Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 267 (last week 244)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

Quadruple

witching day occupied the traders on Wall Street, as the 3rd Friday

of every quarter can produce added volatility due to the simultaneous

expiration of single-stock options and futures and index options and futures.

A

mid-morning sudden spike was not caused by any option juggling but was merely a

reaction to VP Pence’s conciliatory comments about the trade meeting. It did

not take long for the Chinese to pour some cold water on his remarks via things

like “the Chinese side is concerned about the fairness of a trade deal,”

followed by “the US side must remove all newly imposed tariffs.”

This

took the starch out of the upward move, and the Pence

spike was erased in short order. The major indexes managed to tightly roam

around their respective unchanged lines for the remainder of the session, seemingly

unfazed by another set of weak econ data. A dive into the close pulled us back into

the red, but the losses were minor. However, for the week, the S&P 500

managed a gain of some 2.2%.

We

learned that existing home sales continued their downward spiral, as the rise

of 2.5% MoM in May does not tell the entire story. When looking at it longer term,

this data set has tumbled

YoY for the 15th month, which is the worst since the housing crisis.

At

the same time, US manufacturing (PMI) plunged to 10-year lows in June, with

both indexes (Manufacturing and Services) edging closer to contraction.

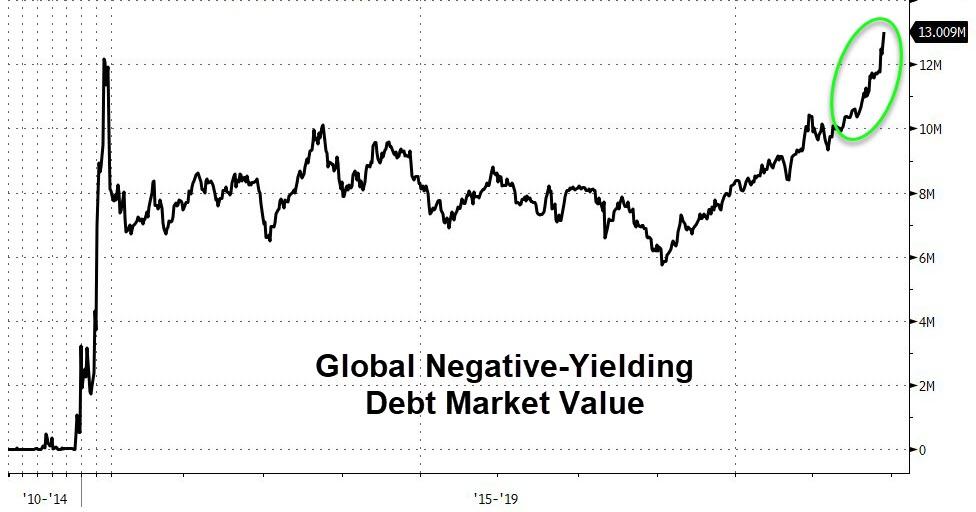

Since

bond yields have been getting most of the attention lately, as the 10-year

is threatening to drop below the 2% level, worldwide, the picture looks even

gloomier. Global negative yielding debt soared by $700 billion in one day to a record

$13 trillion.

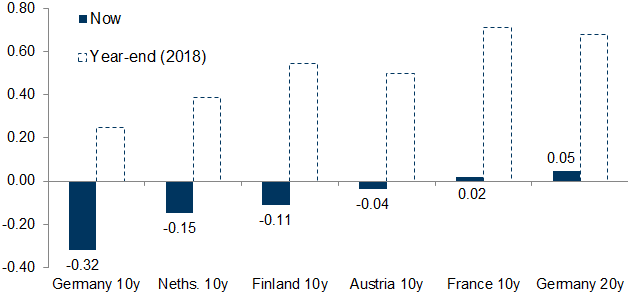

Look

at the yield

disaster that Europe is showing, especially when you review the comparative

data as of year-end 2018. This kind of a collapse in yields is not a bullish

indicator. It’s the opposite, as it clearly points to collapsing global growth

and a potential slide into a recession.

