- Moving the markets

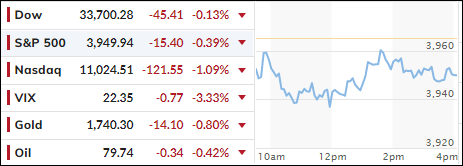

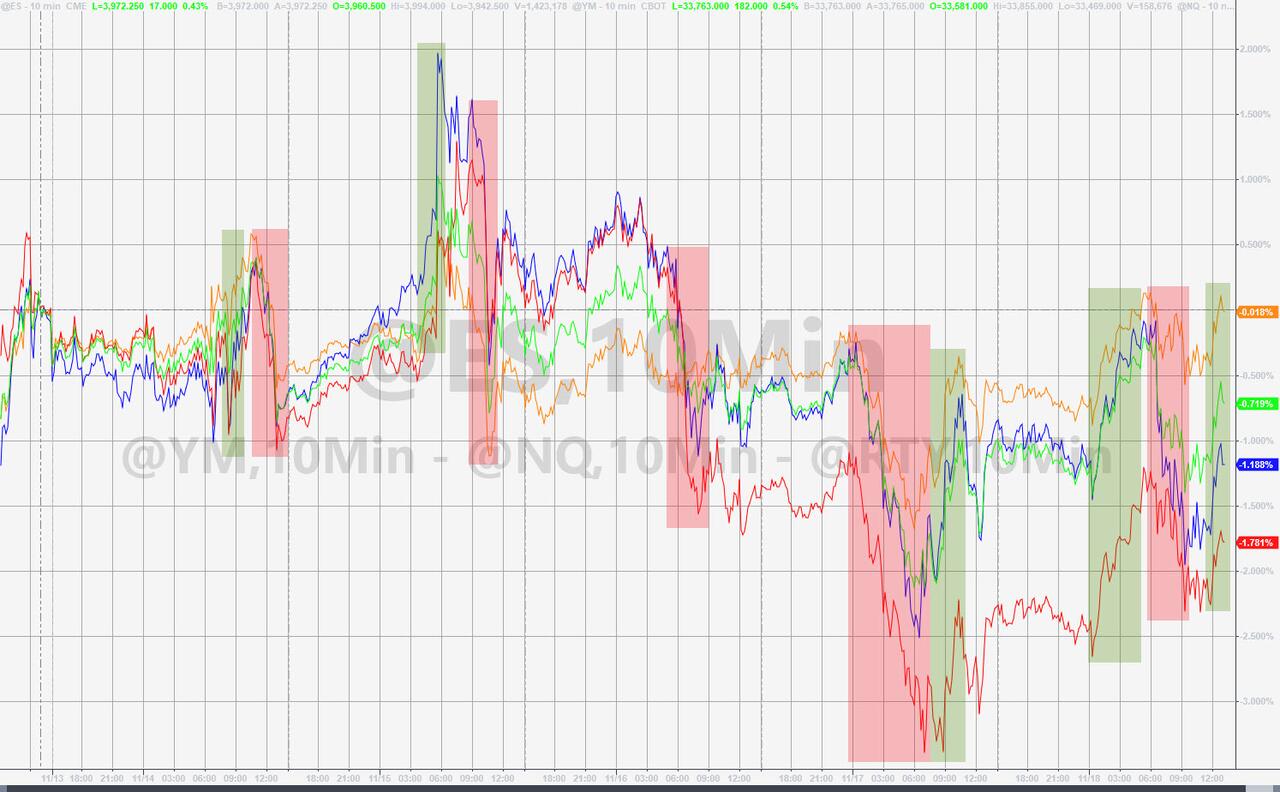

The efforts by a few traders last week to push the markets higher on very low volume came to an end today, when the full staff returned, pushed the sell buttons, and pulled the rug out from under last week’s rally.

