- Moving the markets

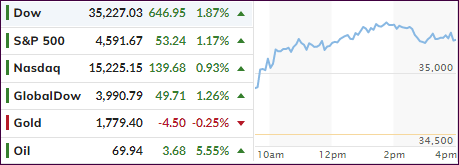

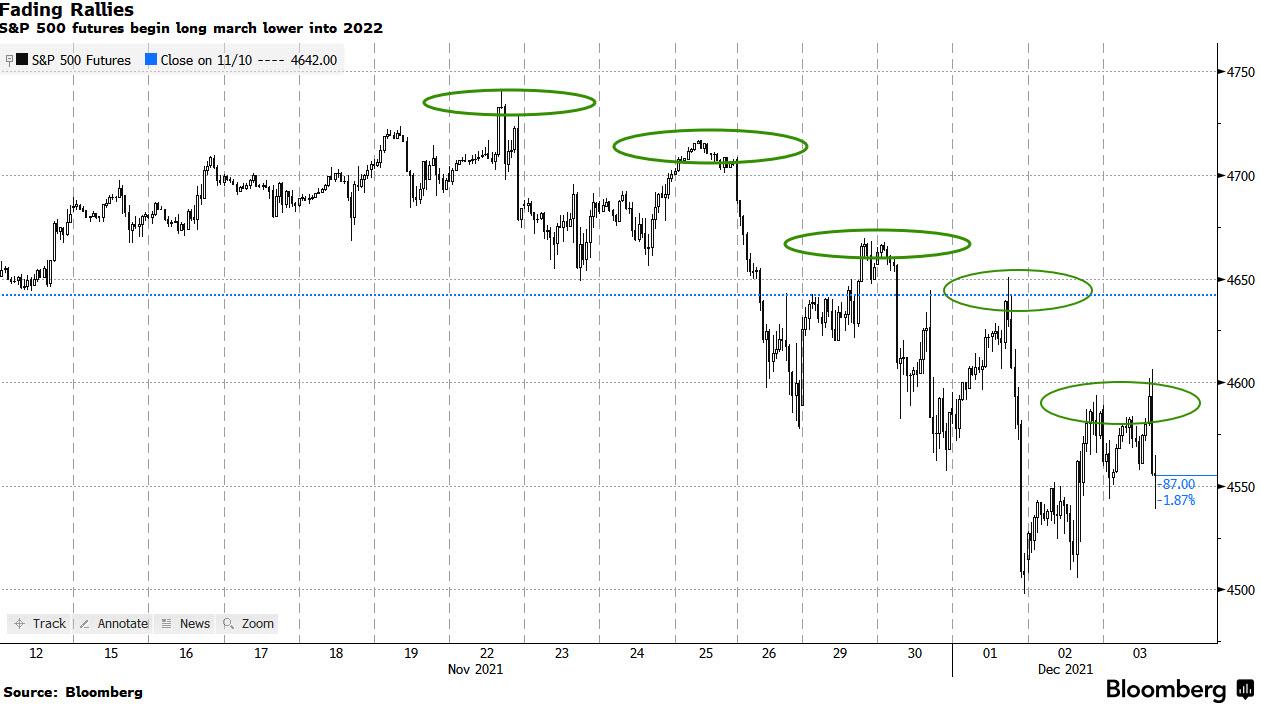

After wild rides in the markets last week, which saw early rallies wiped out later in the session, we finally witnessed an opening surge that improved throughout the day and did not peter out in the afternoon. Sure, momentum slumped a little into the close, but that can be expected.

In the process, the Dow managed to erase all last week’s losses, while the S&P 500 just fell a fraction short. MarketWatch summed up today’s influencing forces like this:

- Shares linked to the economic reopening gained in Monday trading, including energy, industrials, and airlines.

