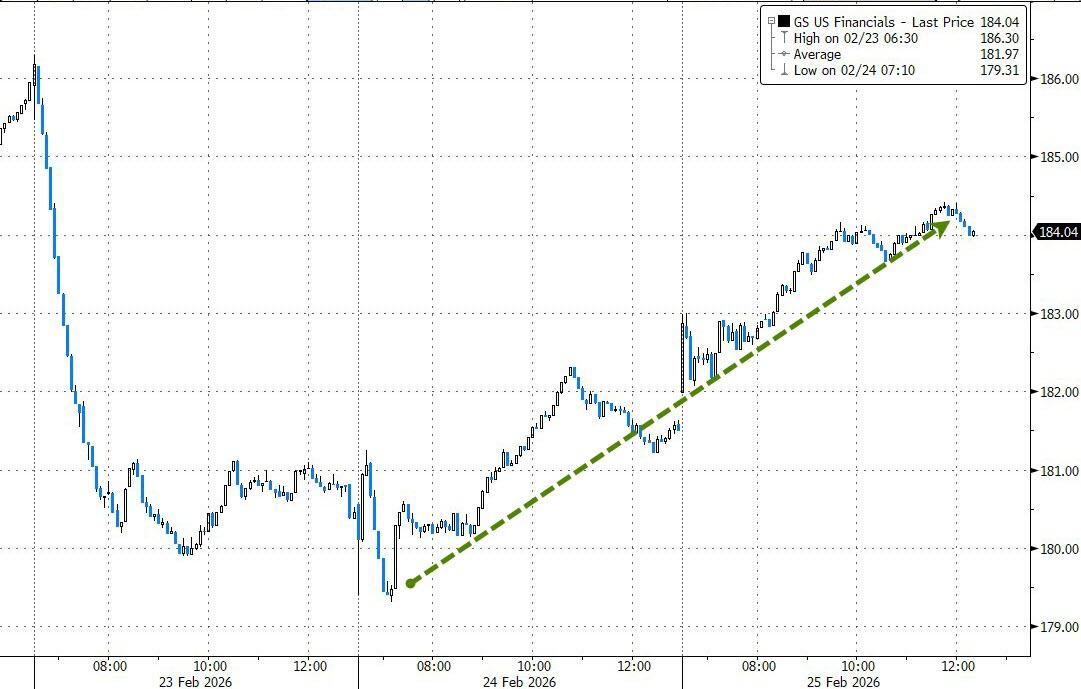

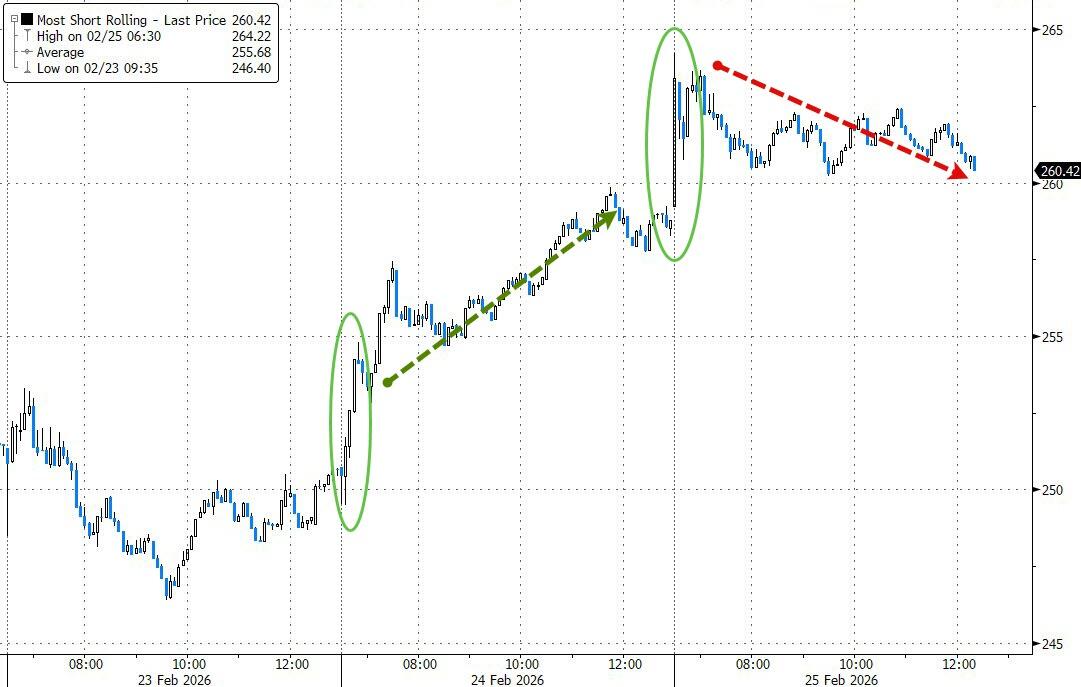

- Moving the market

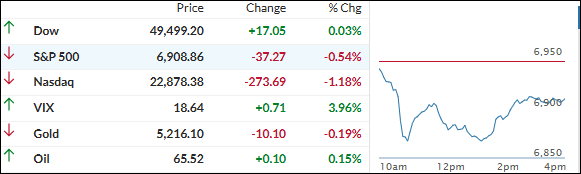

Stocks opened lower and stayed under pressure for most of the day, even after Nvidia and Salesforce dropped their latest earnings.

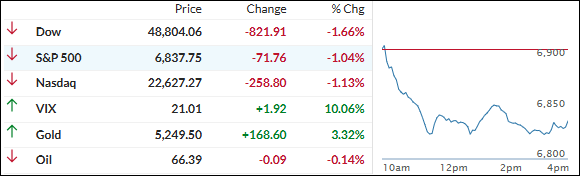

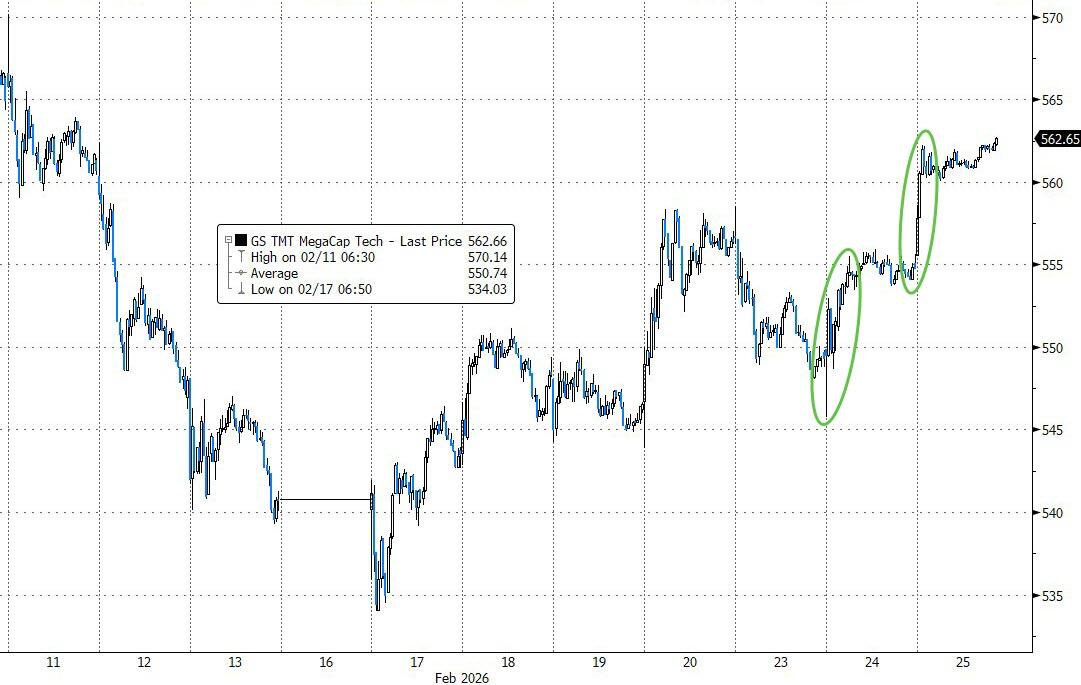

The big disappointment was Nvidia—despite beating on both earnings and revenue, shares got pumped early then dumped about 5%, putting it on track for its worst day since April.

Traders basically shrugged off the numbers and took profits. Other chip names followed suit: Broadcom, Lam Research, Western Digital, and Applied Materials all fell more than 6%.

Salesforce bucked the trend a bit, rising 2% after beating on both top and bottom lines, but it wasn’t enough to lift the broader tech sector.

