Numerous attempts by the major

indexes to break above their respective unchanged lines were rebuffed, as they

ended up diving into the close and breaking a 3-day win streak.

Despite Home Depot’s better than

expected quarterly results, the markets struggled for altitude all day with

worries about the strength of the US economy, along with political developments

in Europe (Italy’s prime minister resigned), weighing on government bonds.

The US 10-year yield slipped

again by 6 basis points to 1.55%. In the meantime, Trump continued his assault

on the Fed by asking to consider deeper cuts, something like 1%. This contradicts

the widely advertised view that we have the “best economy ever.” Well,

if we did, interest rates would be rising and not declining, as they have been.

After the 3-day rally,

uncertainty affected the mood on Wall Street, as Friday’s speech by Fed head

Powell looms large, and you can be sure that every word will be dissected when

the bankers’ conference in Jackson Hole ends.

For hints of things to come,

traders will be busy analyzing the minutes from the Fed’s July policy meeting,

which will be released tomorrow. I expect a wait-and-see attitude to keep the

indexes in check till Friday.

Friday’s rebound did not die

today but continued full force thanks to Trump’s successful jawboning about the

trade talks. It was more of a concession towards the Chinese telecom giant Huawei,

which received a 90-day reprieve, during which it can continue to do business

with American companies without needing a case-by-case license.

Reports that Germany may be considering

stimulus measures, to pull up their sagging economy, helped the global mood and

supported equities for that region. Again, fiscal recklessness is always a positive

for equities.

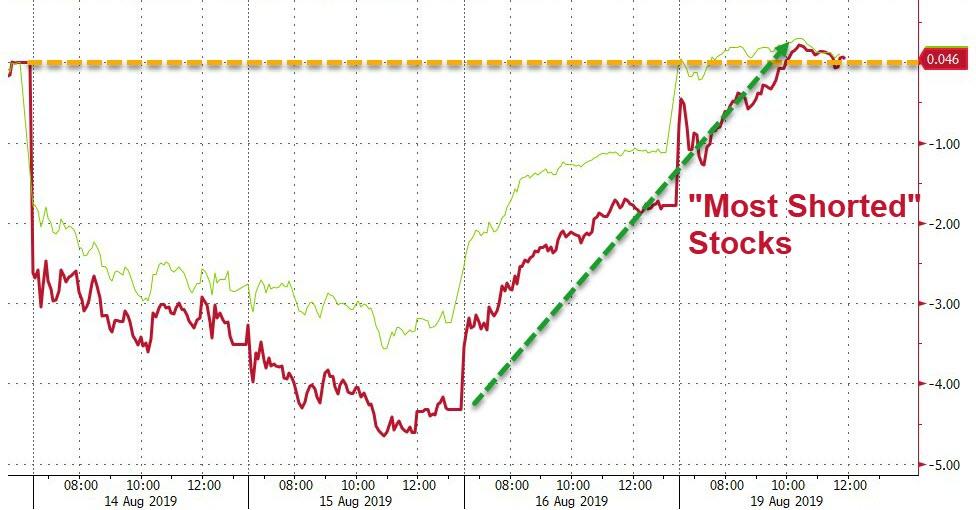

Another big assist came from

a giant short

squeeze, the biggest in 7 months, which started on Friday and kept bulls happy

for the past 2 trading days, as all of last week’s losses have now been

recovered.

In the end, despite slightly

rising bond yields, the mission was accomplished, and the S&P 500 is now

less than 2% away from going green for the month.

Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 199 (last week 206)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

After yesterday’s lackluster session to nowhere,

the markets found some upside momentum, with the ensuing relief rally reducing

some of the losses sustained on Wednesday.

Trying to calm matters was St. Louis Fed

President Bullard’s remarks that inter-meeting action would not be necessary,

referring to the fact that there is no Fed meeting in August, and that a couple

of weeks one way or the other won’t matter.

Then this gag order hit the wires: Fed Chair Powell

has banned any public appearances by any Fed Board member, noting that “appearances

at conferences have been canceled, all scheduled interviews have been abandoned

and any comments on or off the record are outlawed.”

One analyst interpreted this unprecedented

action as a reflection of two pressures:

First, economic indicators increasingly

suggest the US is heading into a recession with the Dow plunging 800 points on

Wednesday.

