ETF Tracker StatSheet

You can view the latest version here.

S&P 500 SCORES ITS BEST WEEK SINCE JUNE

- Moving the markets

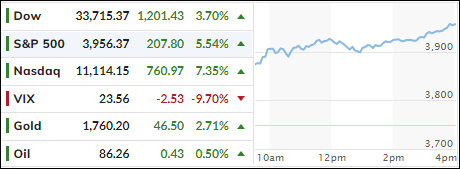

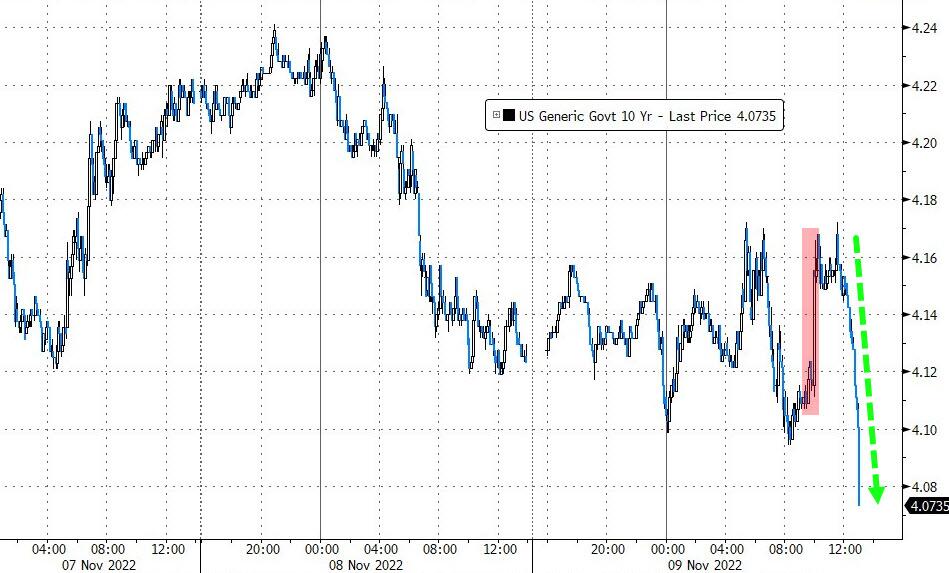

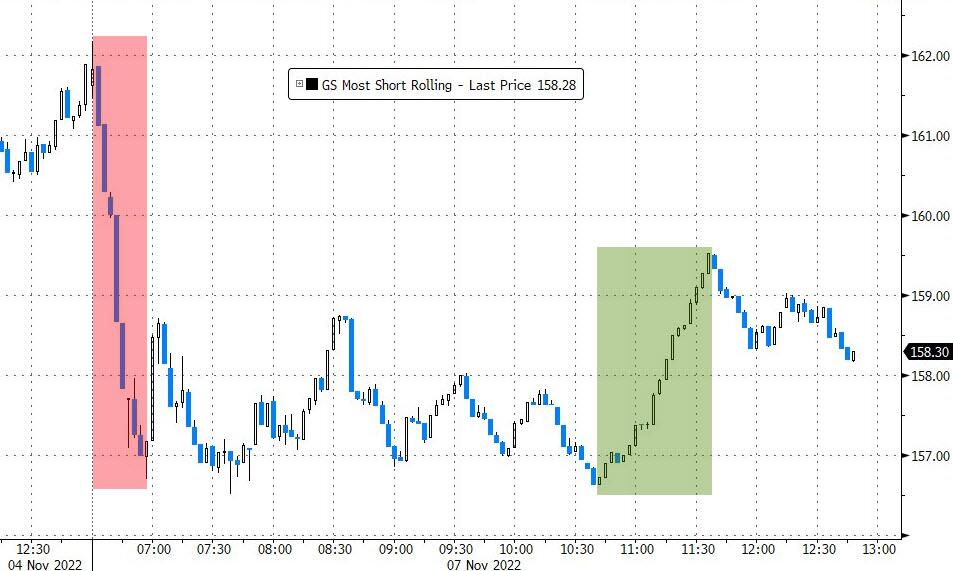

After yesterday’s euphoric reaction to the better-than-expected CPI report, bullish momentum prevailed throughout the session, despite the bond market being closed on this Veteran’s Day. But the short squeeze was alive and well and contributed to another positive ending.

