An early slide managed to gain

some traction, followed by a small rebound that had the S&P 500 hugging its

unchanged line throughout most of the session, before a last-minute pump pushed

the index into the green by a tiny margin.

The outlook for interest

rate reductions later this month has become clouded, thanks to last week’s stronger

than expected June jobs report, but Wall Street traders still are clinging to hope

that a 0.25% cut will materialize.

While the whisper number was

a 0.5% reduction, which had been largely priced in, it makes anything less question

traders as to the success of such an effort. Remember, Wall Street is spoiled

and addicted to lower rates, without which a continuation of the bull market

becomes questionable. We saw the result of a disappointing Fed by the market reaction

last year.

In the end, the markets did

nothing and may not move much in either direction until the Fed clarifies its

policy. With this having been a relatively quiet day, ZH decided to post the

current S&P performance when overlaid

on the 1987 market debacle.

All session long, the major

indexes were stuck below their respective unchanged lines, as uncertainty about

the much anticipated and expected rated cut by the Fed later this month kept equities

in check.

After all, we are only a few

steps away from all-time highs, traders believe we are in a strong economic environment,

despite evidence to the contrary, and want a rate cut so that stocks can continue

to rise ad infinitum. The July rate-cut odds remain at 100%, as this

chart shows.

Besides rate cut hopes being

questioned, all eyes are on Fed chair Powell on Wednesday when he testifies

before Congress on the state of the US economy as well as monetary policy. He

will then also speak before the Senate on Thursday, but most likely his speech will

be a repeat. Nevertheless, every one of his words will be dissected to analyze

what he really meant to say.

In the stock arena, Boeing proved

to be a drag on the Dow, due to the Saudis cancelling a $5.5 billion order, while

Apple

suffered as well, after an analyst downgraded the company from ‘neutral’ to ‘sell.’

Ouch!

With all the hype surrounding

the rate-cut scenario, I wonder what will happen to equities if the Fed disappoints

and does nothing? Consider, there is no Fed meeting in August, so the wait till

September could give the bears a reason to do some serious chest pounding.

Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 279 (last week 276)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

GOOD NEWS IS BAD NEWS AGAIN—BOND YIELDS EXPLODE; EQUITIES

TUMBLE AND RECOVER

[Chart courtesy of MarketWatch.com]