The weakness ties back to ongoing fragility in software and cybersecurity—investors are still nervous about AI tools potentially disrupting incumbent vendors’ businesses. The Mag 7 were a big drag again, but the rest of the S&P 493 held roughly flat.

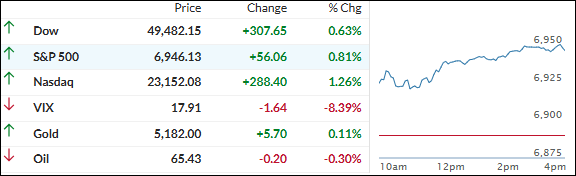

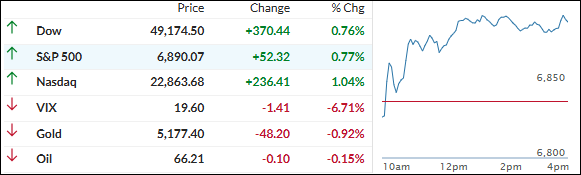

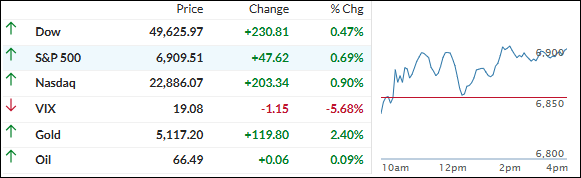

In the end, only the Dow and small caps managed small green closes—the Nasdaq was the day’s biggest loser.

