1. Moving the markets

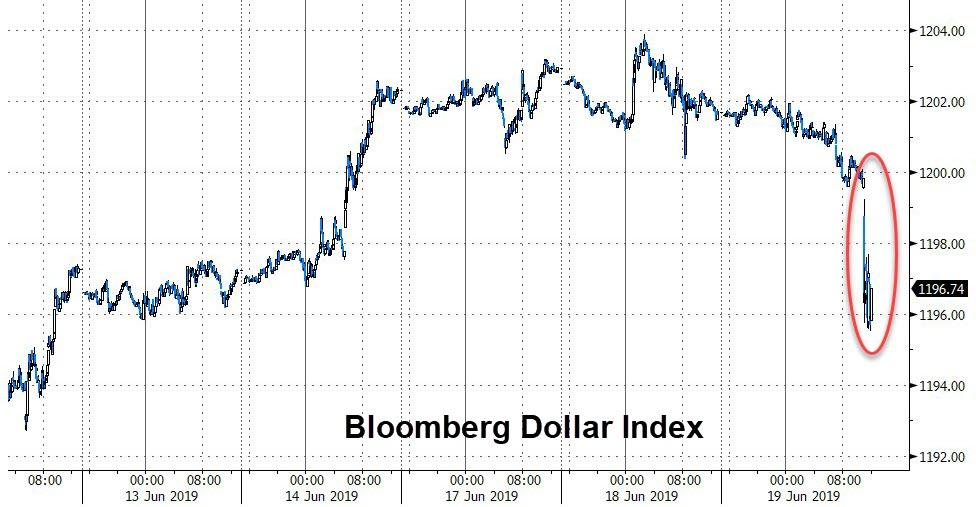

After sleeping on the Fed’s statement on interest rates, Wall Street traders decided that the Fed left the door somewhat open to a rate cut. As a result, expectations soared from 80% to 100% that the Fed will “cut” in July.

That was enough for the major indexes to gap higher at the opening with the S&P 500 setting a new intra-day all-time high in the process, while taking another giant step towards conquering its $3k milestone marker.

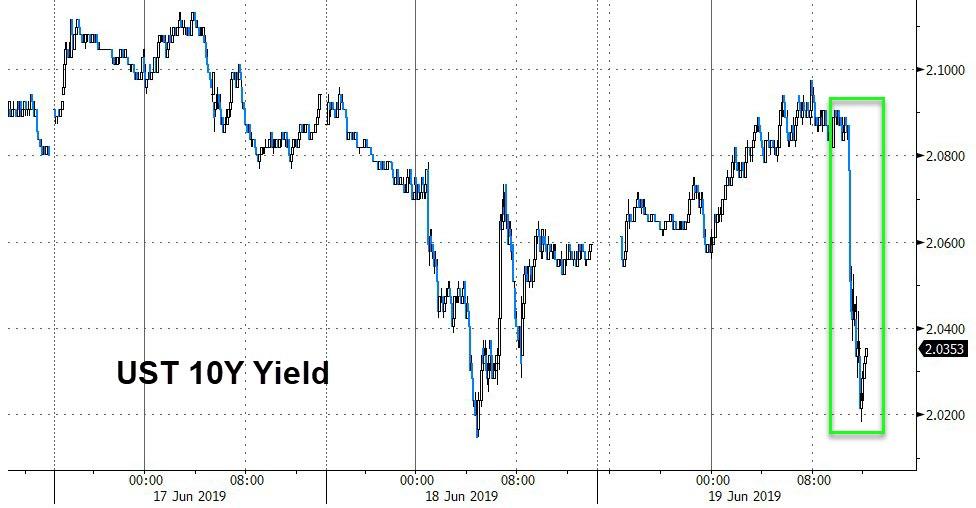

A mid-day dip did nothing but encourage more bulls to jump aboard this pause in upside momentum, and up we went notching new highs for the session prior to the close. Bond yields headed lower again, with the 10-year barely hanging on to the 2% level, although it dipped below it intra-day.

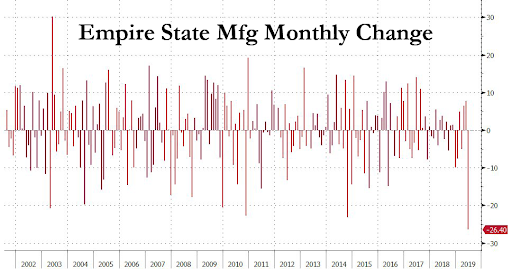

While most of the attention was on the Fed, it’s important to note that tomorrow is quadruple option expirations day, which can cause the markets to move violently in either direction prior to expiration time. I think a great deal of today’s upward ammo came from that looming deadline.

Also helping today’s bullish cause was a report that the warring parties in the U.S.-China trade dispute have decided to get together again, with the U.S. delegation traveling to Japan next week for “preliminary” meetings.

As I have posted before, the rise of the global money supply has been a terrific indicator as to the overall direction of equities. It has surged once again and has been a major contributor to rescuing the markets after the very destructive month of May, during which the S&P 500 lost -6.6%.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}