ETF Tracker StatSheet

You can view the latest version here.

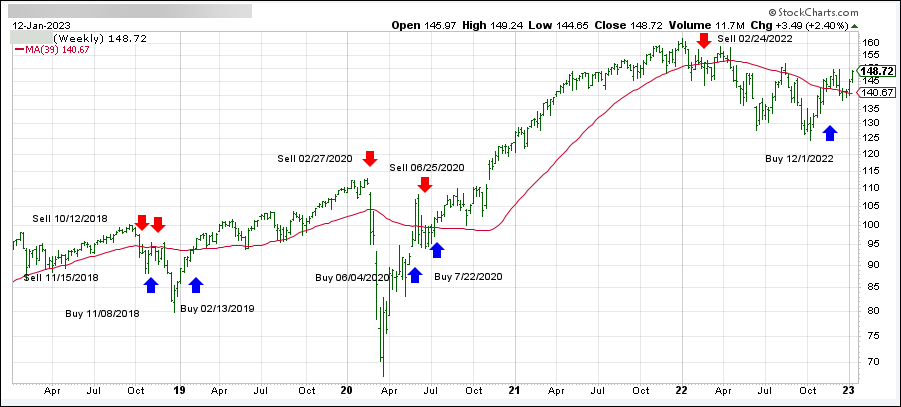

CONQUERING THE FLAT LINE

- Moving the markets

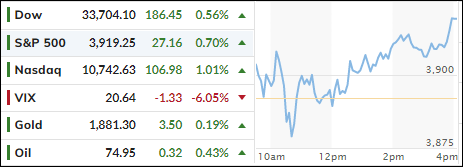

After digging themselves out of an early hole, the major indexes crawled back slowly and surely to end another session on a positive note.

Q4 bank earnings were on the agenda, as JP Morgan beat revenue expectations but warned that it’s setting aside more money, an increase of 49% from Q3, to cover credit losses for what they termed a “mild recession.” The stock slipped initially but recovered late in the day.

Wells Fargo (WF) disappointed, with the stock dropping 4%, and BofA as well slid despite better-than-expected Q4 earnings. WF also added that it’s preparing for the economy to “get worse than it’s been over the last few quarters.”

Still, the S&P recorded its best week since November, as MarketWatch pointed out, and scored its second winning week in a row but falling just short of reclaiming its $4k level.

On the economic front, the Consumer sentiment survey showed that 1-year inflation expectations dropped to 4%, vs. 4.3% expected, which is the lowest 1-year outlook since April 2021.