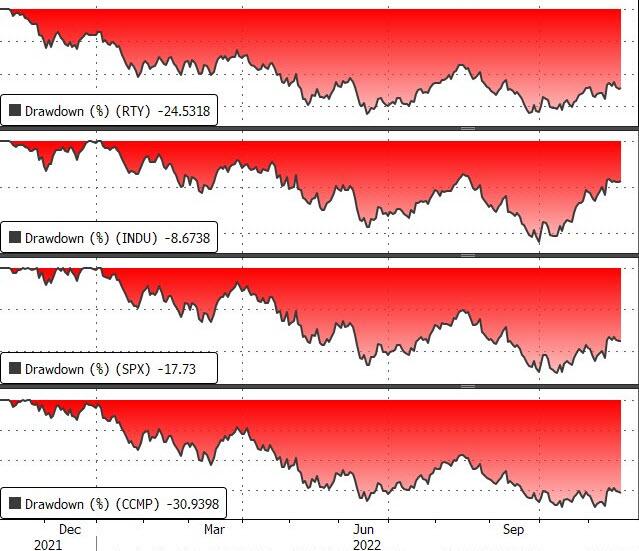

The major indexes shifted into bearish mode, right after the opening bell rang, and never stopped thereby wiping out all the Thanksgiving week gains. Our pending “Buy” signal has therefore been put on the backburner for the time being, as recent upward momentum has now been neutralized (section 3).

This long Holiday weekend introduced more disruptions to the bullish sentiment, as China’s social unrest, caused by extreme Covid restrictions, had local governments tightening their control over the population. That destroyed reopening hopes and put a downer on the world’s second biggest economy in terms of production and shipping.

Domestically, we were treated with a barrage of hawkish messages from a variety of Fed speakers, which ZeroHedge summarized as follows:

- 0950ET *MESTER SAYS SHE DOESN’T THINK FED NEAR A PAUSE IN TIGHTENING, NEED TO SEE SEVERAL MORE GOOD INFLATION READINGS

- 1200ET *WILLIAMS SAYS FED STILL HAS MORE WORK TO DO ON INFLATION, FURTHER TIGHTENING SHOULD HELP REDUCE INFLATION

- 1200ET *BULLARD: RISK THAT FED WILL HAVE TO GO HIGHER ON RATES IN 2023, MARKETS UNDERPRICING RISK FOMC MAY BE MORE AGGRESSIVE, FED HAS `A WAYS TO GO TO GET TO’ RESTRICTIVE RATES, FIRST 250 BPS OF TIGHTENING WAS JUST GETTING TO NEUTRAL, TIME TO LET QT PROGRAM RUN FOR NOW; SO FAR, SO GOOD

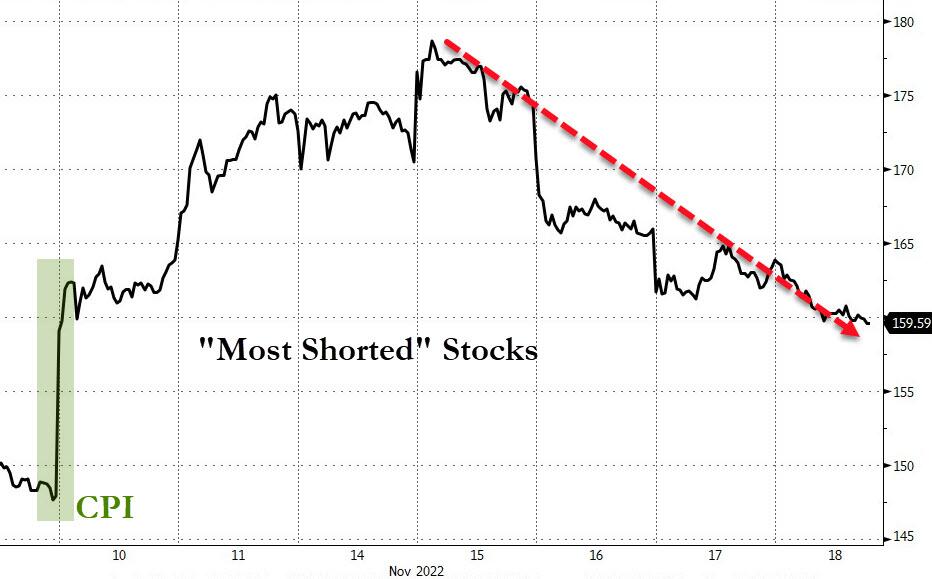

This was the final nail in the bearish coffin, and down we went. Even the most shorted stocks were not squeezed today, so they followed their natural tendencies, namely lower.

