- Moving the markets

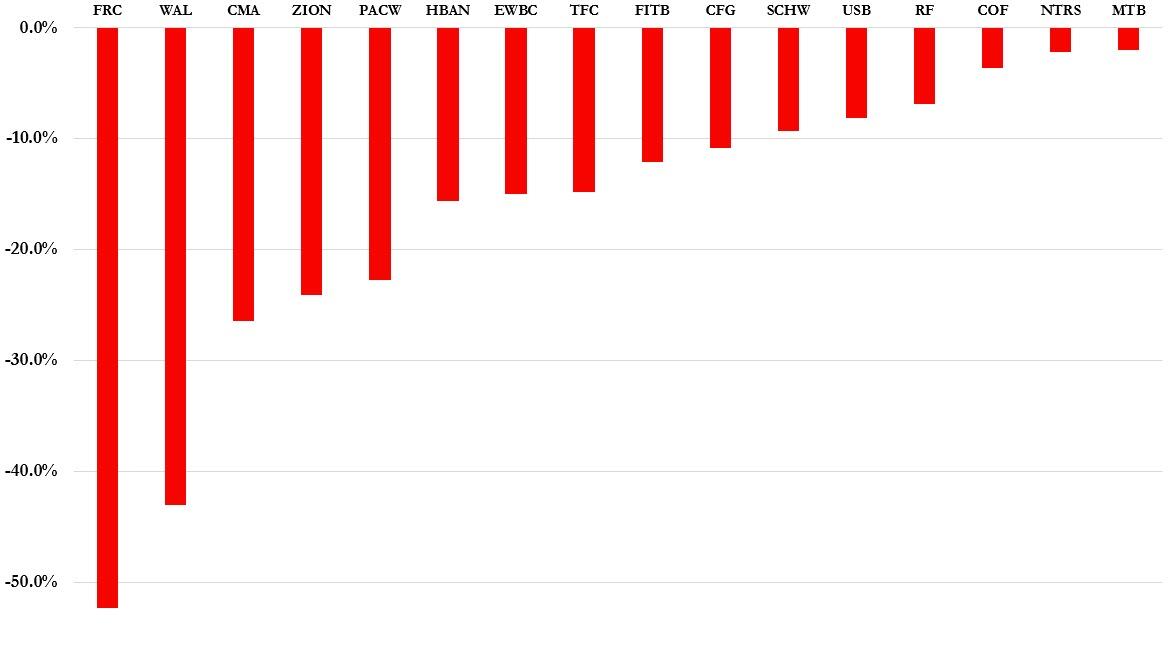

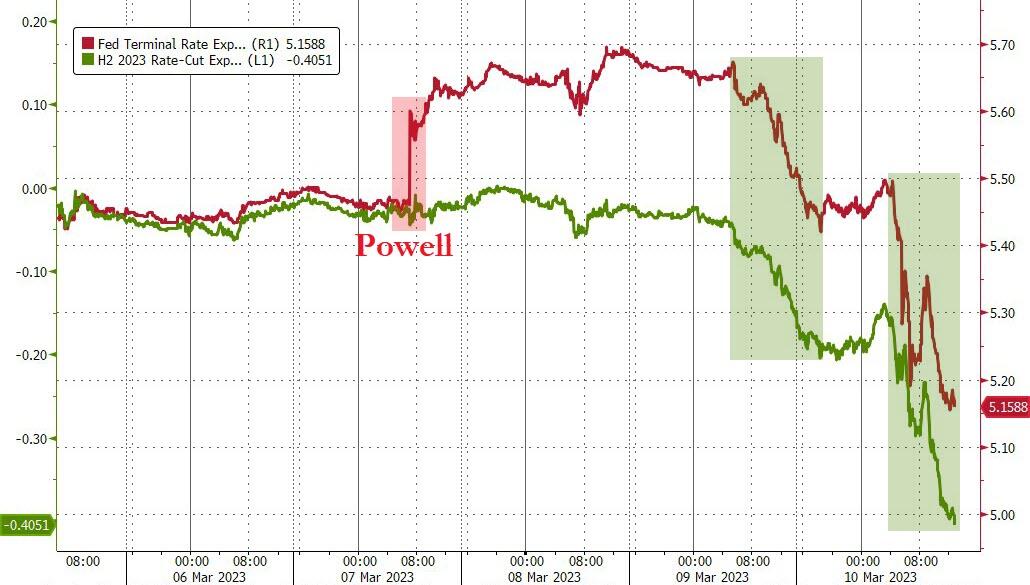

Apparently, Fed head Powell, Treasury Secretary Yellen and the head of the FDIC must have been in panic mode, as they combined forces by announcing (on Sunday) a plan that would backstop ALL depositors in the failed Silicon Valley Bank, while concurrently making additional funding available for other banks. Regional banks are not looking too good given their current losses, as well as the status of their regional bank index KRE.