Moving

the markets

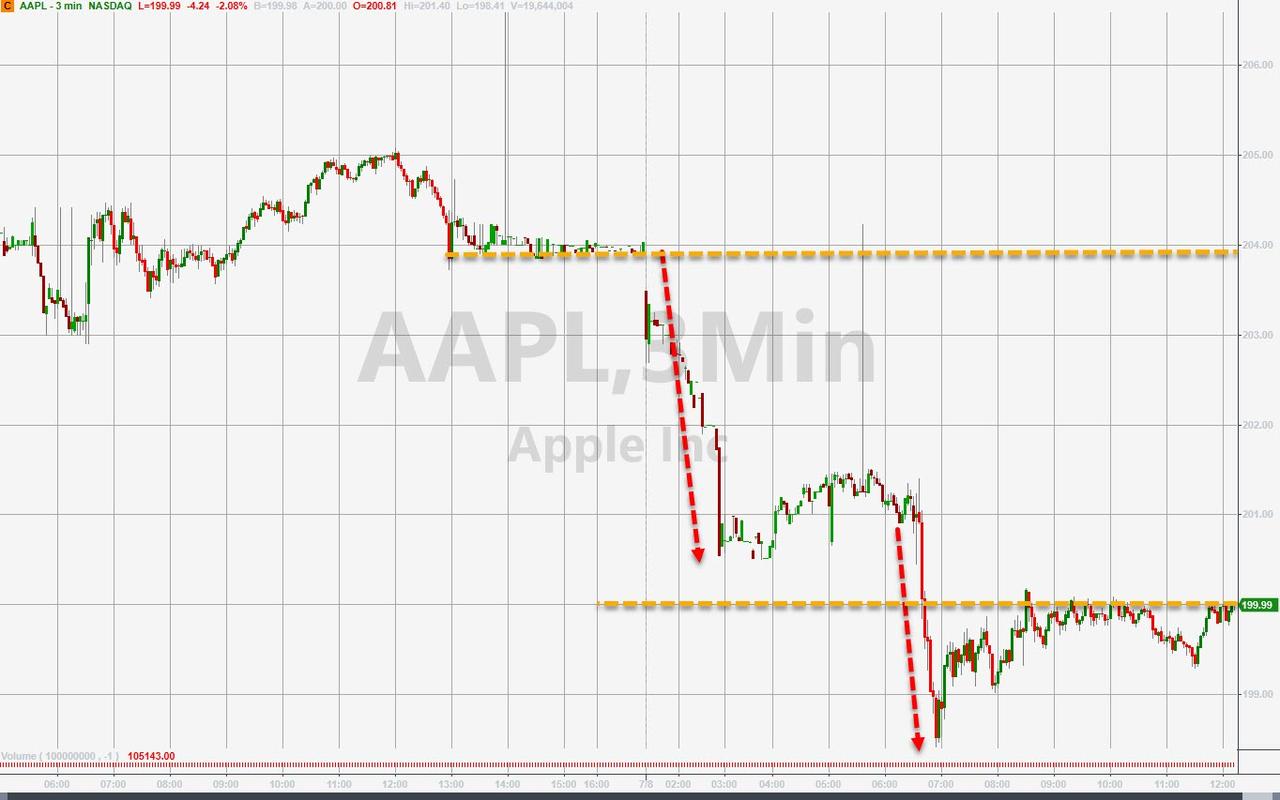

As we’ve seen many times in the past, good economic

news turned out to be bad news for equities, which took a steep dive at the

opening after a better than expected jobs report. We learned that 224k new jobs

were added, which was an easy beat of the 170k expected.

Wall Street viewed this as a negative development

because it endangers, or at least puts in question, the widely anticipated rate

cut by the Fed later this month. At session lows, the Dow had dropped some -0.8%

with the other major indexes showing similar losses.

At the same time, bond yields, which had been on

a downward trajectory, exploded higher with the 10-year at one point being up 11

basis points and solidly back above the 2% level. That is a huge move, as this

chart demonstrates.

The ensuing rebound pulled yields back down a

tad, but we still closed higher by over 9 basis points, while in the equity arena

the losses were reduced sharply with only the safe- haven arena, namely gold,

suffered a loss of over 1%.

ZH summed up the week as follows:

Trade-Truce ‘good’ news was good

news for stocks, ‘bad’ news in macro data this week was good for

stocks, and jobs ‘good’ news today was bad news for stocks

(initially)…

Be that as it may, despite a Holiday shortened week,

the major indexes closed higher with the S&P 500 adding +1.7%. Of course, it

all happened on low volume, so we’ll have to wait till Monday, when the big boys

return, and we’ll find out if there is more fallout from today’s jobs report waiting

in the wings.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

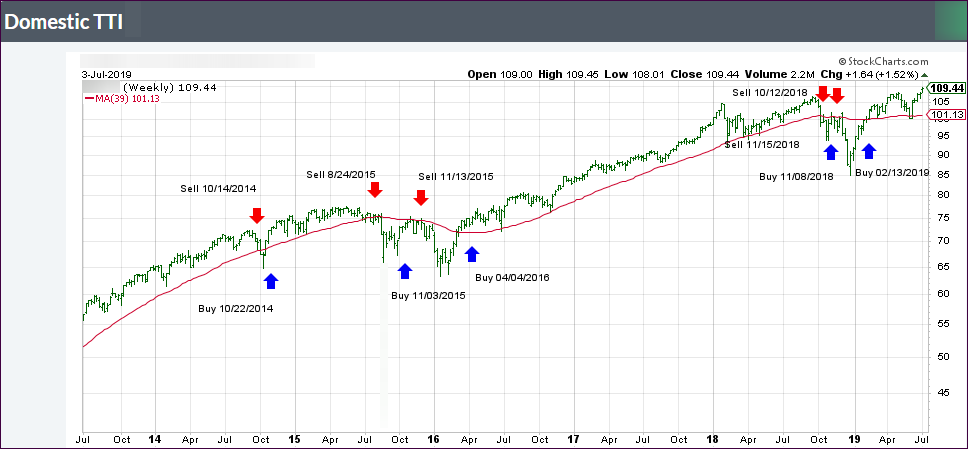

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +8.37% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

The link

below shows all High Volume (HV) Domestic Equity ETFs. The sorting order is by

M-Index ranking. Prices in all linked tables below are updated through 07/03/2019,

unless otherwise noted. Price data not yet available at publication is

indicated with 00.00% or -100.00%. Please note that distributions are not

included in the current momentum numbers.

