Another crazy day on Wall Street had equities swinging wildly, although with reduced magnitude. In the end, the major indexes crawled back but failed to reach their respective unchanged lines.

Every directional turn appears to be headline driven, as the bulls and bears continue to slug it out. Failed peace talks between Russia and the Ukraine caused the potential global economic fallout to move to front and center again thereby putting a damper on the bullish meme.

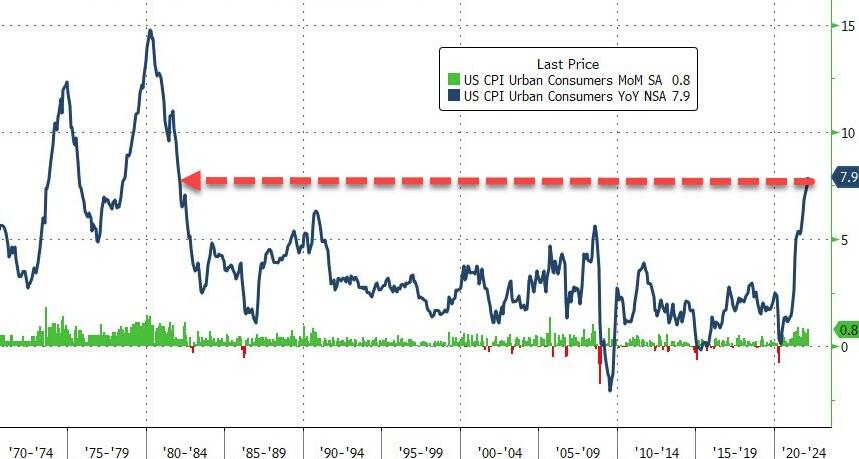

Consumer prices rose at their fastest pace in over 40 years, as ZH reported, with the headline print coming in at the expected +7.9% YoY. That is the highest reading since January 1982 and is also the 21st straight month of increases in consumer prices. So much for inflation being transitory.

Bonds extended their losses, as yields spiked, with the 10-year again approaching the 2% level. The US Dollar went sideways but surged into the close, Crude Oil slipped for the second day, but gold found some footing to recapture the $2k price level.

Volatility is here to stay, which means wild rides on Wall Street may become the standard rather than the exception.

It had to happen eventually, and today was the day. After 4 days of taking a beating, equities finally found a reason to rally, as questionable as it may turn out to be.

One analyst linked it to the adage “buy the rumor, sell the fact,” but in this case it turned into “buy the Ukraine speculation, sell the lack of follow through,” however, we will have to wait and see if the latter part materializes.

Headlines went into overdrive with Bloomberg reporting this:

*AIDE TO ZELENSKIY SAYS UKRAINE READY FOR DIPLOMATIC SOLUTION

That was followed by some dampening of the initial euphoria:

*UKRAINE’S ZHOVKVA: WON’T TRADE `SINGLE INCH’ OF TERRITORIES

And finally, as ZH pointed out:

*UKRAINIAN AIDE: SEEK CLEAR RESPONSE TO EU APPLICATION

Which also seems like a dead end, because as JPMorgan said last night, “Ukraine is no longer insisting on NATO membership, though EU membership would give similar protections.”

Nevertheless, it was a session during which, no matter what happened, the bulls remained oblivious to anything bearish and made up for lost ground by recouping some of this week’s damages.

It was another wild ride, during which energy and commodities were hammered, after their recent bullish run, but both came off their intra-day lows by a strong margin. With higher oil prices and continued inflation, I expect this spanking to be a correction rather than a major directional trend change.

The dreaded “S” word, which I have repeatedly mentioned, remains in play with one hedge fund giant seeing it this way:

The way things are going now, $200 per barrel is a clear possibility, according to Jeffrey Gundlach from investment firm DoubleLine. Speaking to TIFIN, Gundlach said that oil is on its way to $200, and the Fed may be pressed to raise rates while the country is going into a recession, which, he noted, had never been done before. Gundlach also said it was time to admit the U.S. was going into stagflation, and the latest increase in gas prices was only the beginning of the pain.

Safe havens like bonds were losers today, as yields spiked, while the recent performance hero, namely gold, was taken out to the barn and spanked, in process losing its $2k handle.

The madness on Wall Street continues. The Fed will try to manage a soft economic landing, the chances of which are just as great as their past announcement that inflation is “transitory.”