The joint statement also assured depositors that they would have access to their money as of today. This action was the equivalent of pulling the cord for the backup parachute, as the domino effect of citizens withdrawing their funds would have accelerated with lightning speed.

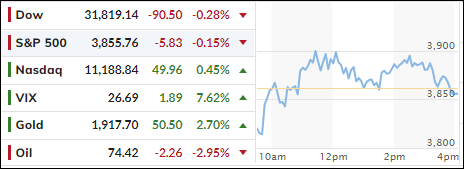

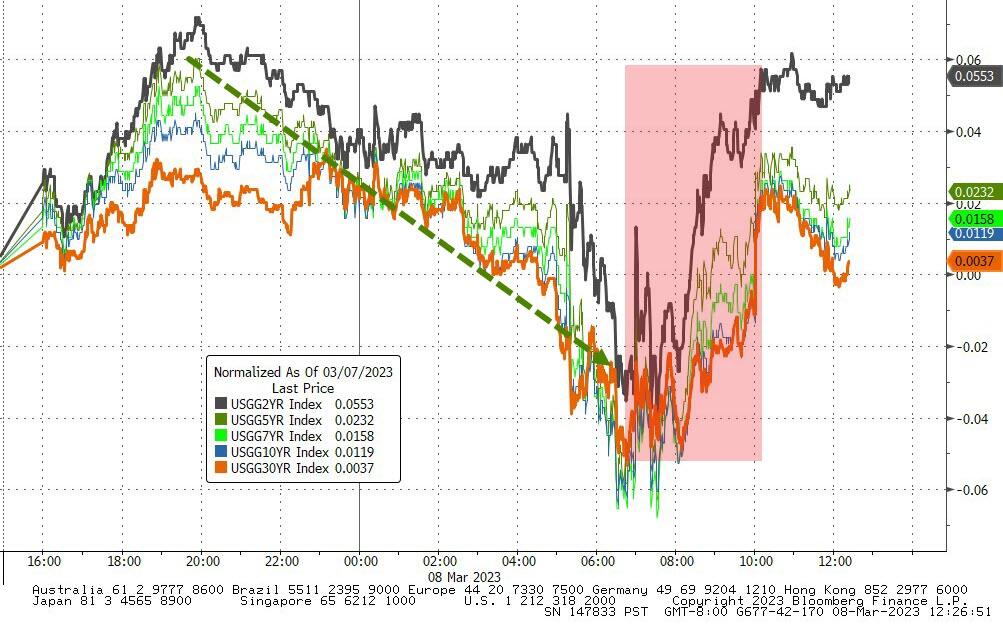

As a result, bond yields plunged and equity indexes, while up solidly in overnight trading, seesawed and ended the session close to their respective unchanged lines. This emergency action does not mean this crisis has been resolved, no, it has been merely halted, as the Fed is trying to ascertain, if other banks are experiencing a similar liquidity shortage (spoiler alert: yes, there are many more cockroaches).

