ETF Tracker StatSheet

You can view the latest version here.

TREADING WATER

- Moving the markets

Despite the tough language used by St. Louis’ Fed President Bullard yesterday, that a benchmark interest rate in the range of 5%-7% would be needed to bring down inflation, the Wall Street crowd refuses to pay attention and still lives the dream that the Fed will soon have to pivot (lower rates).

For weeks now, a variety of other Fed mouth pieces having been singing similar tunes from the same hymn book to no avail, as traders and algos alike continue to focus on the hope that peak inflation and peak rates are now clearly visible in the rearview mirror, and that good times for the markets are ahead of us.

Added ZeroHedge:

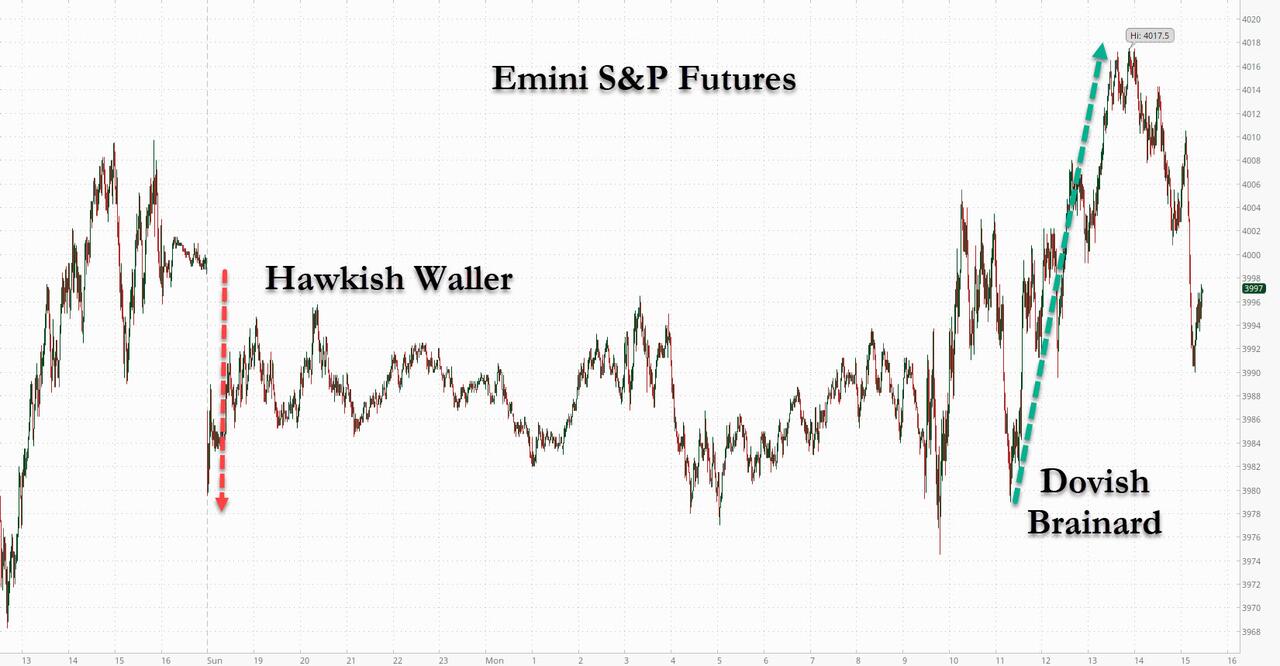

- 16 different speeches from Fed speakers this week – all with the same message: higher rates for longer; no pause or pivot imminent…

And in more detail:

- Bostic: more rate-hikes needed, “must keep rates at peak” until inflation on track for 2%

- Bullard: rates could rise to 7%, “burned two years in a row on inflation optimism”

- Waller: Fed still has “long way to go” on rate-hikes

- Daly: “pause is off the table“

- Kashkari: “not seeing evidence of underlying demand cooling“, “not there yet” to pause rate-hikes

- Collins: 75bps still on the table, “no clear evidence that inflation coming down”

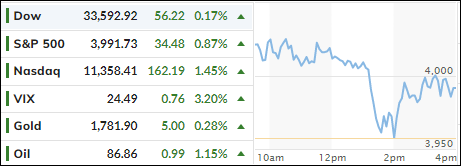

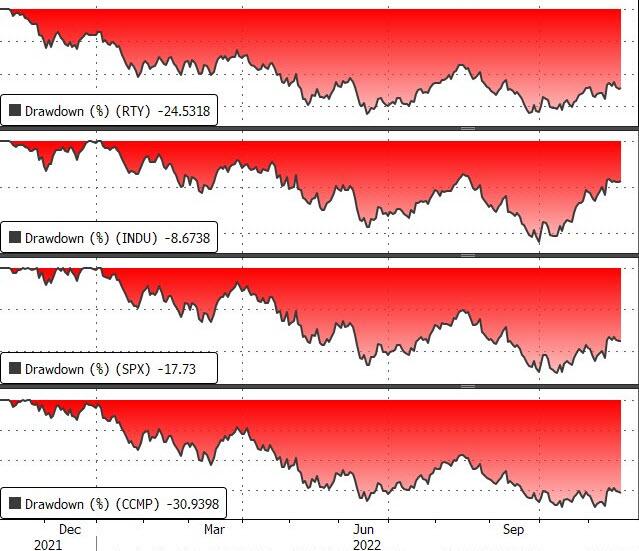

Suffice to say that, after last week’s Ramp-A-Thon, things slowed down during the past 5 trading days, during which the major indexes went nowhere with the S&P 500 surrendering a modest -0.7%. For the month, however, all are showing positive numbers from the CPI induced rebound.