Sometimes you just simply must step back and watch in awe how current markets trade like a penny stock when it comes to volatility.

Yesterday, equities were simply spanked all day, which continued this morning as the Dow sank some 200 points and bounced around below its unchanged line. A sudden burst of buying pulled the indexes out of their slump, and the Dow soared into the plus by almost 600 points.

The bulls were cheering but were quickly disappointed as this surge got wiped out within 30 minutes, after which another rebound failed assuring a red close for the major indexes. Riding a bucking bronco might provide more directional certainty than current market behavior.

To me, this type of volatility seems to occur mainly at major inflection points meaning once a bearish trend turns bullish and vice versa. Year-to-date, we have seen nothing but aimless meandering, with the bearish theme being confirmed after our Domestic Sell signal became effective on 2/24/22.

ZeroHedge summed up today’s craziness like this:

But while everyone has an opinion about what comes next, the truth is that nobody knows what’s really going on as JJ Kinahan, chief market strategist at TD Ameritrade said: “I don’t think the market’s ignoring anything at the moment, to be honest with you. In fact, everything is hyper-sensitive as to what may happen. It’s so fluid and we will see what happens. It’s really tough to predict day-to-day.”

That said, broken markets continue, and the biggest shock overnight was the continued short squeeze in Nickel, which exploded to over $100,000, up more than 250% on the day, before being halted by the LME amid a relentless margin call frenzy which left at least one Chinese tycoon billions poorer.

The flight to safety was on with the main beneficiary being gold, as the precious metal added another +3.04% to close at $2,056. You might have expected to see lower bond yields during these times of stress, but that did happen because yields rallied with the 10-year closing at 1.85%.

Again, this is the time to be exposed to selected sector funds, especially those that take advantage of the current global economic dysfunction.

I noted my surprise on Friday that equities had not been more negatively affected by the geopolitical events, but that notion seemed to have changed today.

One look at the S&P 500 chart above tells the story that the bears ruled supreme and, at least for the time being, won the tug-of-war against the bulls by severely spanking the major indexes.

The decline was broad, except for certain sectors that were rewarding to be invested in. You can view some of those candidates in my latest Thursday StatSheet.

The actors participating in today’s market smacking were the same from last week, ranging from geopolitical events to inflation fears, GDP heading towards zero and supply chain issues, especially in the energy sector. The realization has now set in that the dreaded “S” word, as in Stagflation, can now no longer be ignored, as the economy appears to be in the process of rolling over.

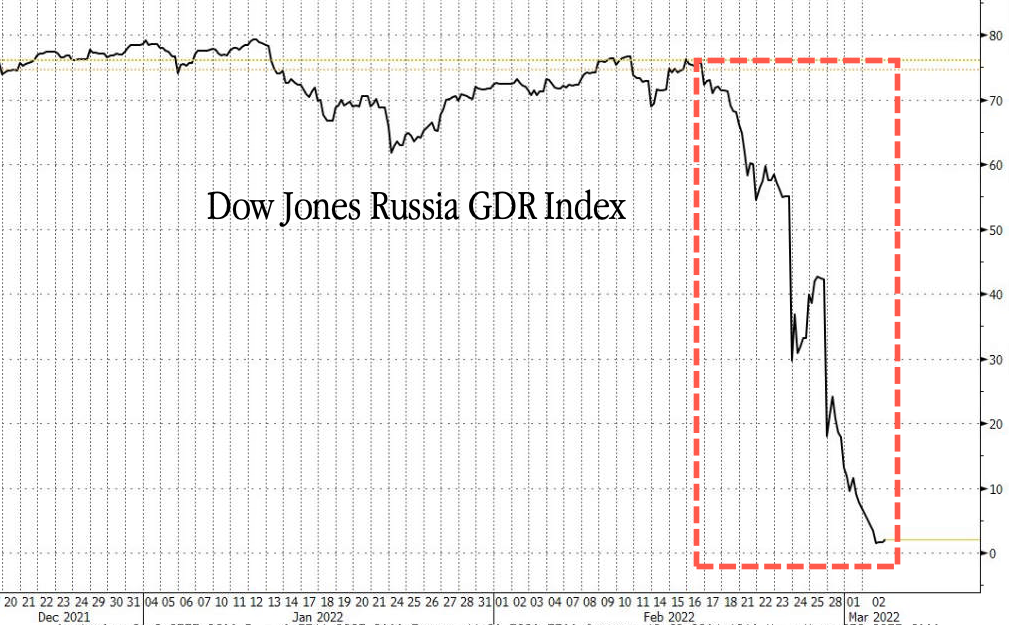

Some traders called the current market to be dysfunctional, while being concerned that credit default swaps may not pay out in case of a default. As ZH noted, part of the reason is that Russian equites have fallen by an absurd amount with one index (GDR) plunging a mind-boggling 97% in just a few days while wiping out some $572 billion. For sure, there will be fallout effects around the world.

