Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 240 (last week 211)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

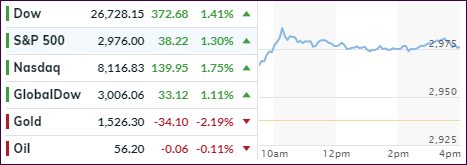

Today’s jobs report came in weaker than

expected, as only 130k jobs were created in August vs. a hoped for 170k. Stocks

shrugged off the poor number with traders and algos alike seeing the positive in

increased odds that the Fed will indeed cut rates (maybe even the whisper number

of 0.5%?) when it meets in 2 weeks.

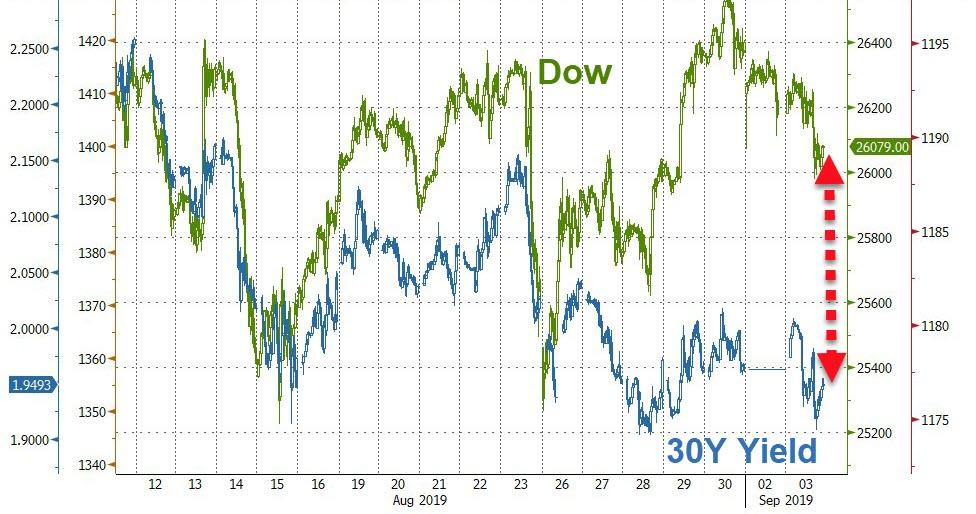

As a consequence, bond yields dropped,

after spiking yesterday, while the dollar dumped

and reached a level that was a starting point for Thursday’s rally. In other words,

nothing was gained.

The mid-day rebound lost steam in the end

with the S&P 500 barely hanging on to a green close, while the Nasdaq slipped

slightly into the red. Still, for the week, the S&P eked out a gain of some

+1.8%.

Trying to keep things calm were words from

Fed head Powell, who said that “he is not forecasting or expecting a

recession,” though he sees “significant” downside risks that the Central

Bank will monitor.

Interestingly, as ZH posted, since the last

Fed rate-cut, the US dollar and stocks are unchanged, while bonds and gold are

up some 6%, as this

chart shows.

Hmm, does that mean rate cuts are no longer providing

the fire power to support stocks? We’ll find out after the next Fed meeting if

this proposition holds true.

ETF Data

updated through Thursday, September 5, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

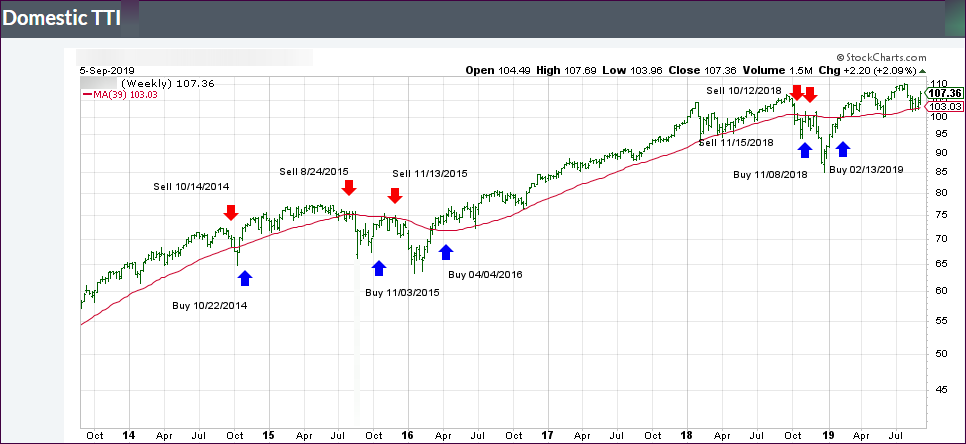

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +4.50% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Just when you thought the

trade deal was dead, news that US and Chinese officials declared a tentative resumption

of tariff talks made the headlines, and off to the races we went with the computer

algos pushing the indexes sharply higher.

Mind you that nothing worthwhile

was accomplished. The warring parties simply agreed to talk again around “early

October,” which these days is considered enough of a progress in the yearlong

trade conflict for equities to surge.

To be fair, bullish

sentiment was boosted by a couple of economic reports. First, ADP estimated that

the private sector added some 195k jobs in August, which raised expectations for

a good number tomorrow when the BLS releases its jobs report.

Second, despite recent surveys

pointing to weakness in the manufacturing sector, the ISM rebounded, even though

60% of its components weakened. Nevertheless, for the day, the markets treated ‘good

news’ as ‘good news’ with equities spiking.

That spike came in the face

of sharply surging bond yields with the 30-year heading back above 2%, while

the benchmark 10-year dashed 10 basis points to 1.58% before pulling back into

the close.