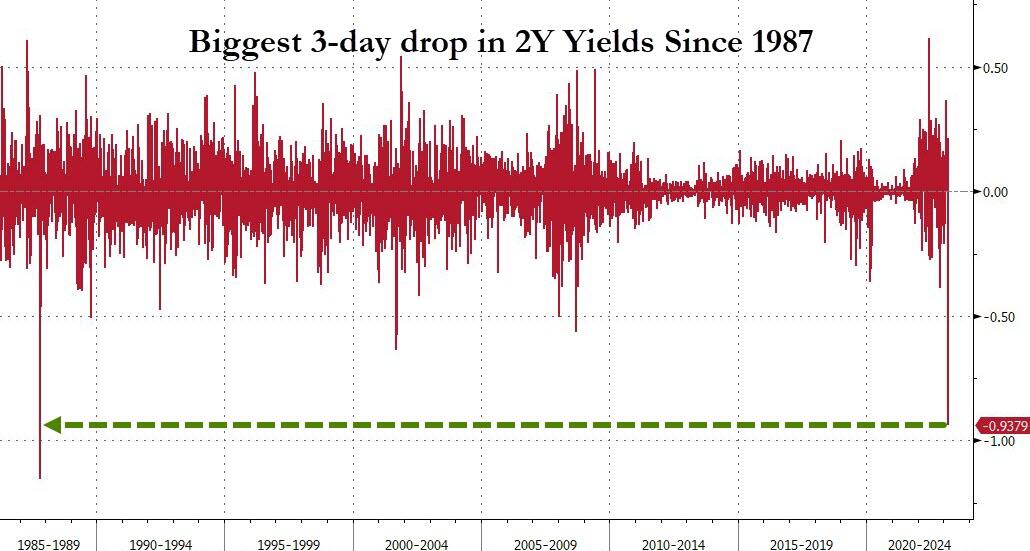

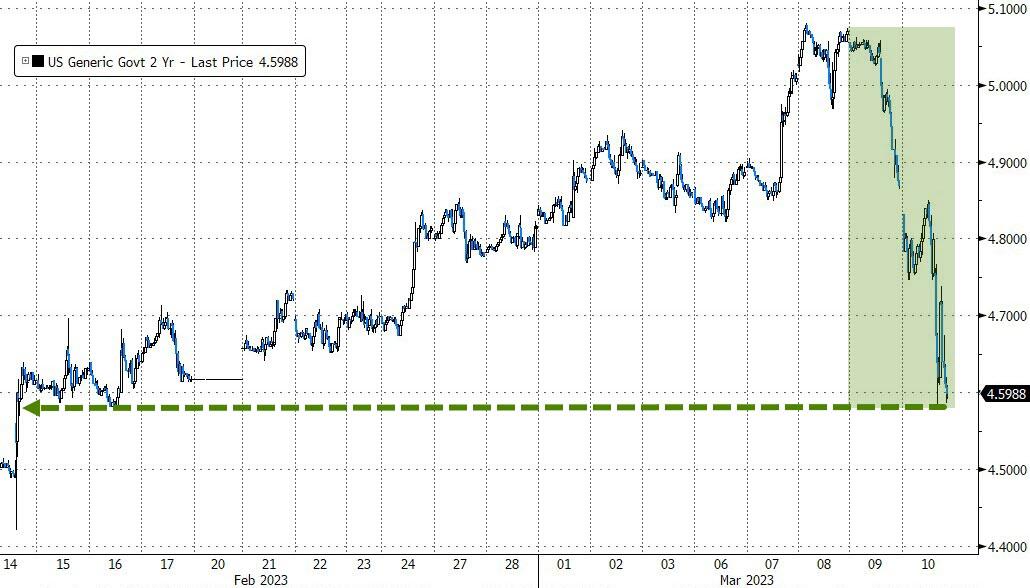

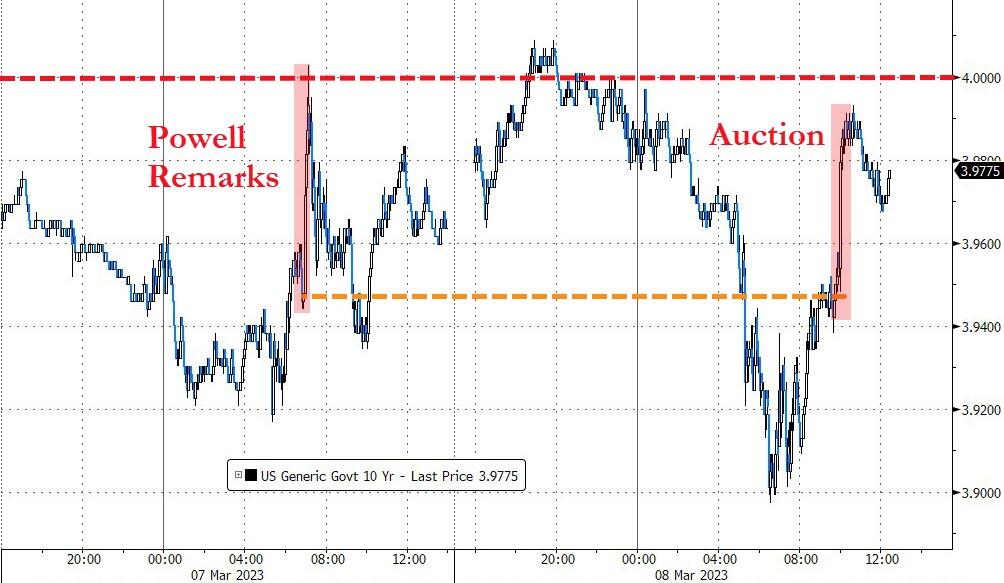

ZeroHedge highlighted that the 2-year yield plunged almost 100bps in the last three days to below 4%, which was its lowest since September 2022. This three-day drop in yield has been the biggest since “Black Monday” in 1987. Hmm…

Looking at the big picture, this event could very well mean the end of the Fed’s aggressive stance on interest rates, as rate hike expectations dropped sharply. The question remains now: “will they hike 0.25% at their next meeting, or will they pause?” For sure, the 0.5% hike option just died over the weekend.

