- Moving the markets

For those hoping for a turnaround Tuesday, it did not happen, as virus headwinds continued to spread around the world. An early rebound proved to be meaningless with the downward trend remaining intact.

Internationally, it was worse than domestically, with our International TTI diving below its long-term trend line by a margin large enough to generate a “Sell” signal for that arena. Please see section 3 for details.

Market sentiment was mixed, as dip buyers try to step in to prop up the indexes, but volume was not heavy enough to accomplish anything other than a temporary halt in the downward swing.

After Monday’s drubbing, traders expected a bounce back, or at least a pause in downward momentum, but the tumble continued unabated. Of course, investor complacency, caused by the Fed’s support policy of the markets, has many in shock, as realization set in that markets can go down, and that corrections of 5-10% are a perfectly normal occurrence.

Not helping the mood were some economic news showing that the Fed Business Survey crashed in February with new orders collapsing, while Subprime Credit Card Delinquencies spiked to record highs and surpassed the financial-crisis peak.

The S&P 500 price of 3,200 was considered by some analysts a crucial support level and, once broken, could lead to higher volatility and more downside risk, in the -10% area. Well, the level did not put up any fight, and the index sliced right through it closing the session at 3,130.

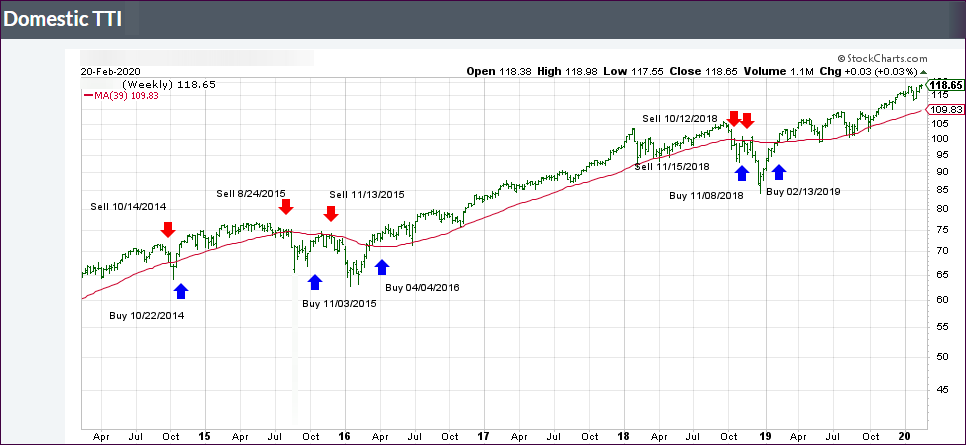

As a result, our Domestic TTI, the main directional indicator, headed south as well and has now reached a point that is within striking distance of a “Sell” signal. As you can see in section 3 below, we are currently only 0.35% away from this event becoming reality.

If it does, and the trendline is clearly pierced to the downside, we will move out of the markets and to the safety of the sidelines, as the odds of this turning into a full-blown bear market will have increased.

Fed vice-chair Clarida did not help matters by saying:

US economy and monetary policy are in a good place, noting that it is still too soon to speculate on whether the coronavirus will lead to a material change in US economic outlook.

Despite a temporary pause in the drop, while Clarida was talking, downward momentum picked up again, as it became clear that there were no solutions or promises forthcoming. Interestingly, the chart I posted last week, proved to be an accurate prognosticator, as the S&P 500 finally caught down to global liquidity.

In my advisor practice, we will start liquidating some of those positions, whose trailing sell stops were triggered, and will prepare for an all-out domestic “Sell” signal.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}