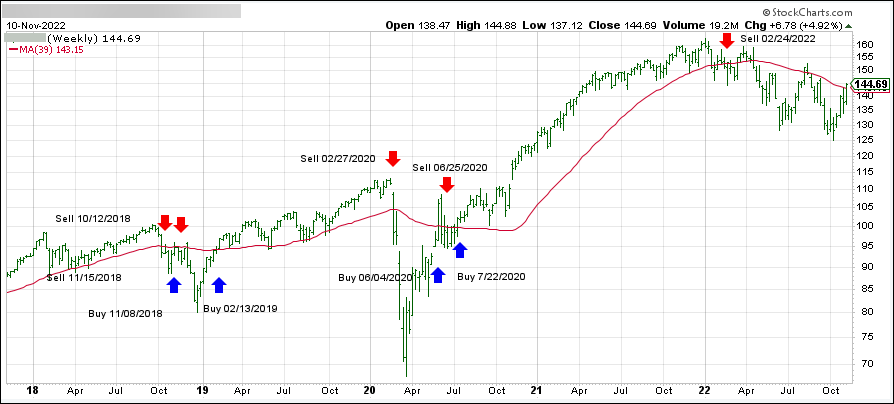

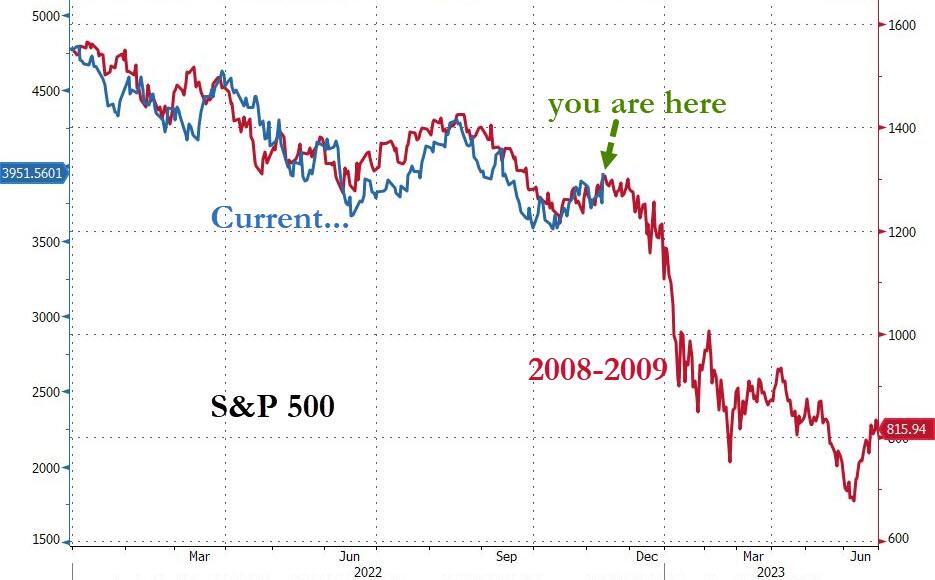

Again, hopes that the Fed would be slowing its interest rate hikes, and therefore supporting equities, was the main driver for the S&P scoring its best week since the June rebound. However, that one ended in a bearish disaster only two months later when the index’s 200-day M/A turned out to be the reversal point to new yearly lows.

This scenario seems to be repeating itself, as the S&P 500 is only 2.16% away from a second attempt to break through that resistance level. If it’s successful, I could see more upside potential. However, if the 200-day M/A turns out to be another impenetrable overhead ceiling, this feel-good CPI rebound may bite the dust.

