Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 203 (last week 221)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

The

entire week has been a roller coaster ride, as stocks tried to find some

support but ended up on the downside with the Dow now extending its losing

streak to five straight weeks, its worst one since June 2011.

An

early morning rally stoked bullish sentiment following reports that Trump was considering

easing up on restrictions against Huawei Technologies as “some part” of a larger deal with China.

That

helped, even though tensions between the two countries have increased and a move

away from an amicable trade deal seemed a foregone conclusion, as Trump again

confirmed the Chinese company to be “very

dangerous” from a security perspective.

Despite

the major indexes closing in the green, and the session featuring a pump, dump

and recovery theme, the S&P 500 lost -1.2% for the week. It looks to me

that markets will continue to be overly sensitive and reactive to any trade

news, and it appears that we are at times taking one step forward to be

followed by two steps back.

While

the focus is and likely will remain on the U.S.-China trade war dispute,

the real elephant in the room is global growth, which will only improve once

global and U.S. economic data show signs of steadiness. Today’s tumble in durable

goods was not a start in the right direction.

You

can easily see that things are not going the right way economically by

observing the bond market. The yield on the 10-year tumbled

and has done so for the past five weeks out of six. Today it closed at 2.32%,

its lowest since October 2017. If the economy was rip-roaring, we would have rising

rates and not falling ones.

As

ZH pointed out, the Fed now has a problem:

How’s it going to be

able to support the market (with lower rates) when investors are already pricing

in 45 bps (0.45%) of rate cuts for 2019?

It appears that the market

thinks the recession has already started.

Right

now, our Trend Tracking Indexes (TTIs) still support the bullish theme; but only

by a small margin. It would not surprise me to see that change soon, as our

International TTI, which usually functions as the proverbial canary in the

coalmine, is already motioning that a ‘Sell’ signal may be forthcoming.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

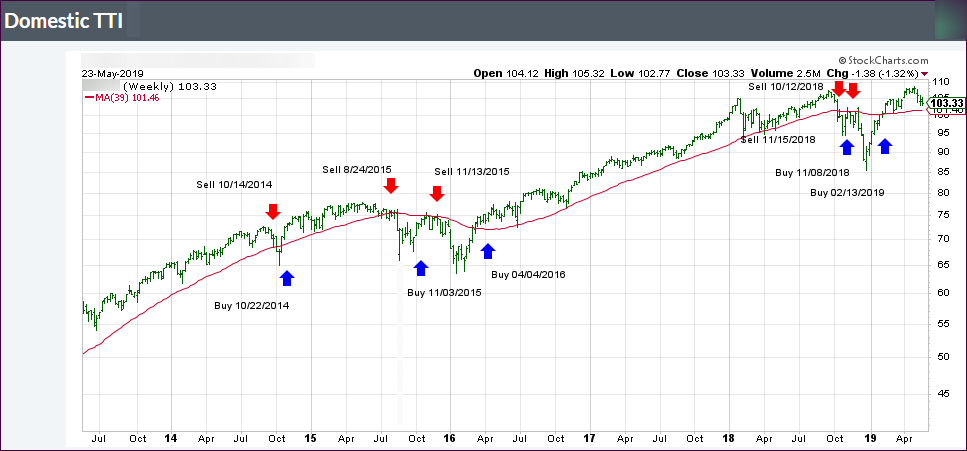

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +1.80% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

There

was nothing for the computer algos to be optimistic about, as far as uplifting

news headlines was concerned. There simply weren’t any, and the Dow started the

session with a 400-point drop and ended up below

its 200-day M/A for the first time since the beginning of the year.

Even

a hint of a rebound was quickly wiped out, as traders worldwide seemed to have

finally gotten the idea that the widely touted trade deal had bitten the dust,

and a protracted U.S.-China confrontation has morphed into a lengthy standoff. These

increased frictions weighed heavily on the markets in general and on the tech

sector specifically.

The

jawboning between the countries went on with China stating the talks would only

continue when the U.S. adjusts its “wrong

actions,” etc., etc., etc. with the tit-for-tat sinking to new lows.

None

of this helped equities, which were struck be several economic data misses. New

home sales collapsed in April, despite a soaring median price, even though

they were expected to slide only -2.5% but instead plunged -6.9% MoM after an upward

revision for March.

Business

Confidence followed suit by tumbling to 7-year lows, while Crude

Oil crashed to 2-month lows, likely as a result of trade tensions reducing

hope for a revival of global growth.

The

bond market was in panic mode, as yields plummeted with the 10-year

touching 2.29%, the lowest since December 2017, as traders moved out of equities

and into the perceived safety of bonds.

During the last 30 minutes of trading, some dip buyers showed up to pull the indexes off their lows, but it was not enough to affect the sea of red we witnessed all day.

After

yesterday’s strong rebound, the markets opened on a weak note with the major indexes

spending the entire session below their respective unchanged lines trying to

find some footing.

Not

helping matters early on was a worsening of trade relations with China, which to

me has now morphed into an all-out trade war, as a Chinese

company has told all of its employees to boycott American products and halt

international travels to the U.S. That kept the markets on a slippery footing

until the Fed released its minutes on interest rates from its last meeting.

The

Fed, as expected, revealed that their members are comfortable being “patient” on their current stance on interest

rates, a position which could last “for

some time.” While officials were split on the rate outlook over the long term,

no one wanted to rock the boat “and push

for a near term policy shift in either direction.”

In

the end, the Fed’s announcement was not enough to keep the bears in check, and,

after a mid-day rally, we dove into the close with selling picking up due to

the White House ramping up its trade war rhetoric.

Where

do we go from here? While our Trend Tracking Indexes (TTIs) continue to support

the bullish theme, there are two indicators, which are flashing warning signs.

The first one, thanks to Bloomberg, is a Boom-Bust

indicator charted against the S&P 500, while the second one is the Global

Money Supply Index.

Both

are forecasting a potential decline in stocks, however, as always, the timing

of it is the big unknown. For that, we will rely on our Trend Tracking Indexes

(TTIs) to point the way towards the exit doors, once the need arises.

The

White House walked back some of its tough talk last night by announcing that they

are offering some temporary exceptions to export limitations against China’s

Huawei Technologies. While the mudslinging continued, it was enough of a

conciliatory gesture to soothe the anxiety among Wall Street traders, which had

been focusing on pressing the sell buttons all day yesterday.

Dip

buyers emerged and drove the major indexes to some solid gains, with especially

the Nasdaq recouping some of yesterday’s sharp losses. Support also came from a

short squeeze in SmallCaps, as this

chart shows.

The

fallout from yesterday’s threat by the Chinese to curtail the export of rare-earth

minerals was immediate, as China’s rare

earth holdings catapulted some 132% in a market that does not have upside/downside

price limits.

On

the domestic front, the news was not good, as existing

home sales tumbled YoY for the 14th month. Expectations had called

for a +2.7% rise in April, which was not even close, as reality showed a decline

of -0.4%, which comes after a shocking -4.9% drop in March. At least for today,

this “bad” news was good news, as the bullish market theme was not even interrupted

to let this realism set in.

Let’s

see if this comeback has legs, or if it is simply a “one-off” in a market that

is predominantly headline driven.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}