Despite yesterday’s sharp sell-off, the High Volume ETFs were affected very little, at least if you measure it from last Wednesday’s report.

To clarify, High Volume (HV) ETFs are defined as those with an average daily volume of $10 million or higher.

These ETFs are generated from my selected list of 90 that I use in my advisor practice. It cuts out the “noise,” which simply means it eliminates those ETFs that I would never buy because of their volume limitations.

With the S&P 500 only having dropped 5 points since last Wednesday, the changes in this week’s HV ETF Cutline report were modest with several ETFs actually climbing up the ladder:

Vanguard Europe Pacific (VEA) from +14 to +20

Vanguard All World-Ex.-U.S. (VEU) from +13 to +19

South Africa (EZA) from -1 to +17

Diversified emerging markets (VWO) from +4 to +14

China (FXI) from -2 to +4

Russia (RSX) from -3 to +2

Bucking the trend, and following the market down during yesterday’s pullback, was PGF (Financials), which dropped from +8 to +3.

PGF (Financials) has been the only ETFs above the cutline with positive momentum numbers, including a low DD% number of -0.87%, for a while. Its 4-wk performance has dropped slightly into the negative (-0.05%), but if you are holding it, it’s still a buy, subject to its trailing sell stop.

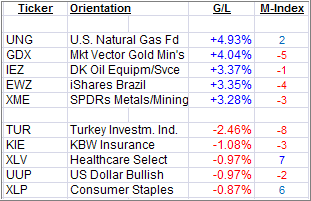

Take a look at the table:

Read More

{kind=link}