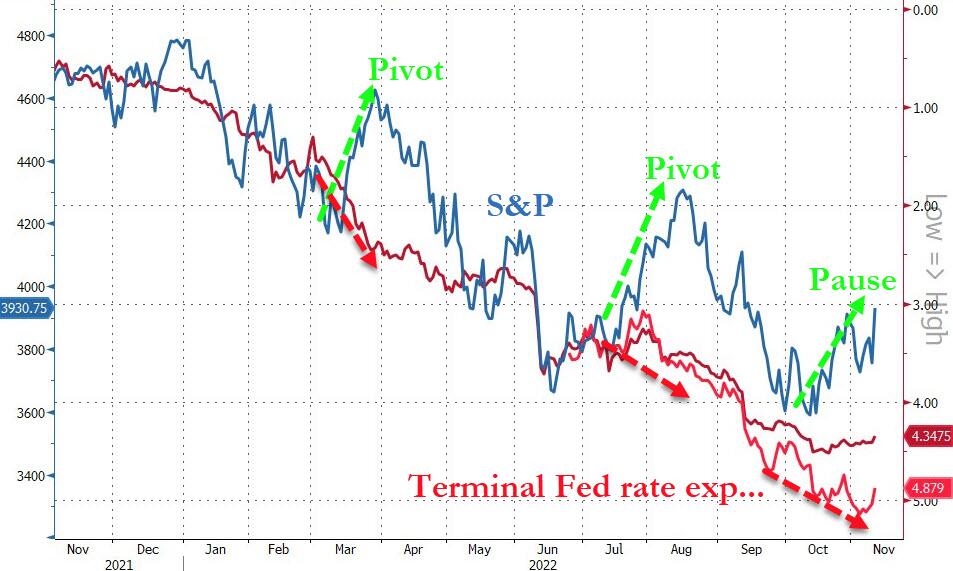

The future for a sustainable rally in equities lies with the Fed and its intentions not only how high they might hike but also for how long. Despite Fed head Powell and its various mouthpieces spewing nothing but hawkish comments, the Wall Street crowd remains convinced that a pause or a pivot is on deck, hence the frontrunning efforts.

Today, it was Boston Fed President Susan Collins, who uttered these words:

- I think that as we have raised rates that the risk of over tightening has increased.

- I do think we’re going to need to raise rates further.

- A smaller, more “deliberate” rate increase should not be confused for a sign that the Fed is backing down from the task of curbing price pressures.

To me, that does not sound like a Fed that is about to pivot…

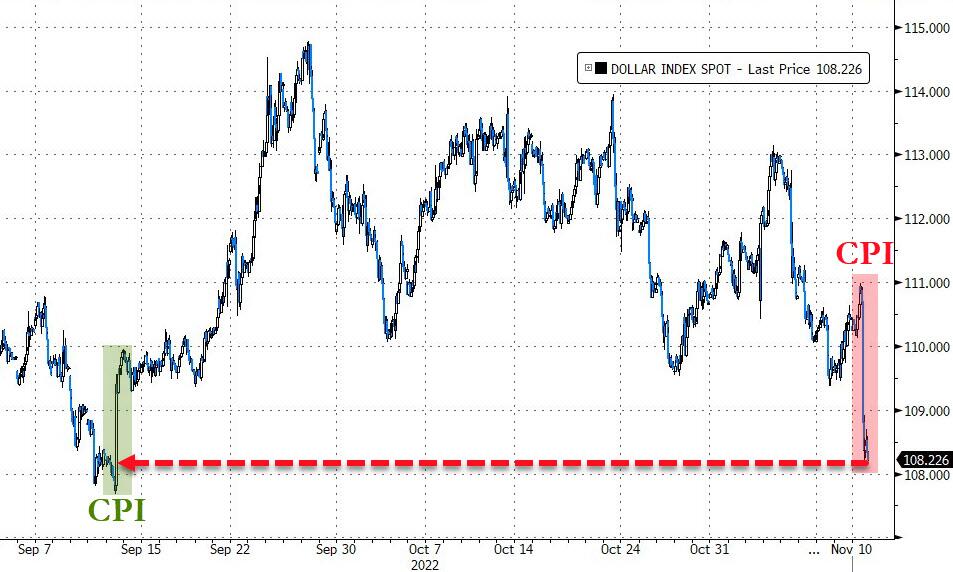

The US Dollar spanking continued, as ZeroHedge reported, with the world’s reserve currency down 5 of the last 6 days. It has lost 5% against its fiat peers and has broken its 50- and 100-day M/As on its way to 3-month lows.

Gold was the beneficiary and closed at $1,770, its highest in 3 months while scoring its best week since March 2020.

According to this analog, we are still in a bear market rally, although my Domestic Trend Tracking Index (TTI-section 3) has crossed its trend line into bullish territory. We should see more clarity next week—in one way or another.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}