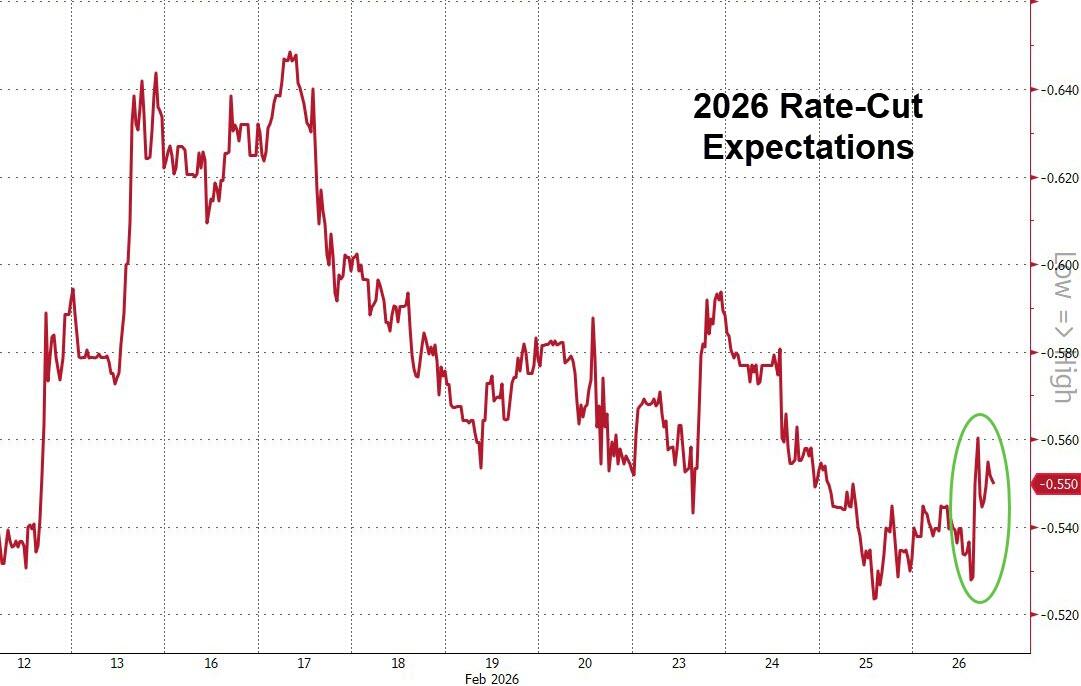

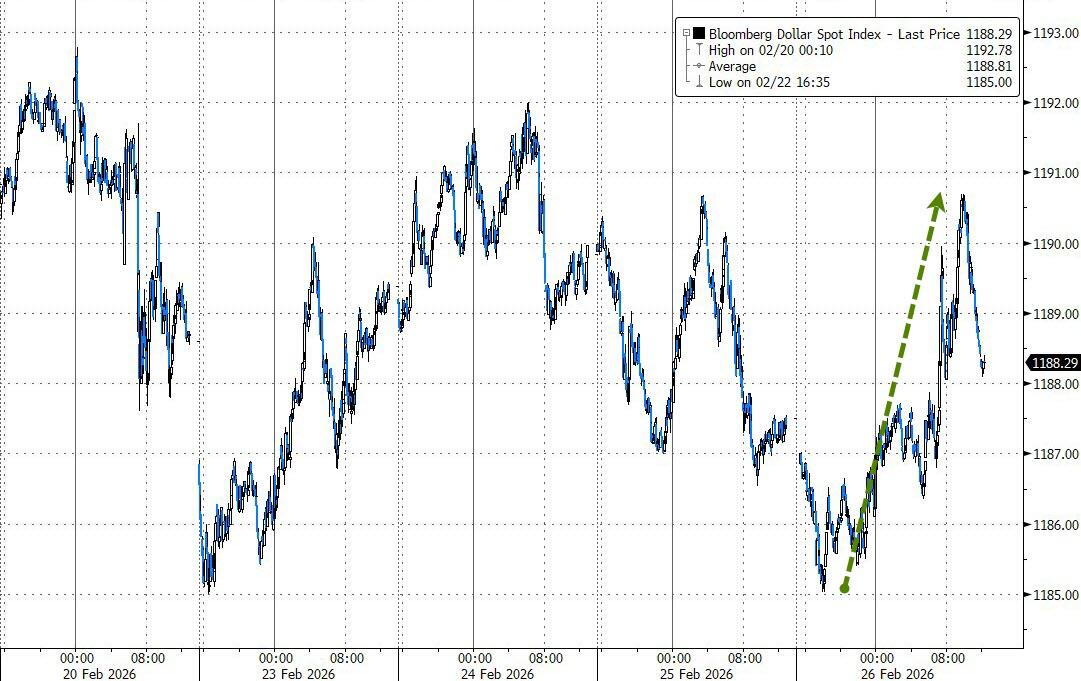

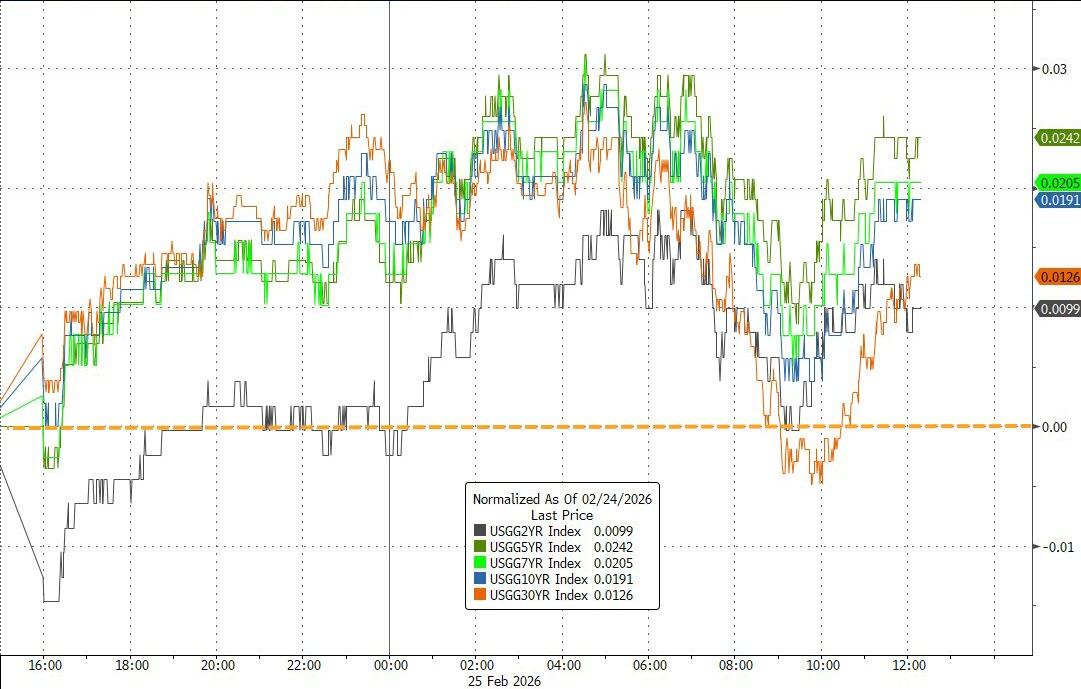

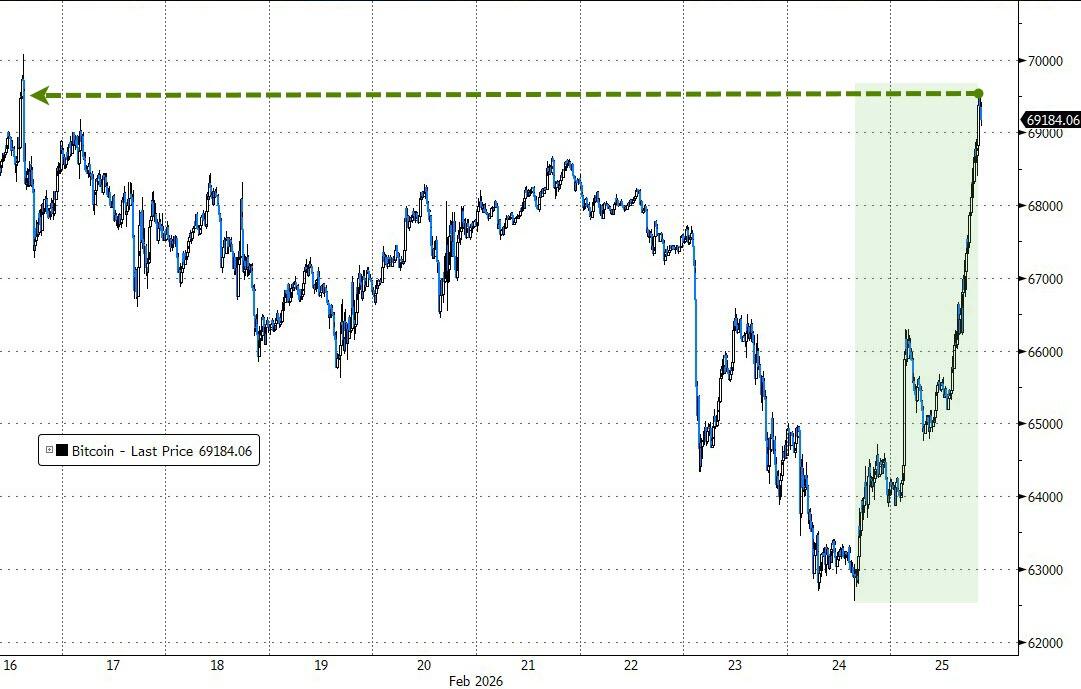