Added ZH:

There is no other way to describe today’s market carnage than a market in turmoil where things are rapidly breaking as commodity collateral is suddenly sparking contagion and liquidations.

Then this:

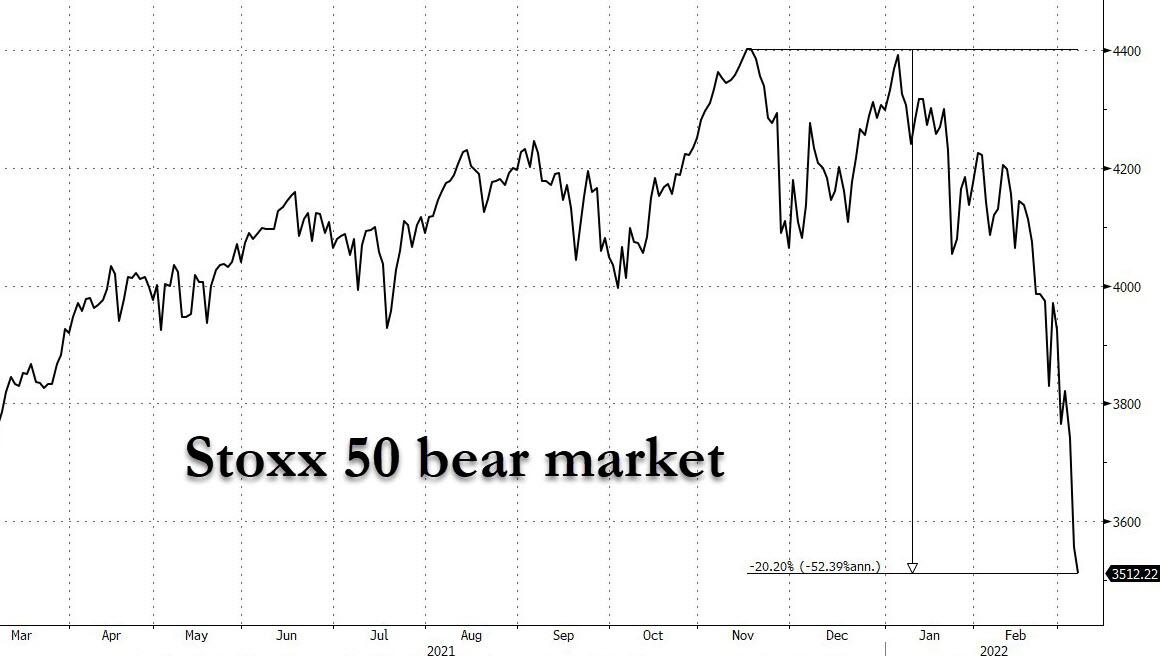

The Nasdaq tumbled 3.6% with the help of Facebook and Moderna both of which have wiped out more than 50% of their value from all-time highs and is now down more than 20% from its all-time high, closing in a bear market, where it joins the Russell, which is now also down more than 20% from ATH.

Europe performed even worse with the well-known Stoxx index now in bear market territory and having reached its lowest level since November 2020. Ouch!

Bucking the trend were gold, energy, and commodities, which appear to provide some stability in an increasingly unstable world, the latter of which was even admitted by the White House:

WHITE HOUSE SAYS U.S. NEEDS TO BE PREPARED FOR LONG, DIFFICULT ROAD AHEAD

Below, please find the latest High-Volume ETF Cutline report, which shows how far above or below their respective long-term trend lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s StatSheet and includes 312 High Volume ETFs, defined as those with an average daily volume of more than $5 million, of which currently 78 (last week 88) are hovering in bullish territory. The yellow line separates those ETFs that are positioned above their trend line (%M/A) from those that have dropped below it.

In case you are not familiar with some of the terminology used in the reports, please read the Glossary of Terms. If you missed the original post about the Cutline approach, you can read it here.