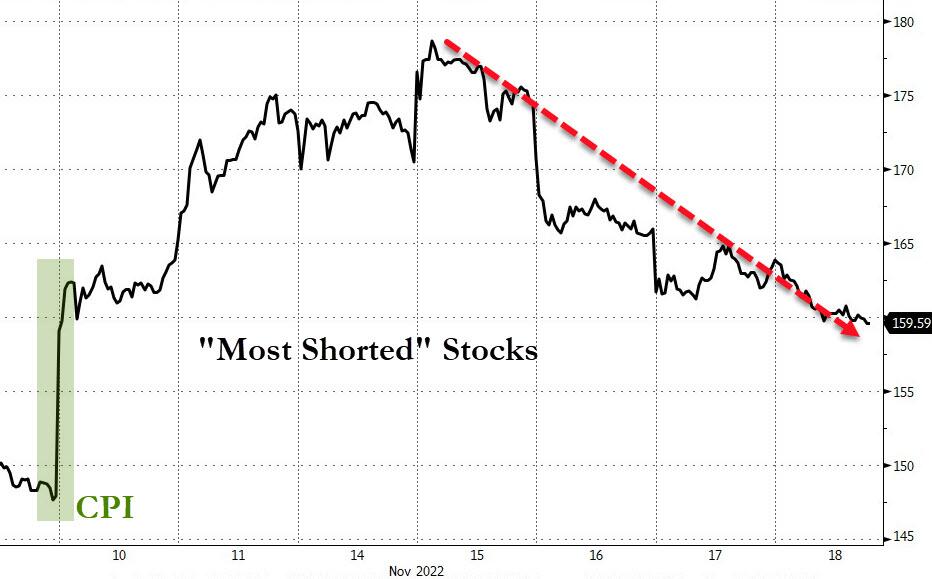

The lack of upside follow through can also be attributed to the “dying short squeeze,” as most shorted stocks did what they are supposed, namely go down. You could pretty much say that for the entire market which, as ZeroHedge pointed out, headed south with utter abundance.