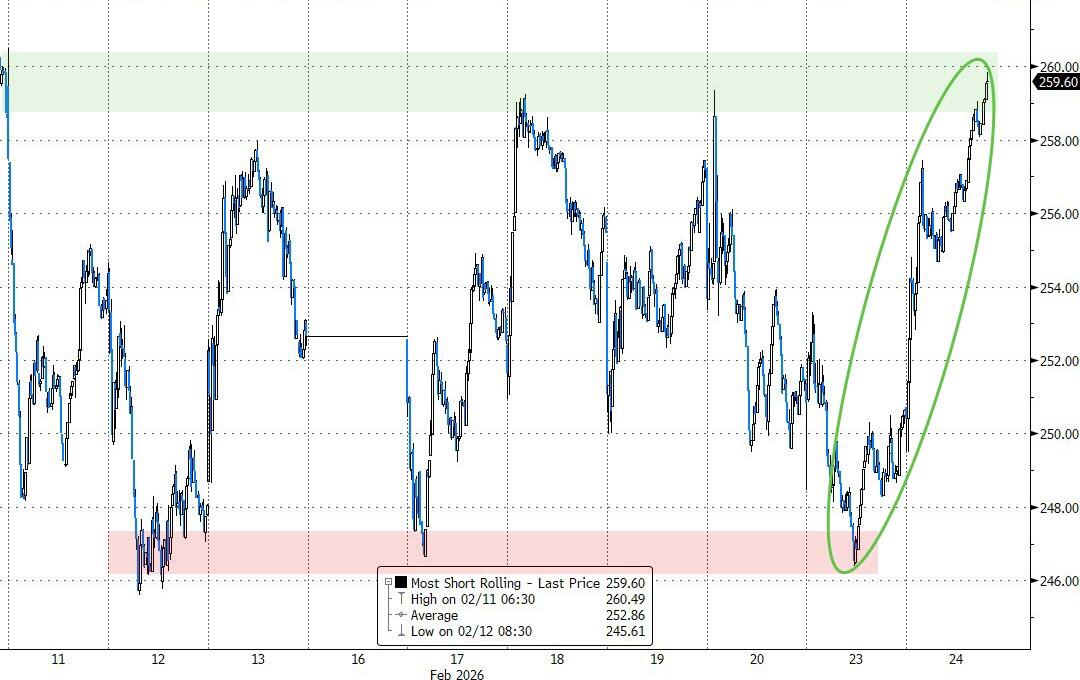

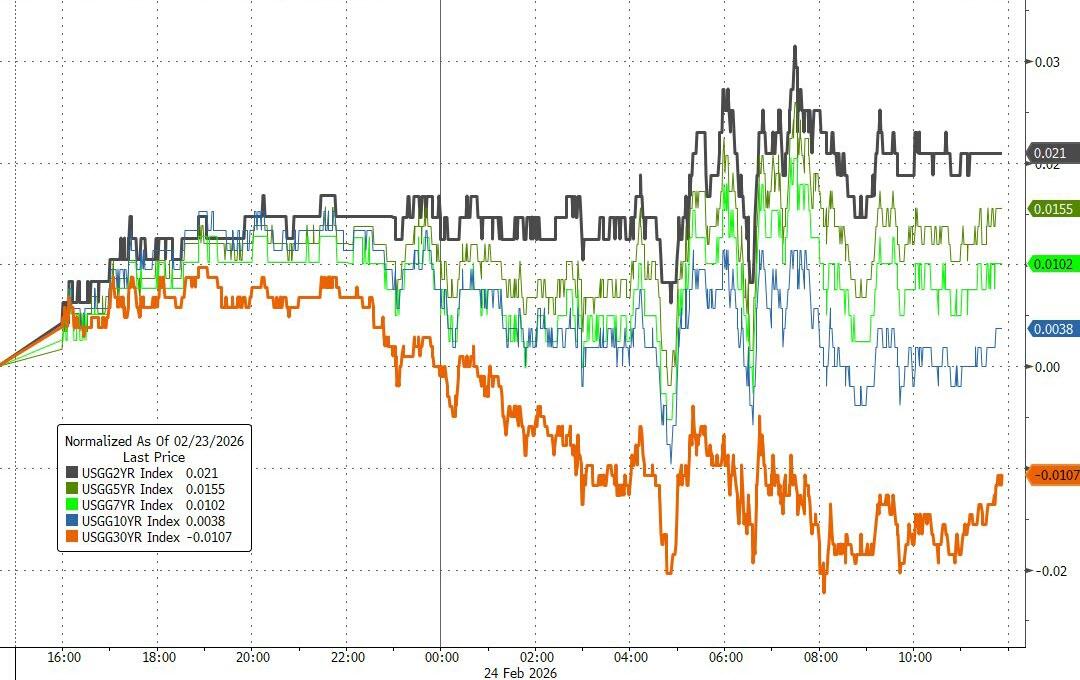

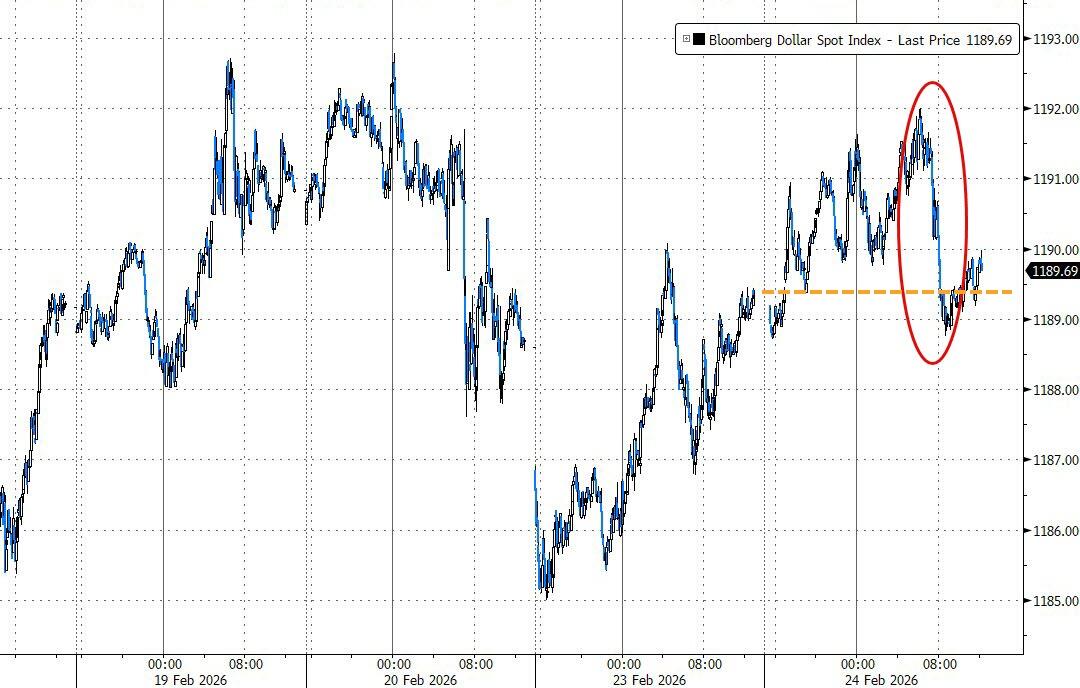

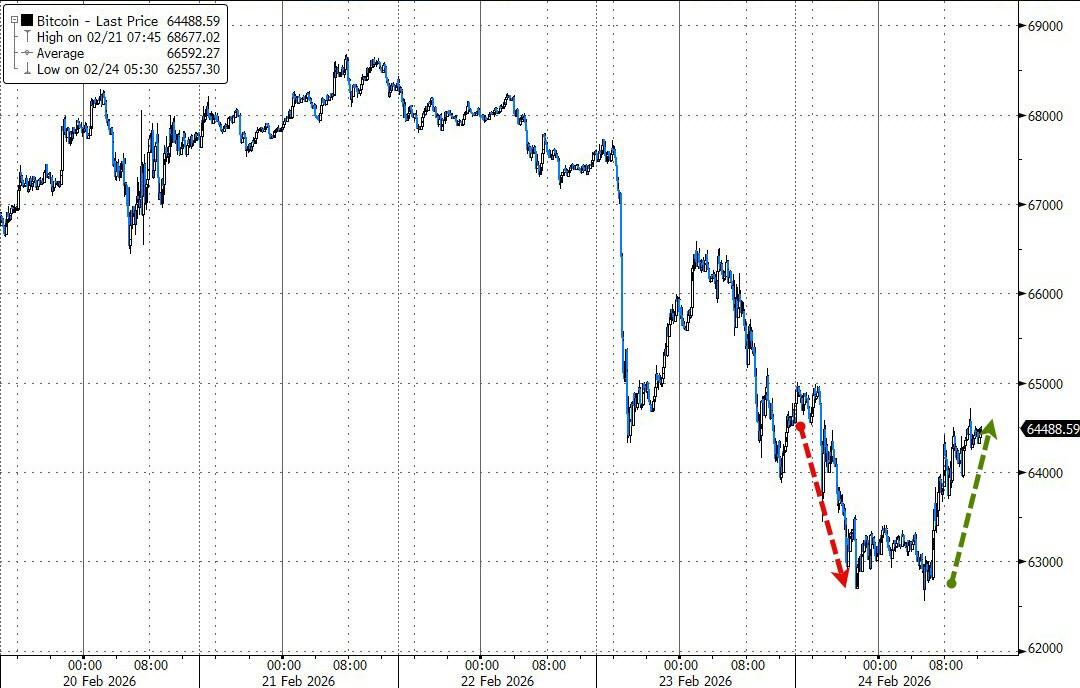

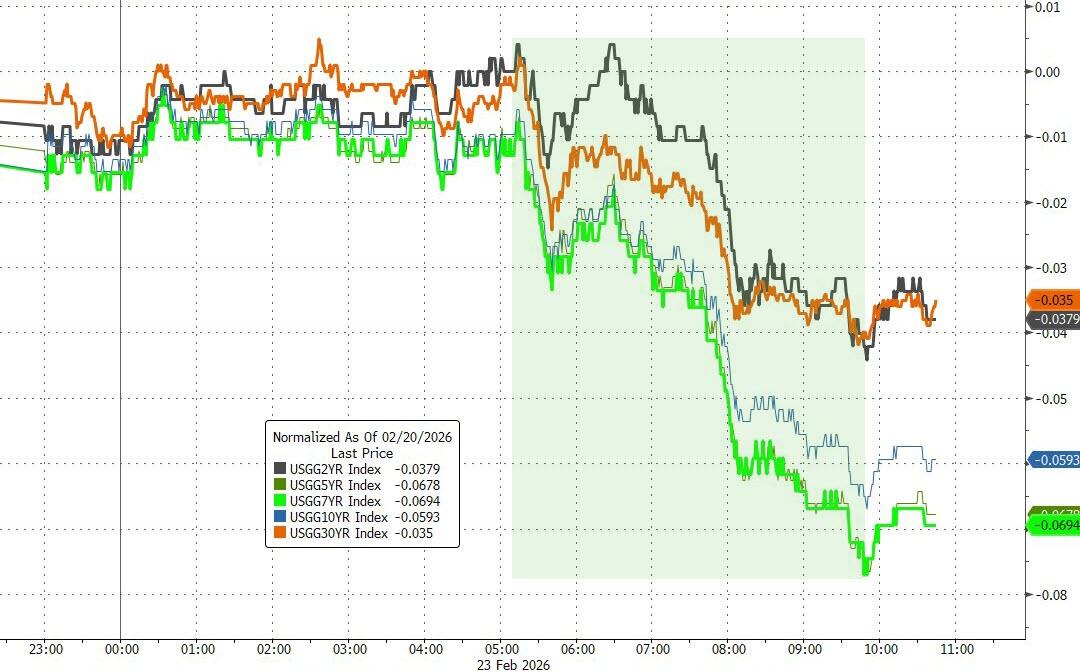