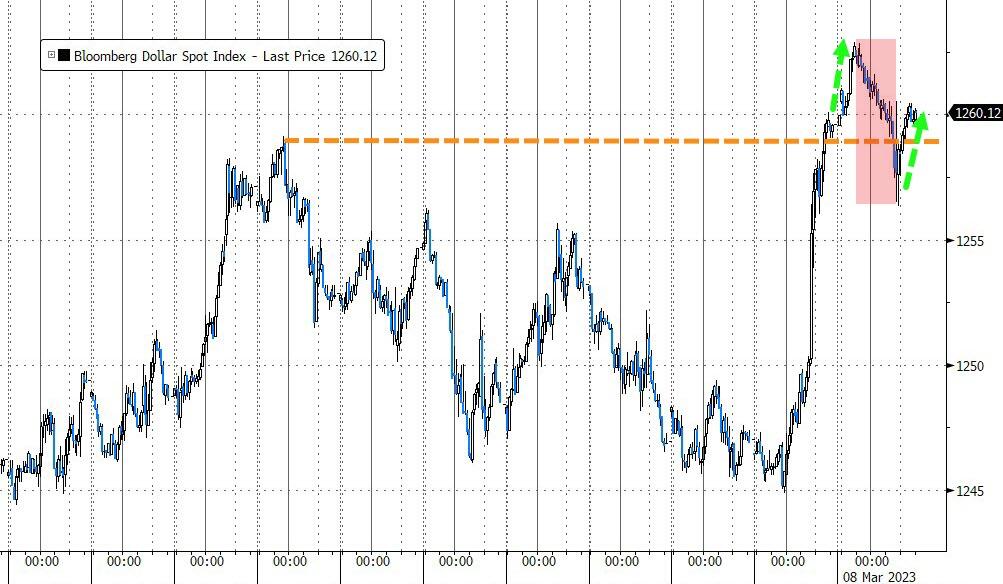

The US Dollar declined to three-week lows and, as you might expect in times of stress and uncertainty, Gold spiked above $1,900, a move of +2.66% for the day.

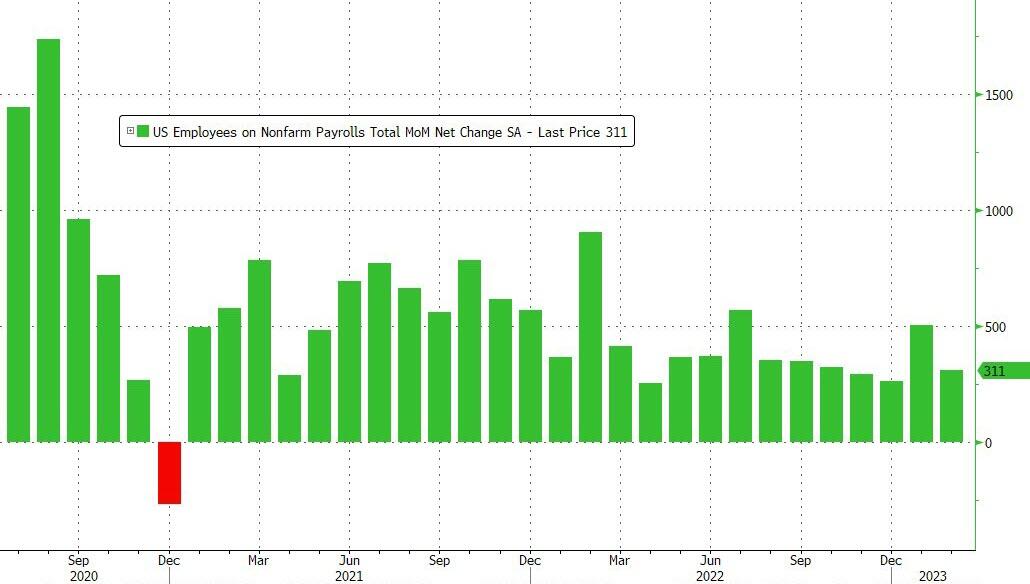

The fireworks are far from being over with the CPI, US retails sales, PPI, and housing data all on deck and waiting to make their mark on the markets.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}