I would like to extend my best wishes for a safe and happy Holiday season to you and your family. I will be taking a couple of days off but will be back on the regular posting schedule as of Monday.

No Load Fund/ETF Tracker updated through 12/23/2010

My latest No Load Fund/ETF Tracker has been posted at:

http://www.successful-investment.com/newsletter-archive.php

The major indexes managed to add another 1% to this month’s tally.

Our Trend Tracking Index (TTI) for domestic funds/ETFs has moved above its trend line (red) by +5.25% (last week +5.26%) and remains in bullish mode.

The international index has broken above its long-term trend line by +7.17% (last week +6.46%). A new Buy signal was triggered effective 9/7/10. If you decided to participate, be sure to use my recommended sell stop discipline.

[Click on charts to enlarge]

For more details, and the latest market commentary, as well as the updated No Load Fund/ETF Tracker StatSheet, please see the above link.

Snaking Higher

Right now, it appears that nothing can seem to end the persistent climbing of the major indexes. Yesterday was no exception as the markets ended up higher by a few points.

Energy and utilities provided a boost along with better-than-expected existing home sales for November. Of course, oil rising above $90/barrel for the first time in 2 years can hardly be a considered a positive. Neither can be an anemic GDP growth of 2.6% annualized for the quarter.

None of this appears to matter to the markets as confidence seems to have increased that 2011 will be a much better year economically speaking, which is expected to support higher stock prices.

The big neutralizer will be the stubbornly high unemployment rate despite stronger numbers in manufacturing along with elevated consumer spending. To me, real estate will continue its downward spiral for the simple reason that we’re stuck with this high unemployment number. After all, last time I checked, people buy houses and make mortgage payments with monies earned from real jobs and not from unemployment benefits.

How these positives and negatives will play out next year is anyone’s guess. Stay on top of the trends so you can easily spot reversals and take evasive action via your sell stops, which will help to protect your portfolio from extreme downside risk.

Holiday Cheers

Three things got the markets going early on yesterday. For one, there was some sigh of relief that dangers of another Korean shootout were laid to rest, at least for the time being. Second, rumor had it that N. Korea was showing willingness to let the United Nations inspectors monitor its nuclear program.

Third, but not least, in regards to the European debt crisis, Chinese Vice Premier Qishan said that the nation would “back measures aimed at stabilizing European counties struggling with debt.” At least for this moment in time, global issues were not on traders’ minds.

The markets inched higher and never looked back. My plan to liquidate one of our country ETFs did not work out as the emerging markets staged a nice rebound rally after seeming to have stalled for the past few weeks. For the time being, we will hold on to this position subject to our sell stop rules.

All major indexes have climbed to some pretty lofty levels when looking at the percentages they have moved above their respective trend lines. The S&P; 500, for example, has now reached a point that is 9.8% above its 200-day moving average. Last time this happened was in late April prior to the market heading sharply south and surrendering some 15% by early July.

I am not suggesting that a repeat is imminent, but I am saying that, based on emails from and phone calls with readers, some investor complacency has definitely set in again. It is for certain that the markets will correct again, we just don’t know the timing and magnitude of it.

Simply be aware and make sure you have your exit strategy planned and in place, so you don’t panic when the next correction strikes.

Leaving Blue Chips Behind

The Nasdaq quietly made a new 3-year high yesterday, but the Blue Chips were left behind as American Express and Boeing proved to be a drag on the Dow and prevented the index from climbing above the 11,500 level.

Interest rates were up slightly, as were gold and oil. The Euro slumped heavily vs. the Swiss Franc and also lost ground against the dollar as Moody’s downgraded some of the Irish debt.

This week will be a short one as all markets will be closed on Friday. I would expect activity to slow down quite a bit as we closer to Thursday. While I will not initiate any new positions, I will continue to track all exit points. Actually, one of our country fund holdings hit its sell stop right on the money today but failed to break through it.

I’ll look at the opening activity tomorrow and will, barring any sudden upside move, liquidate the position.

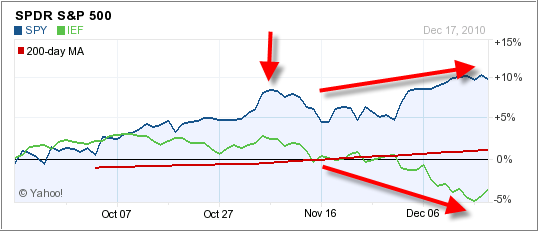

Going Separate Ways

Ever since the Fed implemented the latest round of Quantitative Easing early in November, stocks and bonds have gone in different directions. The 3-months chart above shows the SPY (S&P; 500) vs. IEF, the 7-10 Year Treasury ETF.

Both hit their respective tops simultaneously (vertical arrow), after which bonds reversed direction and slid as interest rates rose. The stock market, as represented by the S&P; 500, dropped initially as well, but found some support and managed to maintain upward momentum although at a slower pace.

Nevertheless, despite having crept higher, stocks seem to have stalled even as economic numbers improved. The concern now is if interest rates continue to head higher at the pace of the past few weeks, stocks will be affected negatively.

We’ve seen emerging markets not only stall as well but come sharply off their highs made in early November. Some are now within striking distance of their trailing sell stops.

Based on reader emails over the weekend on the topic of sell stop percentages, here are the numbers again as I use them in my advisor practice:

For widely diversified domestic and international mutual funds and ETFs, I apply trailing sell stops of 7%. For more volatile sector and country ETFs, I use 10%—both are soft sell stops. That simply means that they are based on closing prices only and not intra-day market activity.