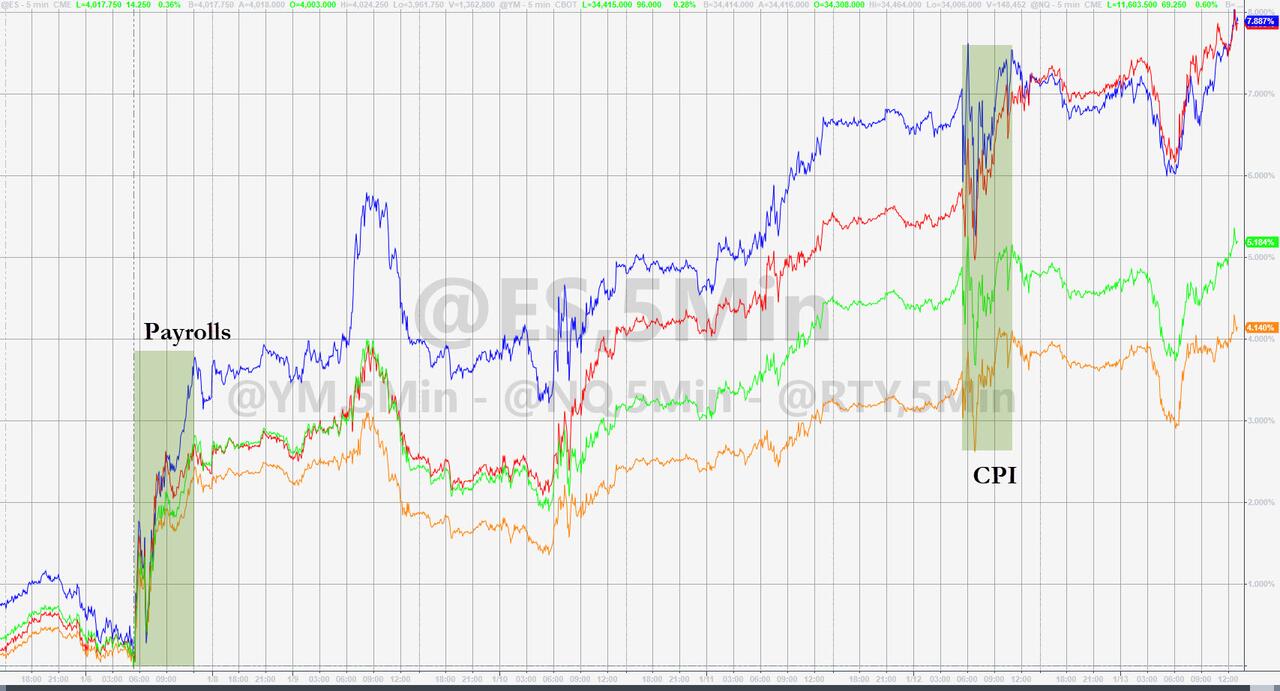

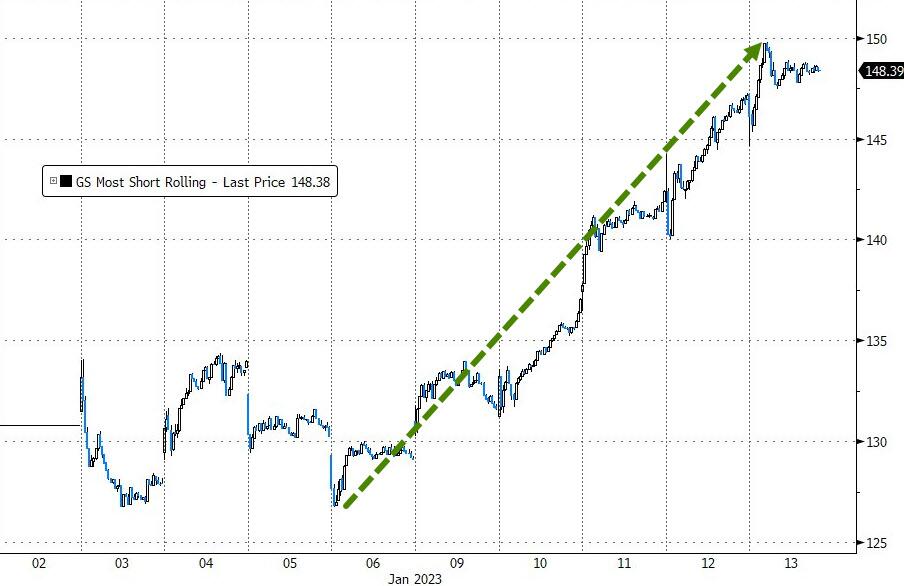

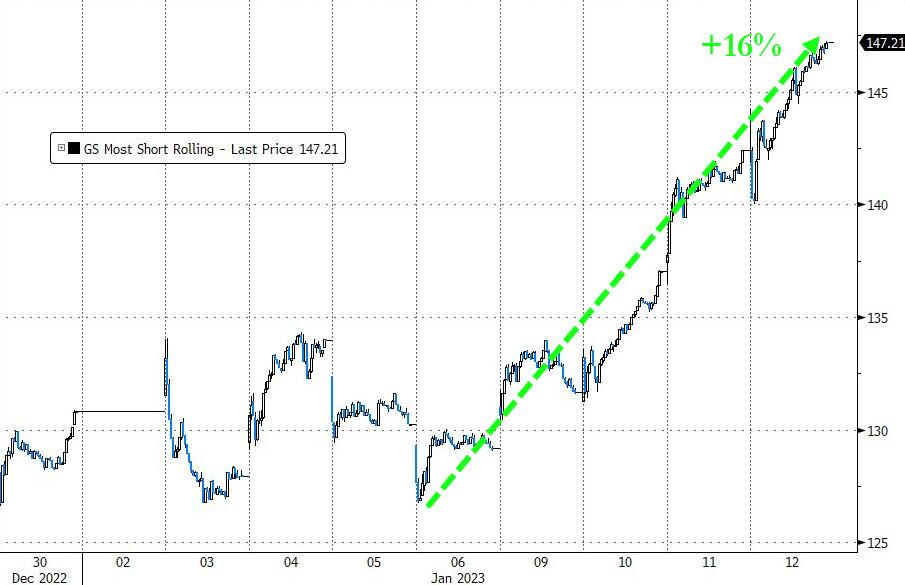

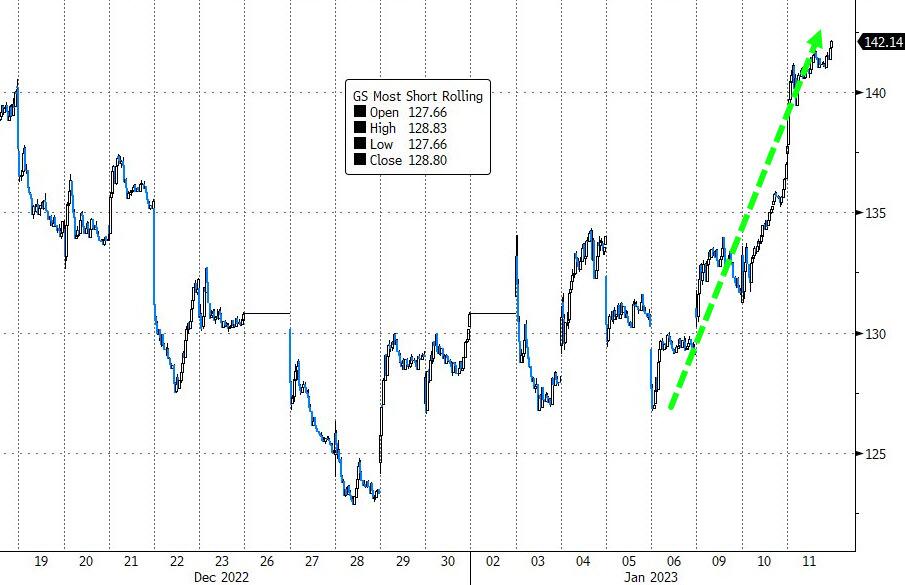

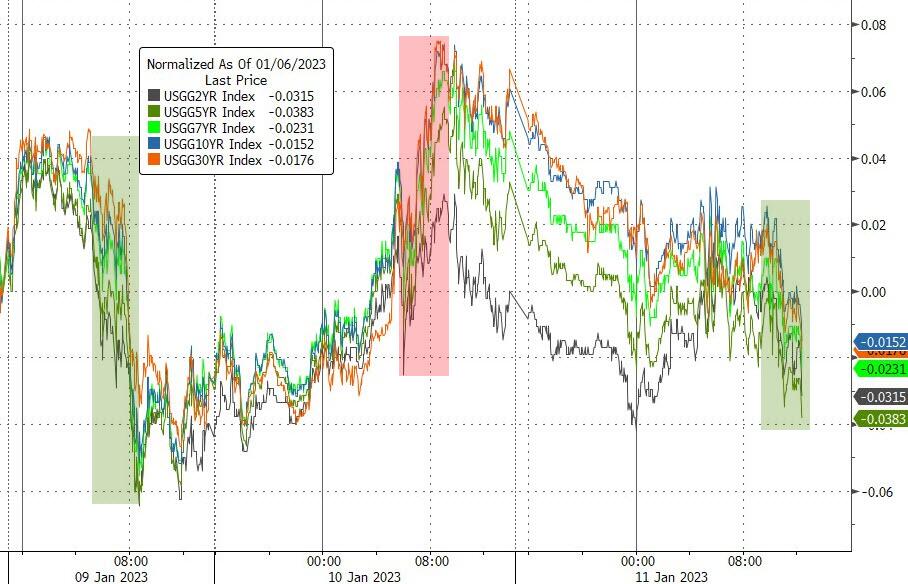

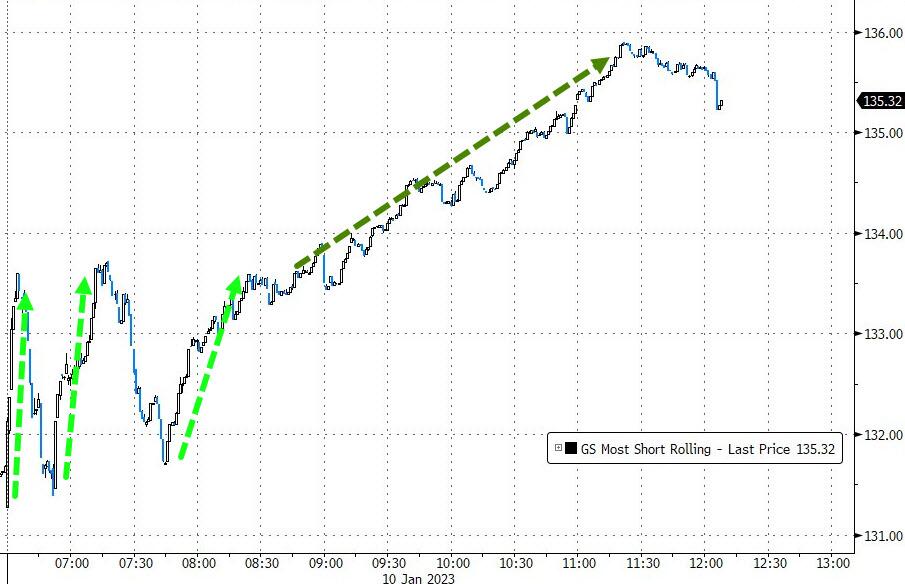

Again, the short squeeze continued unabated and has now pushed up the most shorted stocks an amazing 18% in the past week. Bond yields