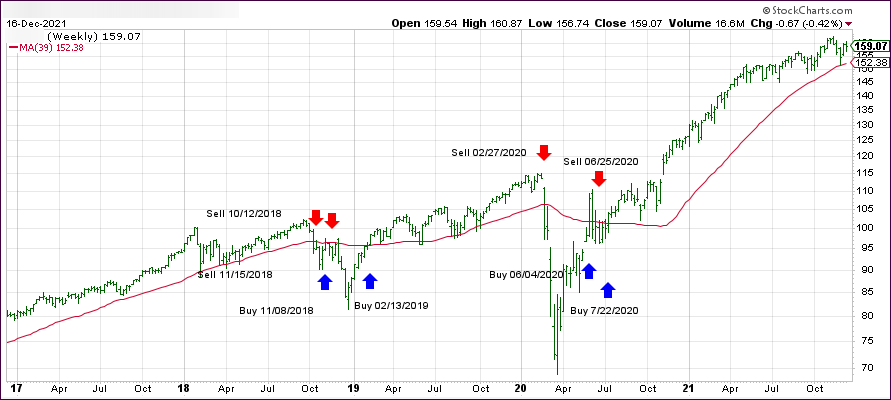

- Moving the markets

My somewhat humorous headline contains some truth in that hope for a Santa Claus rally is alive and well but has been met with resistance due to intensifying omicron fears with a resurgence in the number of Covid cases, which have been blamed on the variant.

To be clear, the Santa Claus rally may still materialize, as “Stock Trader’s Almanac” considers it to be the period including the last five trading days of the year and the first two trading days of January. That means, all hope is not yet lost.

Today was simply a continuation of Friday’s slam with dip buyers again being conspicuously absent. Commented Jim Paulsen of the Leuthold Group:

The downward move in markets “reflecting growing uncertainty surrounding whether the Omicron surge will bring new widespread economic shutdowns, an unexpected shelving of additional fiscal stimulus from President Biden’s Build Back Better plan, and a breach by the S&P 500 index of its 50-day moving average.”

Today, there was no place to hide, because growth, value and SmallCaps were equally hammered, as was the tech sector in general. Even the low volatility SPLV ETF was not able to withstand the selling and gave back -0.31%.

The major indexes swooned in unison and bounded off their worst levels of the session, but it was not nearly enough to even think about a green close. Interestingly, the S&P 500 closed today within 1 point of where it started the month of December, so not much has been gained or lost during this period, despite the index having just suffered its biggest 3-day drop since May.

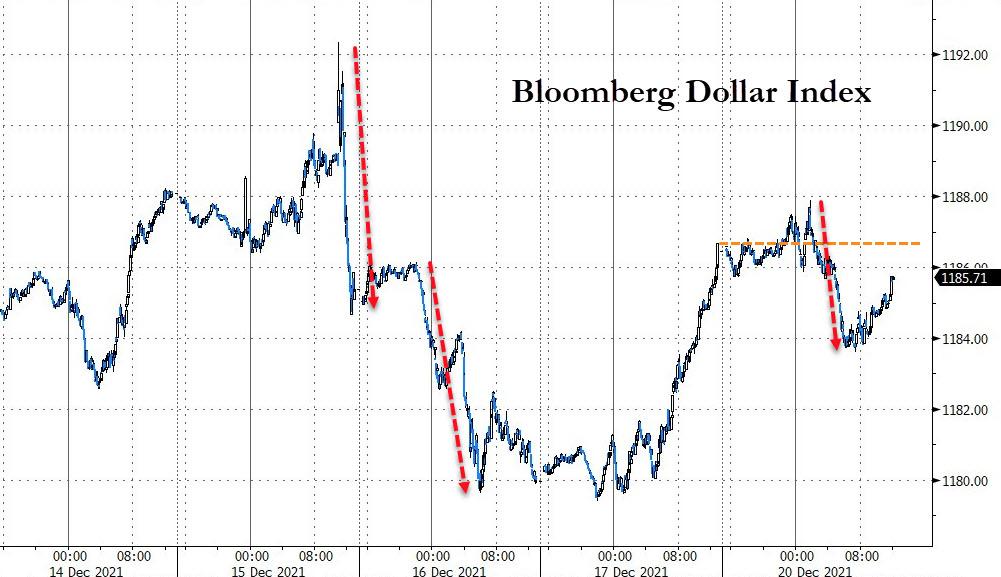

The most shorted stocks surrendered Friday’s victory, as ZeroHedge pointed out, while the US Dollar was not able to build on its recent gains and ended up bouncing lower. Gold held steady for most of the morning, that is until the bears put another nail in the coffin and sent the precious metal down -0.81%.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}