ETF Tracker StatSheet

You can view the latest version here.

GDP SLOWS BUT BEATS EXPECTATIONS

- Moving the markets

All eyes were on the latest release of the second quarter GDP report, and it did not disappoint. While we saw a slowdown from the torrid pace of 3.1% per annum set in the first quarter, the 1.9% expectation was easily beat with the economy growing at 2.1% per annum in the second quarter. The fly in the ointment was that corporate profits dumped to an 8-year low.

While this number is sure to be revised again, for right now, the computer algos saw ‘good’ news as ‘good’ news, and the major indexes rose to new intra-day record highs with the Dow being the laggard again.

This better-than-expected GDP number is sure to give the Fed some headache when it comes to next week’s decision as to whether to lower rates, and if so by how much, or stay put. After all, they see inflation data as mild, which leaves them with the question “are we really seeing a slowdown that justifies further easing?”

The Nasdaq led all the way by gaining +1.11% followed by the S&P 500 with +0.74%. More than 40% of the S&P 500 companies have now reported quarterly earnings, so the earnings race will continue next week.

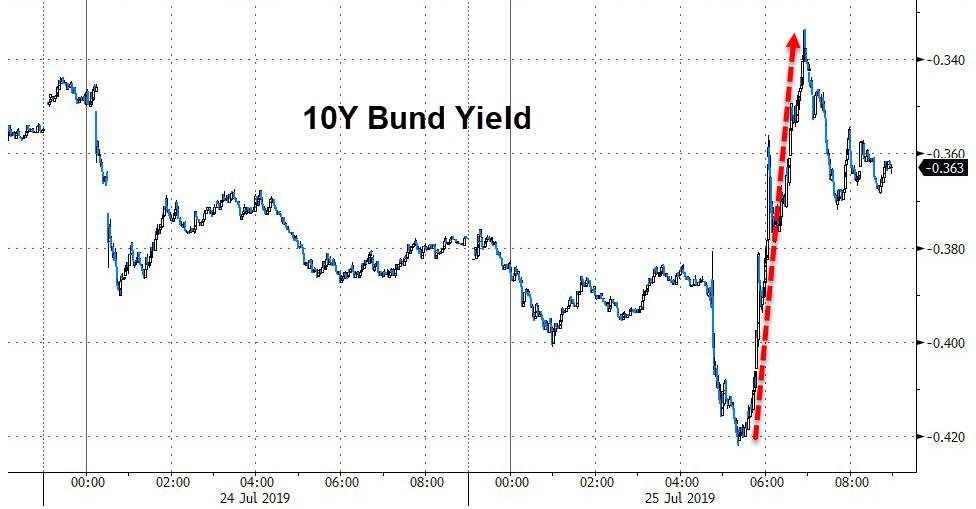

Quipped ZH regarding the Fed: Let’s hope that Powell delivers, because global liquidity is starting to diverge again. This chart makes that abundantly clear, while bonds and stocks continue with their own interpretation of divergence.

The Fed will be on deck next Wednesday, and I for one am curious whether the adage “buy the rumor, sell the fact” rears its ugly head again, especially if the Fed indeed turns out to be in an interest rate cutting mode.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}