Well, it sure didn’t take

much effort to keep the markets going, as Trump successfully dangled the trade

carrot again via this tweet:

“Big day of negotiations

with China. They want to make a deal, but do I? I meet with the Vice Premier

tomorrow at The White House.”

While this did not indicate

really anything, the computer algos saw it as a positive, since China’s chief

trade negotiator Vice Premier Liu He is staying in town till Friday, at least

for now. That was all it took to ramp the markets higher in a vain attempt to get

back to even for the week.

However, a US-China deal is

based on nothing but hope, because as ZH noted correctly:

“The US has not changed

its extensive and rigorous requests for China, nor has it responded to China’s

core concerns,” Renmin University international relations professor Shi

Yinhong said.

“Even if there is a deal, it

could only be a mini-deal, even a minimal mini-deal. A currency pact, if true,

does not bring any substance.”

But optimism is all that

matters, so we’ll have to wait and see how this movie plays out. Given recent history,

this could very well turn into another head fake.

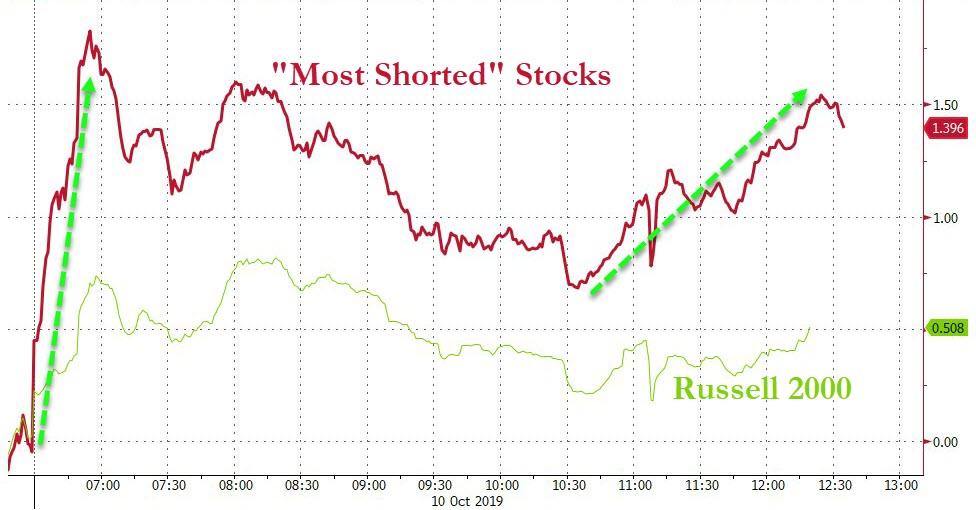

In the meantime, the major

indexes managed to whipsaw around above their respective unchanged lines and scored

another winning session for the second day in row, which was in part supported

by a short

squeeze in SmallCaps.

Still, the S&P 500 needs

to gain about 1.3% from today’s level in order to reach last Friday’s close.

It seems like yesterday’s trade

jawboning between the US and China had taken on too harsh of a tone, so both parties

attempted to ease festering tensions. News reports indicated that China was open

to a “limited or partial tariff solution” while offering to increase purchases of

agricultural products from US farmers to $50 billion.

That was enough of a driver

to push the indexes higher, despite weak domestic data showing Job Openings

plunging to a 17-month low and confirming that Hiring/Quitting continues to remain

on a slippery slope.

Then the Minutes from the last

FOMC meeting on interest rates showed that officials have become somewhat concerned

about the state of the economy with some members arguing that the chances of a

U.S. recession “had increased notably in recent months.”

While that is a negative, it

is not one in today’s environment, where stock market levels are largely supported

by ever decreasing interest rates. And, a recessionary environment pretty much guarantees

that rates will head lower, which is exactly what the markets anticipate when the

Fed meets later this month.

While today’s rebound

encouraged the bullish crowd, it’s noteworthy that this activity was

accompanied by very low volume, about 30% below average, which means the rally

was lacking conviction and may not have enough legs to continue.

Be that as it may, our Trend

Tracking Index (TTI), after slipping below its long-term trend line yesterday, mustered

enough strength to climb back above it by +0.49% indicating, at least for the

time being, that the bullish trend is still alive.

After the Chinese offered

not much hope for a successful outcome of the upcoming trade meeting, today it

was the US’s turn to up the ante by blacklisting 28 Chinese companies due to

alleged human-rights violations against Muslim minorities.

Should this mutual hostility

fest continue, Friday’s scheduled high-level trade meeting might be over before

it even starts. So, it came as no surprise that the markets sold off sharply,

as “trade hope” has been one of the constant drivers of equities.

Then Fed head Powell

attempted, with modest success, to levitate equities by announcing something that

sounded like QE (Quantitative Easing) but wasn’t given that name. Here’s part of

what he said:

While a range of factors may

have contributed to these developments, it is clear that without a sufficient

quantity of reserves in the banking system, even routine increases in funding

pressures can lead to outsized movements in money market interest rates. This

volatility can impede the effective implementation of monetary policy, and we

are addressing it.