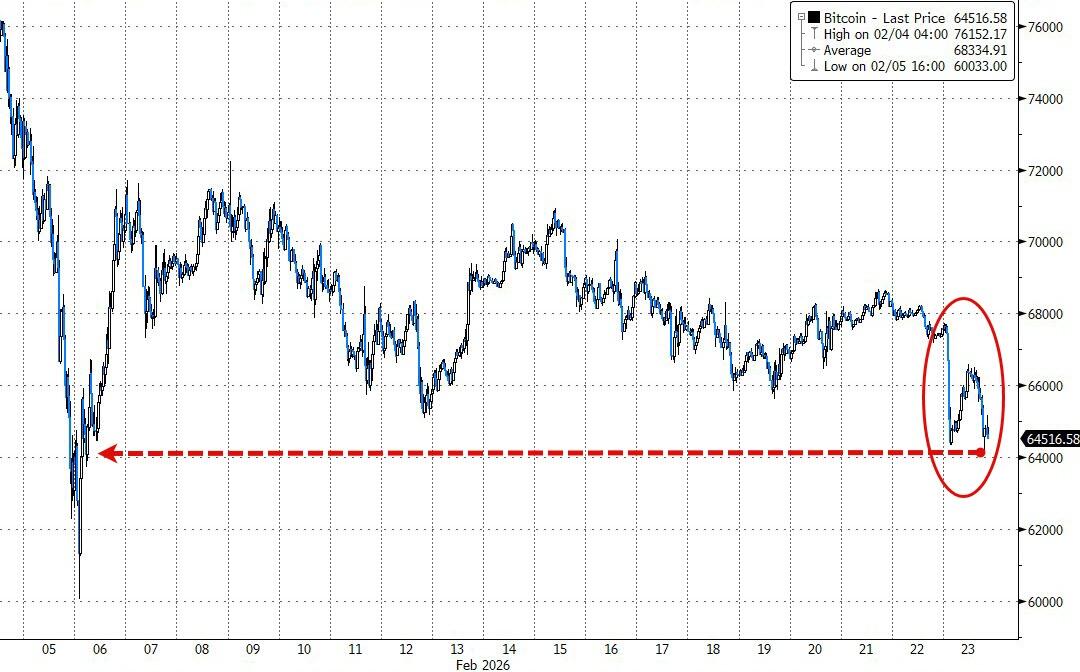

Bond yields eased (pushing rate-cut expectations higher), the dollar gained overall despite a late sell-off, and the metals were mixed: spot gold chopped between $5,150 and $5,200 but the gold ETF closed green, silver eked out a gain, and Bitcoin followed tech lower before bouncing back to $68k.

Today’s big question: why did Nvidia underperform after such a strong beat? Simple answer—classic “sell the news” profit-taking.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}