ETF Tracker StatSheet

You can view the latest version here.

HOMING IN ON ALL-TIME HIGHS

- Moving the markets

The markets got an early lift from retail sales, despite the August report showing a mixed picture. While purchases of new autos and building supplies contributed to the rise of 0.4% last month, most other stores reported weak or declining receipts, which appears to be a sign that consumers have trimmed their spending.

Equities slipped throughout the session with only the Dow closing in the green and scoring its 8th straight gain. The Dow and S&P 500 are now within striking distance of fresh all-time highs, which may very well happen next week in anticipation of the Fed not disappointing and lowering interest rates next Wednesday.

Trade tensions with China appeared to have softened a tad, at least for the time being, in that China exempted US agricultural products from tariffs. That overture came after reports that an interim trade deal has been struck.

Still, something odd is happening in the relationship between bond yields and equity prices. The 10-year yield surged again by almost 13 basis points, a huge move, which many traders consider a bond bloodbath. That should have been headline news but was barely mentioned in the press.

Despite all the rhetoric about lower rates, mortgage rates have shot up, and the 10-year bond yield, which a few weeks ago was at 1.47%, has spiked to 1.90% without as much as a hiccup in equities. Even the 30-year yield climbed an amazing 33 basis points this week, a surge that is the second biggest since 2009.

The rotation out of well-performing momentum stocks into the cyclical and value arena continued, as higher yields impacted low volatility ETFs, such as SPLV and USMV. While they lagged in performance, they are still holding on to their YTD lead over SPY.

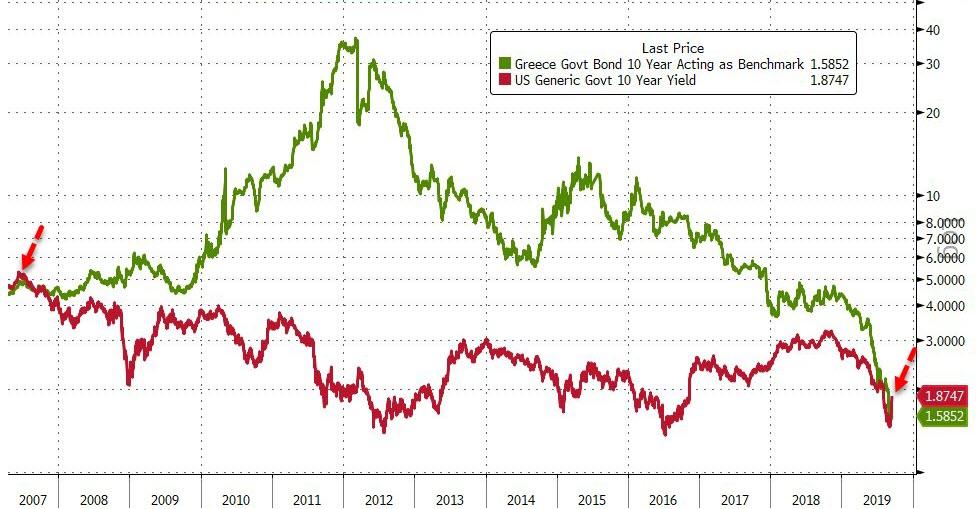

We’re living in a such a distorted system where, as of today, Greek 10-year bond yields are now below US 10-year yields for the first time since 2007. For the uninitiated, that means, at least in theory, Greece is less of a default risk than the US.

Go figure…

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}