Second, relations with the White House have

reached a new low, with president Trump pinning the success of his presidency

upon a strong economy as a recession – Trump believes – would destroy his

reputation and kill his reelection chances. As a result, Trump has – correctly

– blamed the current woeful state of the global economy on the Fed. The problem

is that Trump also “owned” the same state of both the economy and the

market for the past two years, so any recession will be entirely his, just as Yellen

(and Bernanke) intended, and shift attention away from the Fed.

On the economic side, data was dire, maybe

that’s why markets rallied, as Consumer Confidence crashed in August to 92.1

from 98.4 missing all forecasts as per Bloomberg’s survey of economists. Then Housing

Starts plunged by a whopping 4.0% MoM and missing expectations for a 0.2% rise.

And that despite tumbling interest rates and rising mortgage applications

But the story of the week was bond yields, with

the 30-year seeing its biggest crash since August 2011, as it fell to a record

low and crossed the 2% level to the downside. As I posted before, the race

to the bottom is on, and lower rates appear to be on the menu, with now $17

trillion of global bonds being negative. It’s only a matter of time until we

get there as well.

That is, unless a Black Swan event suddenly reverses

that trend and catapults yields considerably higher. It looks to me that volatility

and uncertainty will be with us in the foreseeable future.

ETF Data updated through Thursday, August 15, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

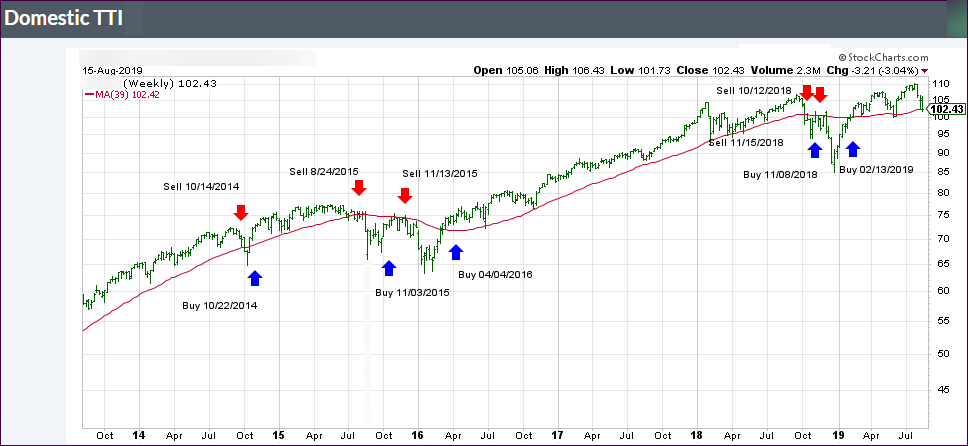

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +0.08% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

The market got an unexpected

assist, which prevented a continuation of yesterday’s slide; at least for the

time being. Retail sales surged in July, but that does not mean all is well, as

these surges

in the past have been followed by contractions. But for this moment in time,

it was a positive with sales gushing +0.7% MoM vs. an expected +0.3%.

Then WalMart delivered better-than-expected

second quarter earnings, as well as same store sales growth, while projecting

even better numbers in the future. We also learned that US productivity increased

2.3% in the last quarter after a healthy 3.5% gain in the first 3 months.

These numbers put the

US-China trade dispute on the back burner, but a spokesman for China’s foreign

ministry seemed to throw out this olive branch:

“We hope the U.S. can

work in concert with China to implement the two presidents’ consensus that was

reached in Osaka, and to work out a mutually acceptable solution through

equal-footed dialogue and consultation with mutual respect.”

This was counter to an

earlier comment that threatened unspecified retaliation against Trump’s threat

to impose more tariffs in September. And so, the jawboning goes on…

The WSJ reported that the European

Central Bank (ECB) is in the process of revealing a stimulus package at its next

meeting in September that should exceed investors’ expectations. In other words,

things are so bad, economically speaking, that only a shock-and-awe effect will

revive Europe’s sagging economies.

As a result, the 10-year US

bond yield took

a dive below the 1.5% level to touch 1.48% before rebounding. That was the lowest

price in three years and confirms that the race to the bottom will accelerate.

If you think, zero percent interest rates are simply insane, you are correct.

Look across the Atlantic towards

Denmark, where this idiocy has now morphed into negative mortgage rates. Denmark’s

3rd largest bank is now paying

people to take out a mortgage.

In the end, the markets meandered

aimlessly with the absence of bulls and bears marking a day that was

clouded by confusion and uncertainty. However, it was a good environment for those

of us holding the low volatility ETF SPLV, which advanced +1.11% vs. the SPY’s

more meager +0.26%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}