Makes

me wonder when the equity markets will figure this out…

In

the meantime, we will ride this trend until it ends, when it bends and our Trend

Tracking Indexes (TTIs) signal to get us out of equities and to the safety of

the sidelines.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

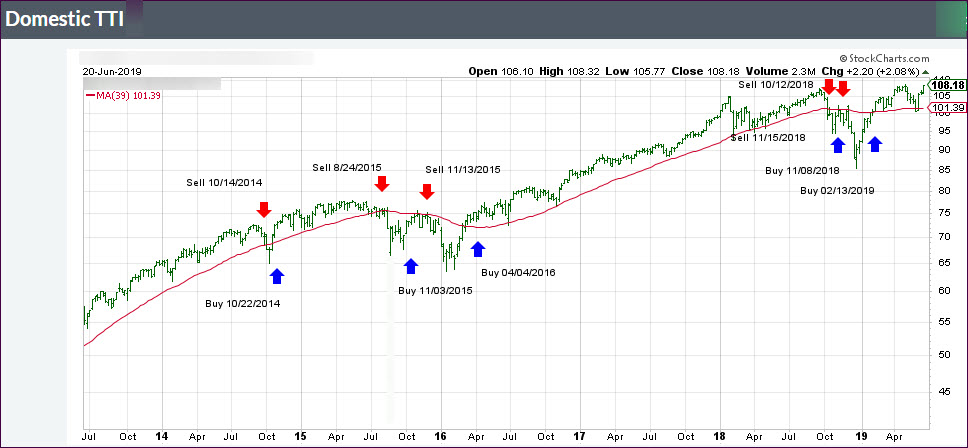

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +6.73% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

After sleeping on the Fed’s statement on interest rates,

Wall Street traders decided that the Fed left the door somewhat open to a rate

cut. As a result, expectations soared from 80% to 100% that the Fed will “cut”

in July.

That was enough for the major indexes to gap higher at

the opening with the S&P 500 setting a new intra-day

all-time high in the process, while taking another giant step towards conquering

its $3k milestone marker.

A mid-day dip did nothing but encourage more bulls to jump

aboard this pause in upside momentum, and up we went notching new highs for the

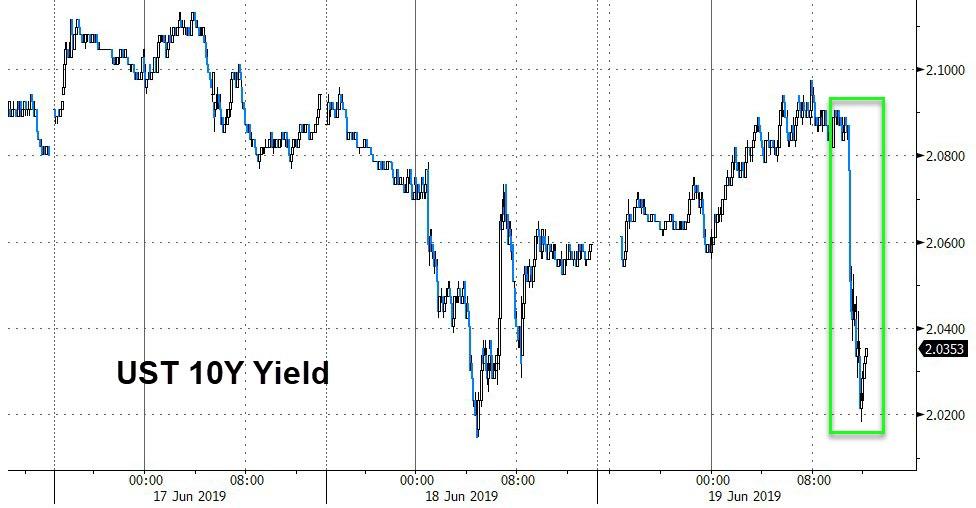

session prior to the close. Bond yields headed lower again, with the 10-year

barely hanging on to the 2% level, although it dipped below it intra-day.

While most of the attention was on the Fed, it’s important

to note that tomorrow is quadruple option expirations day, which can cause the markets

to move violently in either direction prior to expiration time. I think a great

deal of today’s upward ammo came from that looming deadline.

Also helping today’s bullish cause was a report that the

warring parties in the U.S.-China trade dispute have decided to get together again,

with the U.S. delegation traveling to Japan next week for “preliminary” meetings.

As I have posted before, the rise of the global money supply

has been a terrific indicator as to the overall direction of equities. It has surged

once again and has been a major contributor to rescuing the markets after the

very destructive month of May, during which the S&P 500 lost -6.6%.