Indeed, my colleagues and I

will soon announce measures to add to the supply of reserves over time.

Consistent with a decision

we made in January, our goal is to provide an ample supply of reserves to

ensure that control of the federal funds rate and other short-term interest

rates is exercised primarily by setting our administered rates and not through

frequent market interventions. Of course, we will not hesitate to conduct

temporary operations if needed to foster trading in the federal funds market at

rates within the target range.

“I want to

emphasize that growth of our balance sheet for reserve management purposes

should in no way be confused with the large-scale asset purchase programs that

we deployed after the financial crisis.”

ZH supplied the rough translation

of the above:

Don’t confuse balance sheet growth for “reserve management” with balance sheet growth for “stock market management.”

While that helped equities to regain some footing, it was short-lived, as Trump stepped up by announcing notable actions against human rights abusers in China, which just about destroyed any gains from Powell’s talk and furthermore may have put a big temporary nail in the trade coffin.

Stocks had enough of this

and south we went in a hurry with the major indexes closing not only at new

lows for the day but also hitting critical technical levels.

For the last 1.5 years, ZH

has been tracking current market direction compared to events leading up to the

crash of 1987, as this

chart shows.

While history may not repeat,

the above chart makes a solid case, that it may. Additionally, our main directional

indicator, the Domestic Trend Tracking Index (TTI), pierced its long-term trend

line to the downside today by -0.39% for the first time since February.

While this is only a scant piercing,

it nevertheless indicates that tough times for stocks could be ahead. I will watch

developments closely, and if more weakness persists tomorrow, will start liquidating

some of our more volatile holdings with the remainder being on the chopping block

soon thereafter.

I would not be the least bit

surprised, given current and recent chaotic events, if we find ourselves back on

the safety of the sidelines very soon and watching the markets self-destruct.

An early drop was followed

by a pop above the unchanged line but in the end, equities simply ran out of steam

with the S&P closing at its lows for the session.

Early words of hope regarding

the always uncertain US-Trade relations managed to pull the markets higher, but

even the often confused computer algos must have interpreted that as nothing but

hot air, and down we went.

Of course, uncertainty reigned

supreme with high-level tariff negotiations between Washington and Beijing being

on deck for later this week. Setting the tone were Chinese officials, as they expressed

reluctance to hammer out a broad agreement in Washington this Thursday and Friday.

The market

odds seem to support that view.

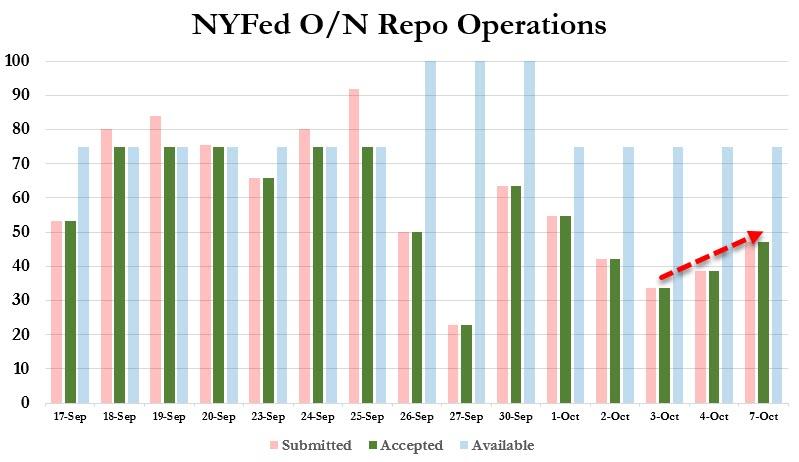

I have commented on the rather

complex inner workings of the overnight repo market, as well the fact that some

of the financial plumbing appears either not to be not working or has simply

broken down. ZH presented this chart

showing that, despite the last quarter being over, the problems continued, as

repo demand has picked up again.

As I posted before, a short-term

disconnect is nothing to worry about, but we’re now past the point of a temporary

assist by the Fed, and I will watch closely if this will turn into a precursor for

more weakness in equities.

On a personal note, I will not be posting today and Friday. This time it’s not a business issue, but a personal one. My wife and I will be traveling to San Diego to be part of my son’s wedding. I will, however, monitor the markets and adjust our holdings, should that become necessary. Regular posting will resume this coming Monday.

I mentioned yesterday that our International Trend Tracking Index (TTI) had crossed its long-term trend line to the downside by -2.00%.

This morning, it took another steep dive thereby clearly heading deeper into bear market territory, which means a ‘Sell’ signal, effective today, has been generated.

As I posted at the time of the ‘Buy’, I did not participate in this cycle due to us being 100% invested in the domestic arena.

If you are following my methodology, this means that all “broadly diversified international funds/ETFs” should no longer be held.

{kind=link}

{kind=link}

{kind=link}

{kind=link}