- Moving the markets

Well, that did not last very long. Even though the Fed’s most dovish words yesterday were able to soothe markets and produce a bounce back from early losses, today was a different day.

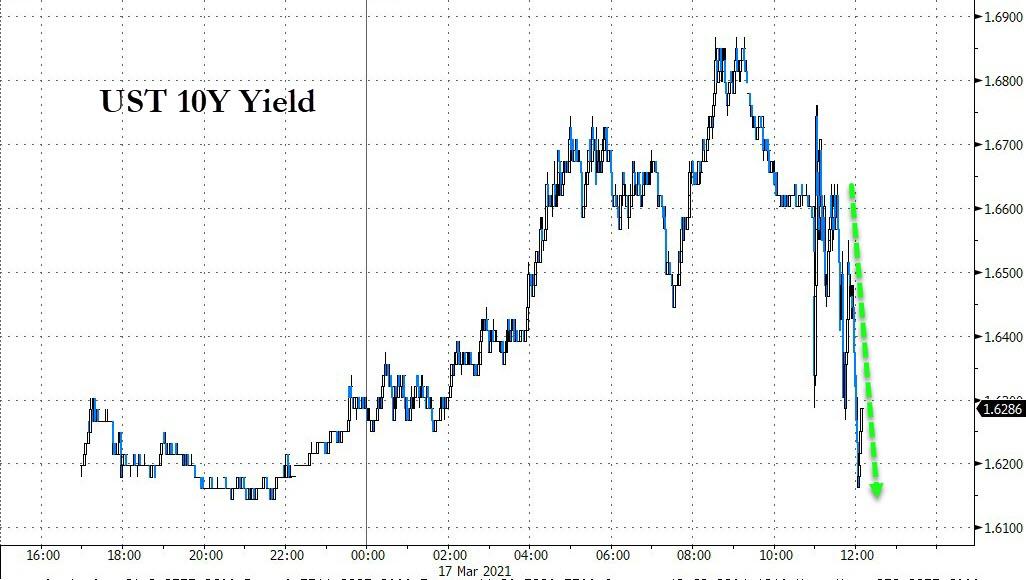

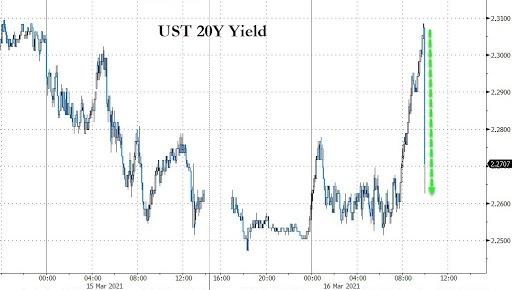

Bond yields suddenly surged, up 11 basis points intraday to 1.75% for the 10-year, but they came off that high to close up +7.5 basis points. Confusion reigned in the markets, and traders and investors alike scrambled to grasp where that volatility came from.

Added MarketWatch:

By confirming the Fed’s willingness to stand pat, even if inflation saw a temporary surge beyond 2%, investors may be raising the probability the economy will run hot in the next few years without having to worry about the central bank pulling away the market’s punchbowl. In that scenario, long-term bond yields would have little protection against the risk of an inflationary surge.

And that sums it up perfectly. Inflation at current levels is far higher than what the Fed admits and any considerable improvement in the economy will only add to that worry, the fear of which is now apparently reflected in the pricing of bond yields.

Tech shares got hammered with the Nasdaq plunging -3% with only the financial sector (XLF) closing higher by +0.52%. The S&P 500 tumbled a more moderate -1.48% and the Dow fared the best, down only -0.46%.

Economic data were mixed at best with weekly jobless claims at 770k turning in another poor number compared to expectations of 700k. Looking at the bigger picture, it means that over 18 million Americans are still dependent on government jobless benefits, a number that has not changed materially for four months, according to ZH.