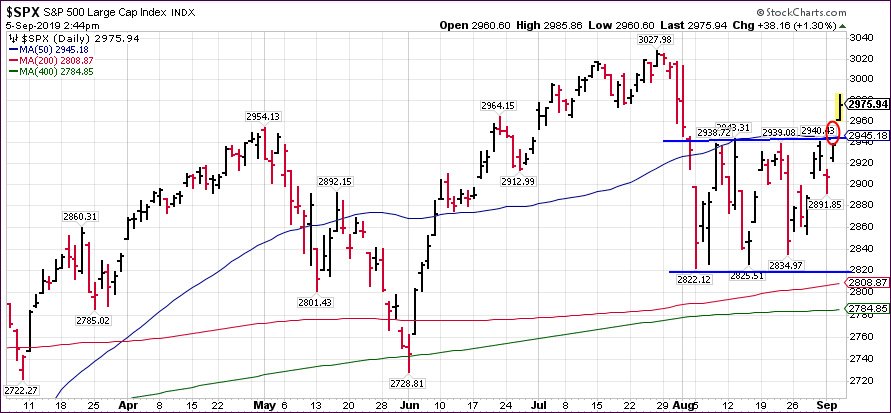

The S&P 500 broke out

of its 5-week trading range (upper blue line) leaving a break-away gap behind

(red circle). This gap will need to be closed at some point, so it’s questionable

at this moment in time whether this breakout has enough legs to take out July’s

highs.

This strong up move in the face

of dramatically rising bond yields is unusual and, while this push benefited

the S&P 500, it’s low volatility cousin SPLV, which I have preferred during

this ‘Buy’ cycle, lagged and did not participate.

This means for this current cycle,

which started on 2/13/19, the S&P 500 (SPY) has made up some ground and is

now showing an +8.28% gain, which is still substantially behind the SPLV’s +12.89%.

Tomorrow’s jobs numbers are bound

to affect market direction. The question is “which way?”

The major indexes staged a turnaround,

after yesterday’s pullback, encouraged by an apparent ease in Hongkong tensions.

Chief executive Carrie Lam announced that she would withdraw the controversial extradition

bill that has sparked months of violent protests, which were feared to eventually

hurt the business climate and global financial markets.

While this bill meets only

one of five demands from the protesters, at least it’s a step in the right

direction, which put the computer algos into a buying frenzy and spreading a

sea of green in equities.

Also helping the bullish mood

were reports that the People’s Bank of China will soon implement cuts in reserve

requirements for Chinese banks, a move that is expected to boost growth and

shows willingness by the government to battle the effects of higher US tariffs

on Chinese imports.

This readiness by the Chinese

to engage in some sort of stimulus eased fears, at least for the moment, that

the US economy might slide into a recession in part due to the endless US-China

tariff conflict, which has been a contributing factor to not just a worldwide disruption

of supply chains but too a slowdown of global economies.

Likewise giving an assist to

the bullish cause was more dovish encouragement from a variety of Fed speakers

that rate cuts are on the menu. ZH summed them up as follows:

Williams (Dovish):

“Ready to act as appropriate”, July cut was right move, economy mixed

(admitted consumer spending not a leading indicator), international news

matters, low inflation biggest problem.

Kaplan (Dovish):

“Monetary policy a potent force”, worried about yield curve

inversion, economy mixed (factories weak due to trade, consumer strong),

watching for “psychological effects” on consumers, “if you wait

for consumer weakness, it might be too late.”

Kashkari (Dovish):

Tariffs, “trade war are really concerning business”,

job market not overheating, slower global growth will impact US, most concerned

about inverted yield curve. Fed’s policy is “moderately

contractionary.”

Bullard/Bowman (Looked Dovish): Took

part in “Fed Listens” conference but made no comment on policy but

then again when has Jim Bullard ever not been dovish.

Beige Book (Mixed):

Moderate expansion but trade fears are mounting, but optimism remains, despite

what Kashkari says: “although concerns regarding

tariffs and trade policy uncertainty continued, the majority of businesses

remained optimistic about the near-term outlook”

Evans (Dovish): Trade

policy increases uncertainty and immigration restrictions lower trend growth to

1.5%, Auto industry especially challenged

As a result, the markets

have now ‘priced in’ an astonishing 124 bps (1.24%) of rate cuts through the

end of 2020. Tip of the hat goes to ZH for this

chart. On the other hand, a trade deal is now almost entirely ‘priced

out,’ which means that the only ‘big dog’ left to support equities is none

other than the Fed and its policies.

Last week’s rally was based

on nothing more than rekindled optimism that the ever-accelerating trade war with

China may be “again” on another verge of the warring parties agreeing to a

ceasefire.

On the other hand, how many

times can you cry “wolf” before it’s being ignored.

Apparently, we have not

reached that moment in time yet, as on Sunday morning, against all wishful thinking,

the US slapped tariffs on $112 billion in Chinese imports. It only took 1

minute for China to retaliate via higher tariffs on some $75 billion of US

goods.

That killed the “trade deal

is imminent” proposition, and it became clear that Tuesday’s market reaction

would be a negative one, and that’s exactly what happened.

Assisting the sour mood of traders

and algos alike was a report showing that US manufacturing is the weakest in 10

years, and the headline manufacturing number plunged

into contraction.

At its lowest point, the Dow

was down over 300 points, and the S&P 500 almost closed the breakaway

gap I mentioned last Thursday, while the index seems to be heading towards the

lower band of the 5-week trading range.

With the slippage of the

markets, it appears that there may be some recoupling of stocks and bond yields

in the near future, as the jaw

of death has closed slightly—and not in favor of stocks.

We will find out soon enough

if that tendency continues.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}