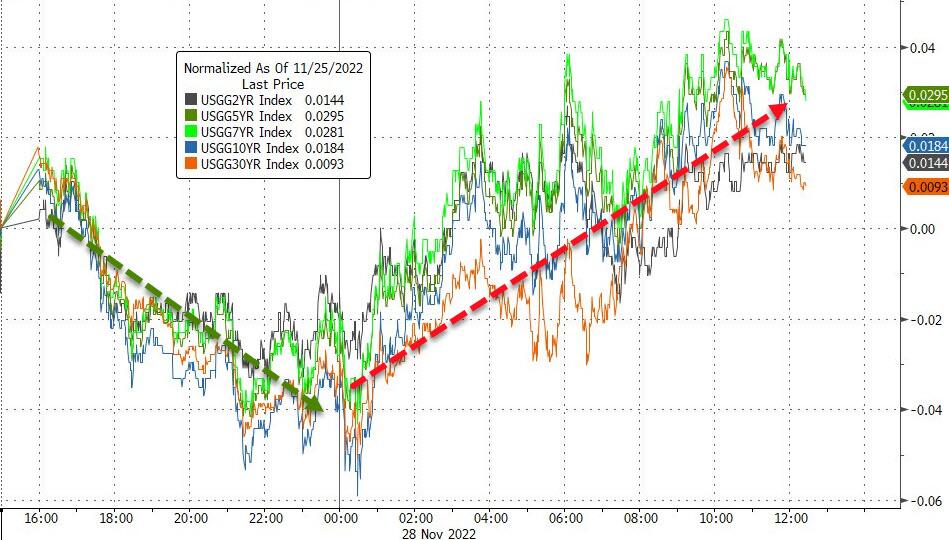

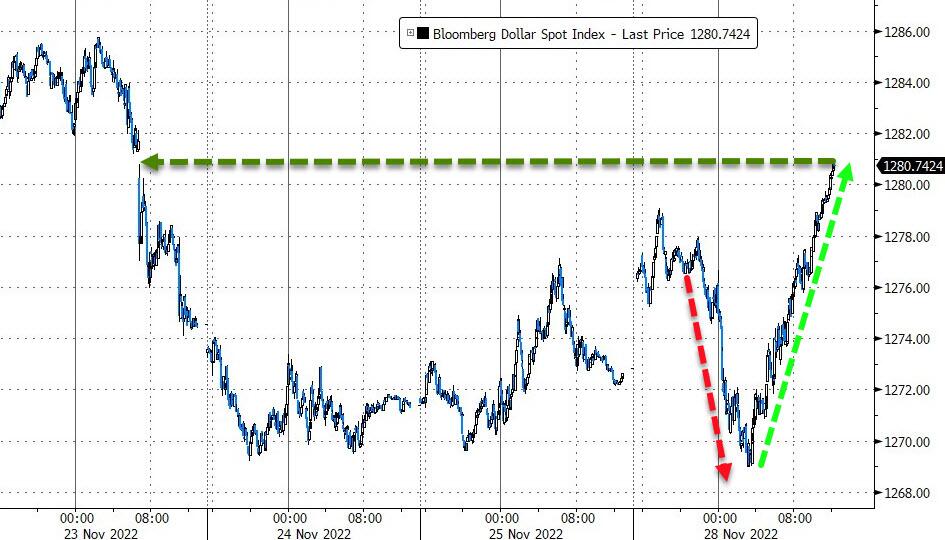

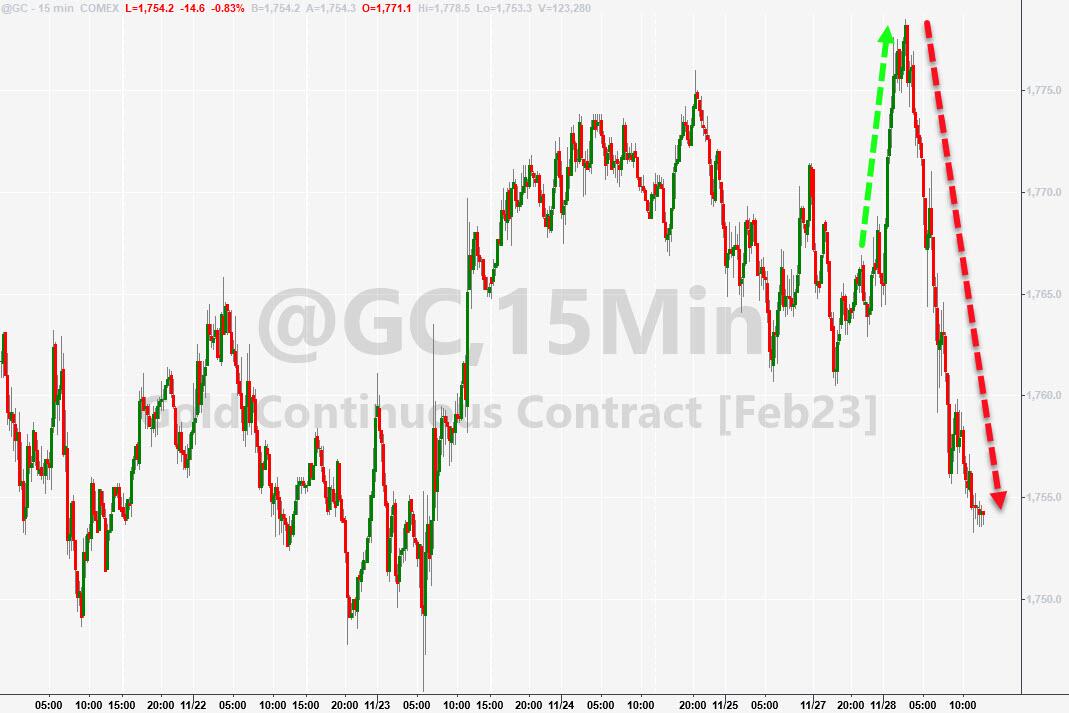

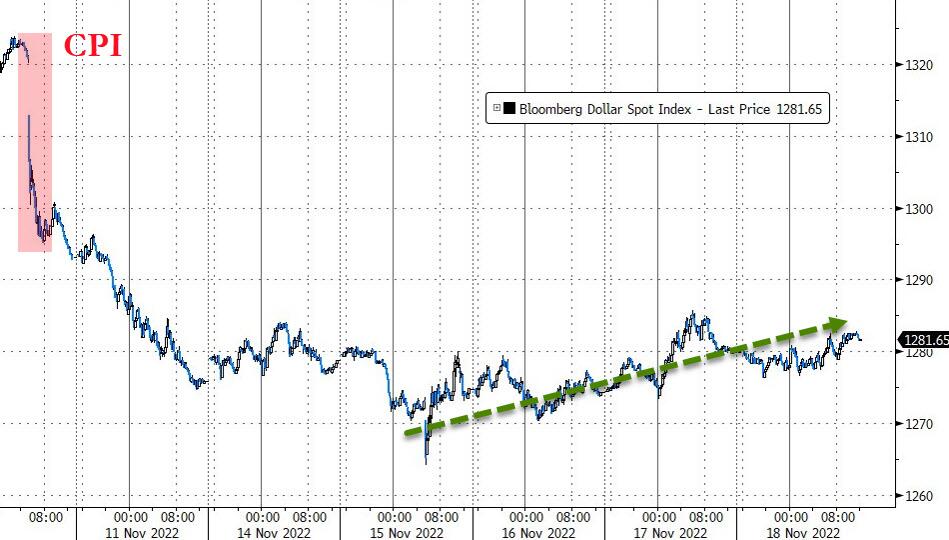

Bond yields retreated with the 10-year ending just about unchanged at 3.68%, as the US Dollar rode a rollercoaster in the process reversing recent losses. Gold followed suit but ended the day lower.

The S&P 500 has reached another critical point, namely its 200-day M/A, which is now in striking distance. Will we see a “threepeat,” or will the index finally break through this stubborn resistance level and support the bullish meme?

Only time will tell.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}