One of the most eagerly watched events, namely the Fed’s verdict

on interest rates, came and went without much of a market hiccup. A gentle

early slide gave way to a modest bounce late in the session, with the major indexes

notching another green close and moving within striking distance of taking out

their old all-time highs.

The Fed decided to hold interest rates steady and motioned

that it’s unlikely that they would cut borrowing costs for the remainder of the

year. Of course, judging by their past actions, nothing is ever chiseled in

stone, and they left themselves a little wiggle room by pronouncing to “closely

monitor” inflation and growing “uncertainties.” The latter appeared

to be a jab at the escalating trade tensions between the U.S. and China.

In other words, if things change, they may change their mind…

While the White House might not be too pleased with this outcome

(Trump has been advocating an interest-rate cut for months), market reaction

was kind of muted, but we did zig-zag higher after the Fed announcement.

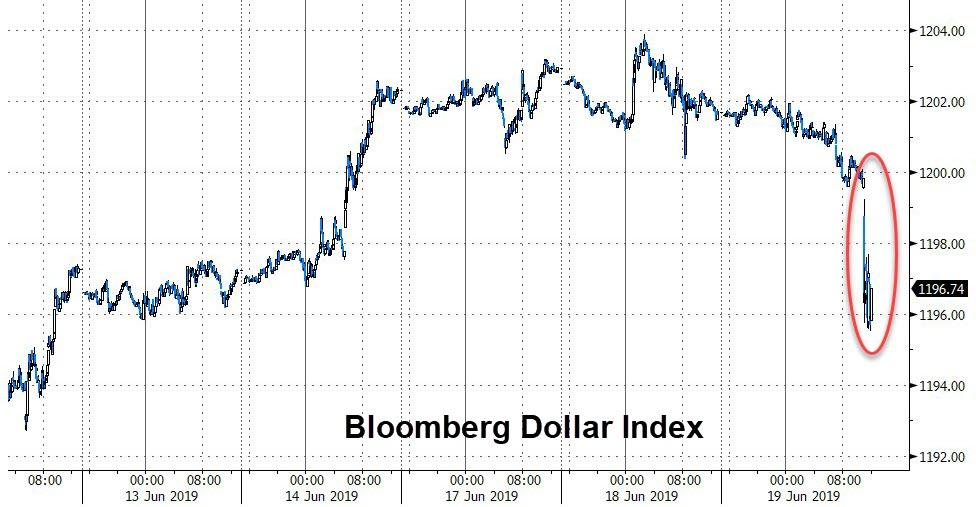

Bond yields were the beneficiary, as yields dropped with

the 10-year

heading towards the 2.01 level, while the U.S. Dollar tumbled

after the Fed released its statement.

Could the markets take off from here and push into record

territory? For sure, “if” at the upcoming G-20 meeting in Japan, Trump and his

Chinese counterpart Xi agree to a trade deal, or at least pronounce progress in

negotiations. That should do the trick and give a boost to the major indexes.

Trump got the markets pumping this morning after tweeting

that there will be an “extended meeting” with China’s Xi at the upcoming

G-20 meeting in Japan. Bloomberg also added that the two leaders had confirmed

a plan for meeting on the sidelines.

That was enough hype for the headline-scanning computer

algos to drive the markets out of last week’s trading range, with the S&P

500 now hovering within 1.25% of its record high. Never mind that various reports

later-on toned down the Trump/Xi meeting, but that no longer mattered. The bulls

were up and running.

The other positive for equities was what appeared to be a

policy turnaround, when the head of the European Central Bank (ECB), Draghi,

hinted at lower rates and more stimulus. I recall that, only a few weeks ago,

Draghi announced no policy changes in the foreseeable future. Hmm, things must

have really taken a turn for the worse…

His dovishness was just what global traders wanted to hear

with the instant result that stocks pumped and yields dumped, widening the already

substantial divergence

between the S&P 500 and the 10-year yield.

Bond yields crashed globally, as you can see here,

here

and here.

Other than the U.S., most bond yields on the face of this earth have now

slipped into negative territory. For example, if you invest in a German 10-year

bond (called ‘Bund’), your annual interest rate is now -0.32%. In other words, you

lose -0.32% every year for 10 years. How is that for insanity?

For further contemplation, ZH posted the question: Who’s

right? Global Bonds, Global Stocks or Global Macro?This

chart shows the divergence. Eventually, we will find out the answer to that

question.

My guess is that bonds will prove to be right, with

stocks ultimately having to correct down to fair value.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}