 16-month losing streak. They came in at +0.6%, while the

median sales price also advanced by 4.3% from a year earlier.

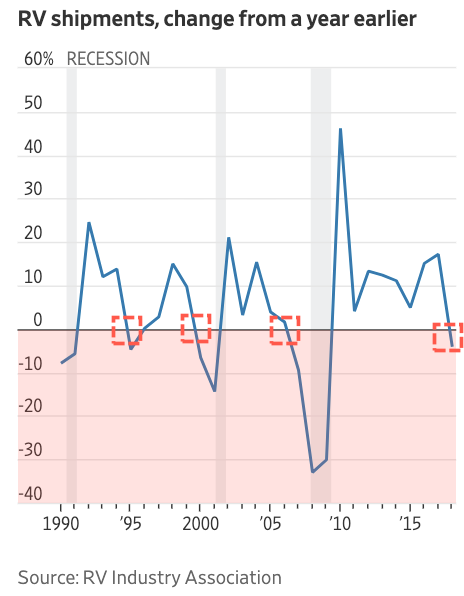

Offsetting this good news

were reports that the RV industry crashed with domestic shipments

to dealers plummeting 20% so far this year, after dropping only 4% for the entire

year of 2018. Ouch.

On the global scene, Germany

attempted to sell the world’s first 30-year negative yielding bond (-0.11%), which

failed miserably. When the dust settled, it turned out that only 824 million

Euro of the total 2 billion Euro offering were sold with the Bundesbank now

being forced to retain the unsold portion. That’s a big ouch. After all,

government bonds need to be sold to cover the ever-growing deficits.

For the week, we saw that Monday

was up, Tuesday was down, and Wednesday was up. This rollercoaster may very

well continue until the bankers’ Jackson Hole meeting ends on Friday, or the weekend

G-7 meeting results, or lack thereof, make their presence felt on Monday.

Numerous attempts by the major

indexes to break above their respective unchanged lines were rebuffed, as they

ended up diving into the close and breaking a 3-day win streak.

Despite Home Depot’s better than

expected quarterly results, the markets struggled for altitude all day with

worries about the strength of the US economy, along with political developments

in Europe (Italy’s prime minister resigned), weighing on government bonds.

The US 10-year yield slipped

again by 6 basis points to 1.55%. In the meantime, Trump continued his assault

on the Fed by asking to consider deeper cuts, something like 1%. This contradicts

the widely advertised view that we have the “best economy ever.” Well,

if we did, interest rates would be rising and not declining, as they have been.

After the 3-day rally,

uncertainty affected the mood on Wall Street, as Friday’s speech by Fed head

Powell looms large, and you can be sure that every word will be dissected when

the bankers’ conference in Jackson Hole ends.

For hints of things to come,

traders will be busy analyzing the minutes from the Fed’s July policy meeting,

which will be released tomorrow. I expect a wait-and-see attitude to keep the

indexes in check till Friday.

{kind=link}

{kind=link}

{kind=link}