Whenever the

TTI is above the trend line, and therefore in “Buy” mode, you can either use

the tables in the link below to make your selections or choose from the 10 ETFs

in the Spotlight, which are featured daily as part of the market commentary:

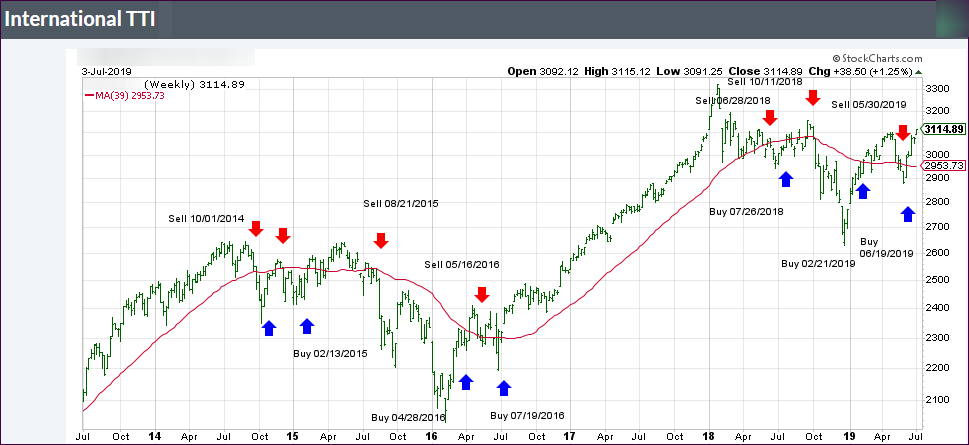

The

International Trend Tracking Index (green) has now moved +5.49% above its

long-term trend line (red). The new ‘Buy’ signal went into effect on 6/19/2019.

The listings

in the link below represent the High Volume (HV) International ETFs I track to

be used during a Buy cycle. They are sorted by M-Index ranking:

This ETF

Master list shows the total of all ETFs listed, which allows you to get a quick

overview of leaders and laggards. The sorting order is by M-Index. Momentum

figures for all ETFs are not adjusted for dividends.

The link below

contains a list of HV ETFs for countries/regions, which I am tracking weekly.

Please note that data in this table does not include adjustments due to

distributions.

Country

funds, especially over the past few years, have been volatile. So, the use of a

trailing stop loss (I use 10%) is imperative to protect your portfolio from

severe downside moves.

5. SECTOR ETFs: SELECTIVE

BUY

To diversify

our portfolios, we always need to look for different opportunities to invest

our money. The table of HV Sector ETF listings in the following link covers a

broad spectrum of possibilities. The sorting order is by M-Index:

Here too, I

recommend the use of a 10% trailing stop loss to minimize the risk.

6. BOND & DIVIDEND ETFs: SELECTIVE BUY

If you

prefer using ETFs for the generation of income, here’s a list of bond and

dividend paying ETFs. It’s important to first look at how these instruments

have held up in terms of momentum figures. Then you should visit your favorite

financial web site to examine yield and other details.

Please note

that data in this table does not include adjustments due to distributions.

Please note

that some of the above funds try to outperform the index they are tied to by

the percentage stated. While this can enhance your returns, it can certainly

accelerate your losses as well. No matter which way you choose, be sure to work

with a trailing sell stop (I suggest 10%) and be aware that volatility will be

your constant companion.

8. NEW SUBSCRIBER INFORMATION

To get a

head start on more successful investing, please click on:

In case you

missed it, you can download my latest e-book “How to beat the S&P 500…with

the S&P 500,” here. If you are investing

your 401k and must use mutual funds, I suggest you primarily stick with the

S&P 500 as described in my book. Of course, you can always use the above

tables to find sector or country ETFs to your liking and use the equivalent

mutual funds as offered by your custodian.

Disclosure:

I

am obliged to inform you that I, as well as my advisory clients, own some of

the ETFs listed in the above table. Furthermore, they do not represent a

specific investment recommendation for you, they merely show which ETFs from

the universe I track are falling within the guidelines specified.

Despite most Wall Street traders being gone this week,

the S&P 500 is heading towards its 3,000 level—on very low volume. With only

another hour to go, because of a shortened session, we may very well see this milestone

being hit.

I have a few commitments this afternoon and will not be able

to write today’s report. Regular posting will resume Friday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}