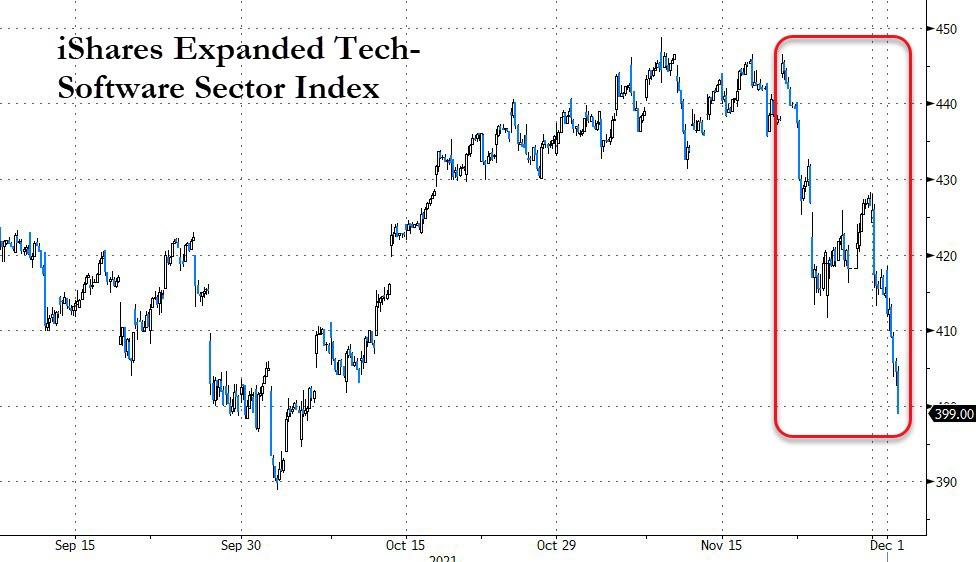

- Investors continued to sell tech stocks with relatively high valuations. Those shares dragged the market down to a losing week on Wall Street last week.

- The 10-year Treasury yield rebounded after falling last week amid the omicron threat.

- There’s a major shift underway at the Federal Reserve to bring about a faster end to its pandemic easing policies.

The Nasdaq lagged the other two major indexes as the health care and tech sectors were weighing down the indicator, with Moderna being the biggest decliner by shedding 15%.

Anxiety about the new Omicron variant remains, despite continuous reports of its symptoms being less severe, but fearmongering in the MSM seems to be always in high gear. It appears that any economic data are playing second fiddle to the latest headlines dealing with Covid 19 or its variants.

Finally, the short squeeze came back to life again, after being suspiciously absent during last week, and gave a much-needed assist to insure the rebound would not run out of steam.

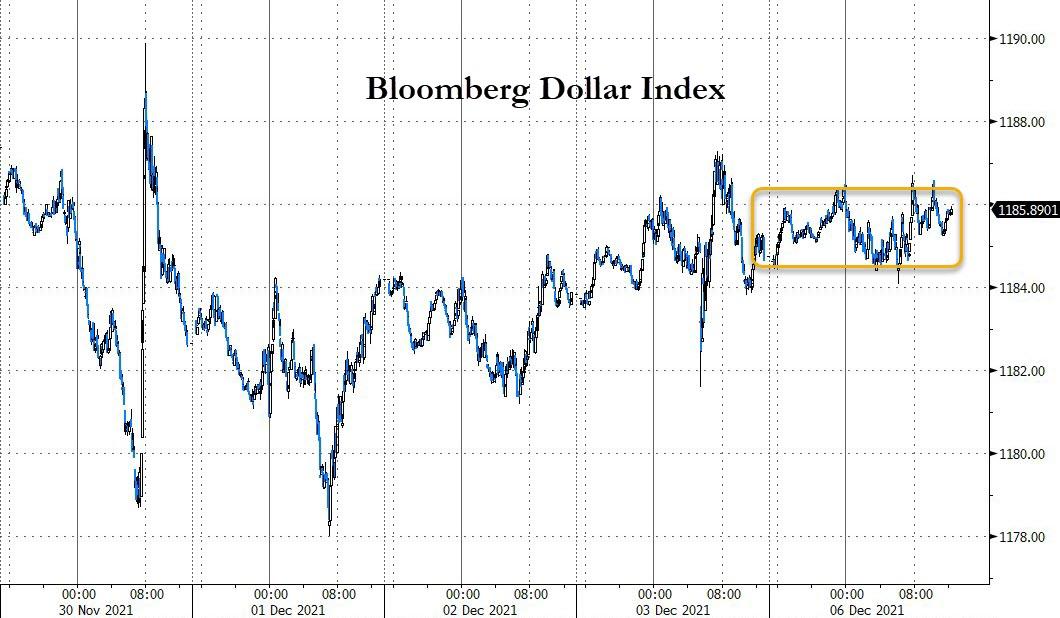

Bond yields surged after an early dump, with the 10-year eking out a small gain and closing the session at 1.48%. The US Dollar went sideways for most of the day but ended up higher by a modest 0.19%.

Gold drifted lower after Friday’s strong rebound with the precious metal giving back 0.24%, while still attempting to permanently conquer its much fought for $1,800 level.

I expect the recent volatility to stay with us, especially when on Friday the much-anticipated US CPI will be released.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}