gave an assist this week by dipping lower, as Fed rate trajectory expectations drifted as well but bounced higher today, as ZeroHedge pointed out.

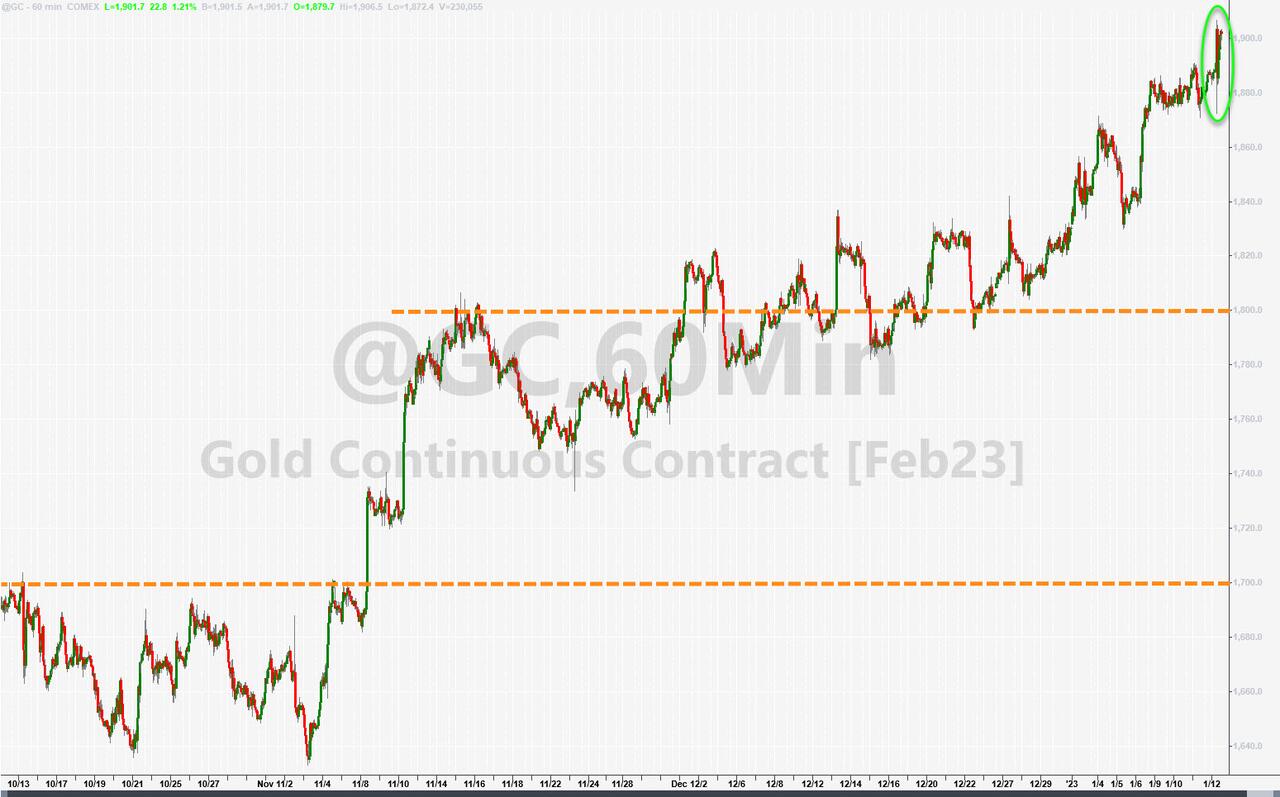

Gold continued its ramp to higher levels and has notched 6 straight days of gains to reach its highest level since April 2022. The precious metal triggered a golden cross, which is the moment in time when the 50-day M/A crosses its 200-day M/A, a very bullish sign.

Gold does well in an era of uncertainty, which Treasury Secretary Janet Yellen seemed to indicate we are heading into, when she said that the US will hit the debt ceiling next Thursday, an event which analysts referred to as “significant market pain.”

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}