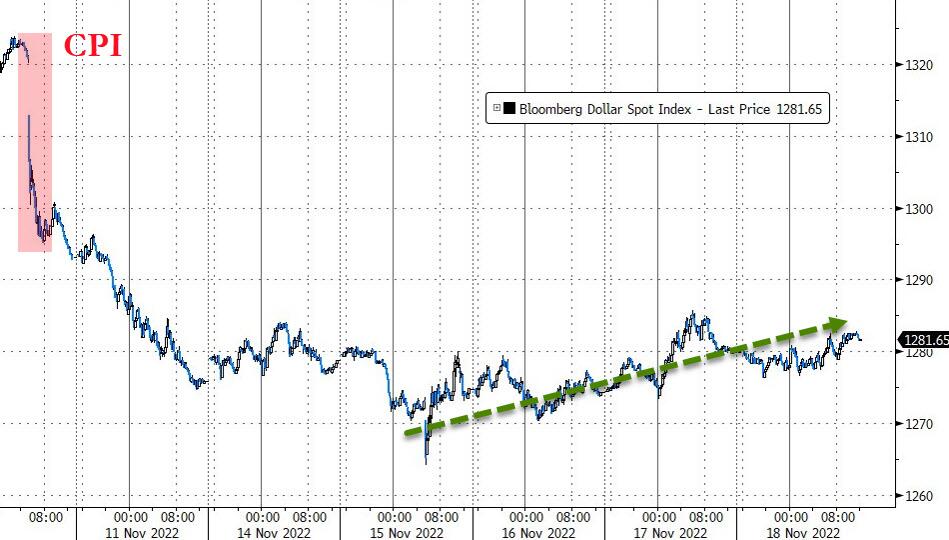

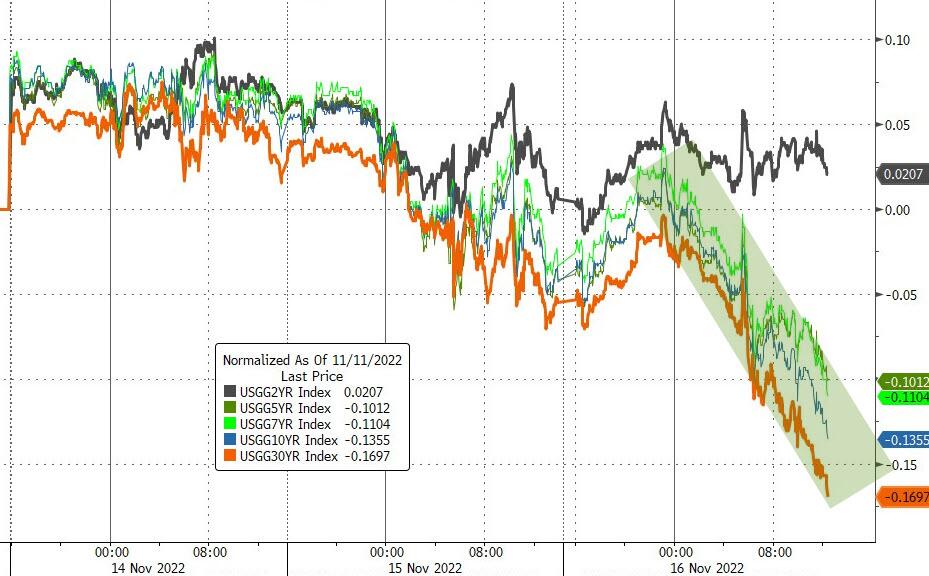

Bond yields were mixed with the 2-year pumping and the 30-year dumping. The US dollar edged higher, while gold slipped but held on to its $1,750 level.

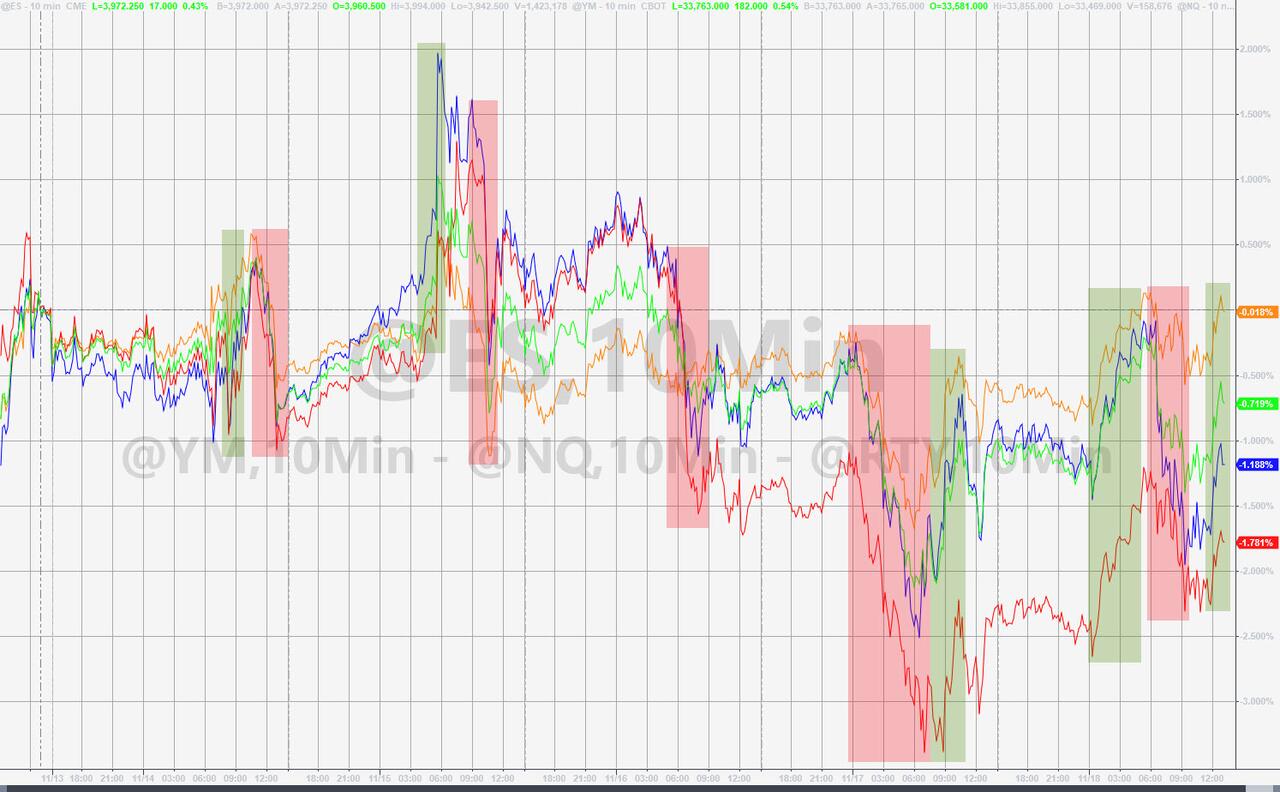

From a directional point of view, our Trend Tracking Indexes (TTIs) performed the trend line dance with not much won or lost, and no clear direction is discernable at this time (section 3).

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}