Even a better-than-expected jobs report (678k gained vs. expectations of 423k) was not enough to compete with the negative overhang of the geopolitical environment, as the Russia-Ukraine skirmish continued unabated, despite encouraging attempts on both sides to schedule meetings.

It’s not my job to discuss the Ukraine media headline euphoria but focus on the market fallout. While the initial losses, showing the Dow down 500 points, were sharply reduced by the time the closing bell rang, the outcome was still bearish with the Dow now having scored its fourth straight losing week.

MSM will now try to blame the domestic and global economic conditions on the Ukraine crisis, but keep in mind that slow growth, rising prices, and supply chain issues have plagued us long before said crisis came into the picture. However, negative supply shocks will take things to a new level and move us into uncharted territory.

MN Gordon from the EconomicPrism.com summed up like this:

There are not only oil supply shocks to contend with. There are also food supply shocks…and broken supply chains.

He also succinctly pointed out Fed head Powell’s dilemma:

For Powell, the task at hand this week was twofold. First, demonstrate the central bank would be taking measures to control inflation. Second, show Wall Street the Fed still has its back.

Thus, Powell went middle of the road. He’ll be proposing a 25-basis point rate hike at the upcoming FOMC meeting.

“We’re going to use our tools, and we’re going to get this done,” said Powell to the Senate Banking Committee.

In other words, he’s effectively doing nothing to fight inflation.

What gives? Is this some kind of joke? How’s a 25-basis point rate hike supposed to rein in inflation that’s officially raging at 7.5 percent?

Clearly, Powell’s pivot is a pivot to nowhere. High consumer price inflation is here to stay.

This accurately assesses the current situation with the open-ended question being: Can markets really see this as a bullish environment long term?

Crude oil continued its march higher by gaining 6.58% on the session to close a shade under $115. Europe not only fared the worst in the equity department with their indexes scoring the worst week since March 2020, but their energy costs exploded to a record high.

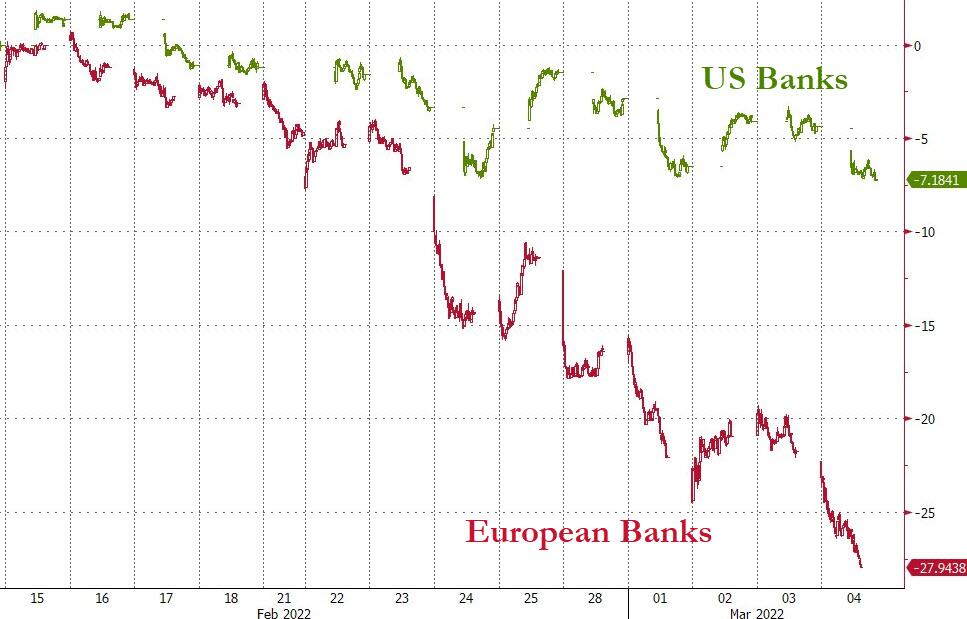

And it did not end there. While US Banks showed weakness, it was nothing compared to their European cousins, which imitated a swan dive. The US Dollar benefited by being perceived as a haven of safety, as dollar liquidity problems ran rampant.

Helping my favorite commodity ETF to add an astounding 4.21% on the day was the fact that Bloomberg’s Spot commodity index saw not only its biggest jump since September 1974 but also closing at a record new high.

Gold followed suit and added another 1.93% to close at $1,973.

There is chaos in all markets, and I am surprised how well domestic equities have held up—so far.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}