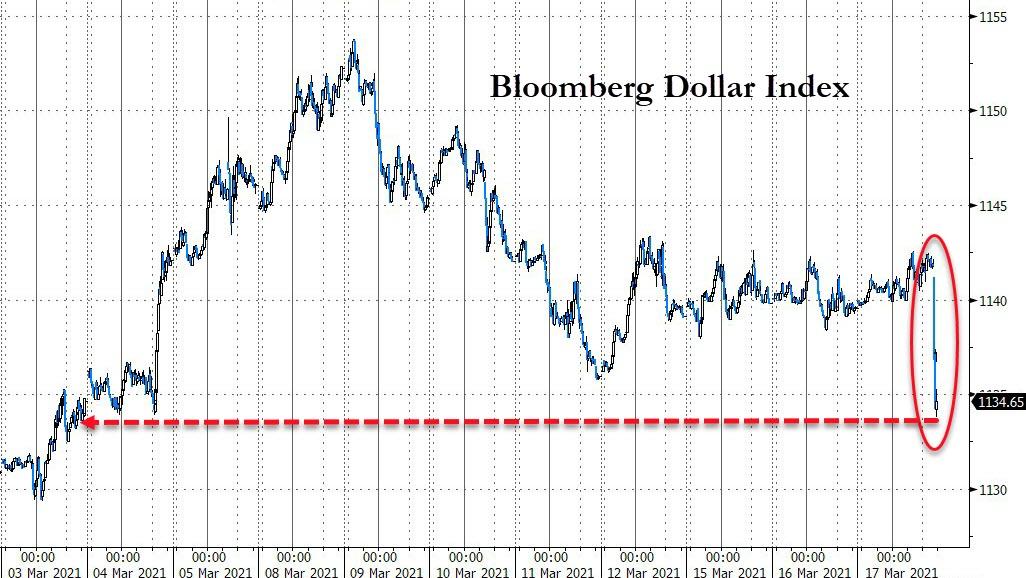

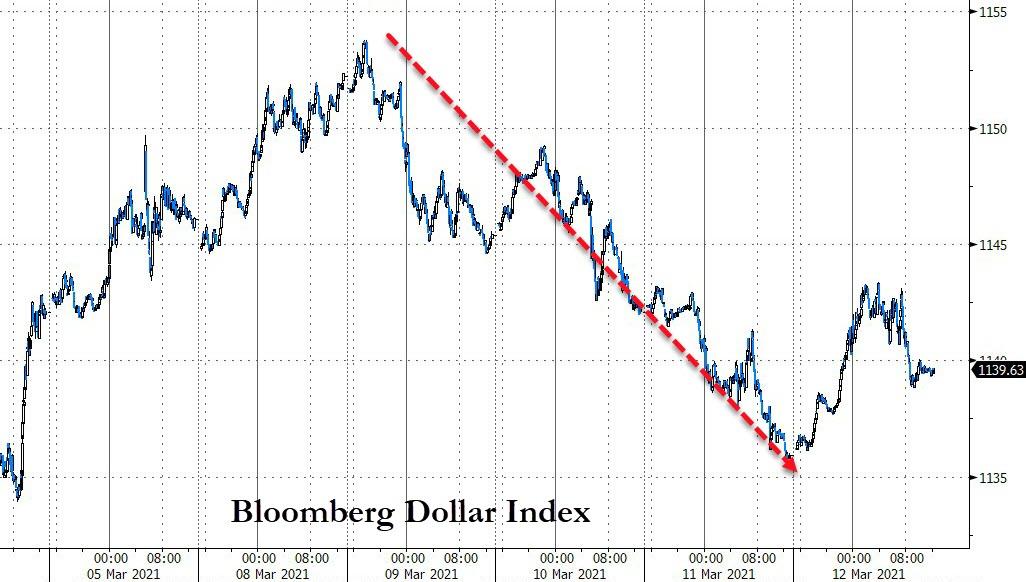

The US Dollar index recovered from yesterday’s drop and headed higher, but spot gold managed to hang on to early gains, yet the gold ETF GLD ended in the red.

Tomorrow, we may see another kick up in volatility, as another market event is on deck, namely the quad-witch (quadruple expiration), when we get the simultaneous expiration of stock index options, market index options, individual stock company options and single-stock futures.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}