- Moving the market

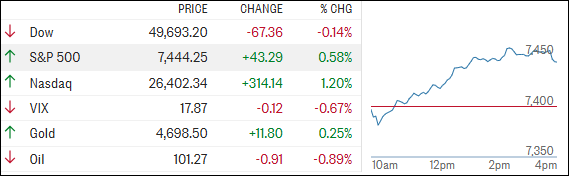

Markets were all over the place today after another hotter‑than‑expected inflation report sent bond yields racing to a 10‑month intraday high. The Dow slid early under the weight of rising rates, while strong gains in chip stocks helped keep the Nasdaq afloat.

{kind=link}

Tech once again led the charge, easily outperforming the rest of the market. Meanwhile, inflation fears—made worse by rising energy prices tied to escalating tensions in the Middle East—pressed on more rate‑sensitive sectors like retail and banking.

Just a day earlier, both the S&P 500 and Nasdaq had already backed off record highs following a hotter‑than‑expected consumer inflation print.

Then came Wednesday’s producer price index, and it didn’t help matters. PPI jumped 1.4% in April, the biggest monthly increase since March 2022 and far above the 0.5% economists were expecting. On an annual basis, wholesale inflation surged 6%, topping estimates and marking the strongest reading since late 2022.

For policymakers, this kind of data is about as unwelcome as it gets. No matter who’s in charge, inflation running this hot makes it tough to even talk about interest‑rate cuts anytime soon.

By the end of the session, the S&P 500 and Nasdaq managed to squeeze out modest gains, while the Dow climbed out of a deep early hole to finish roughly flat.

In commodities, oil kept ripping higher—up more than 8% over the past three sessions—as Middle East tensions simmered, and global stockpiles continued to shrink at a record pace.

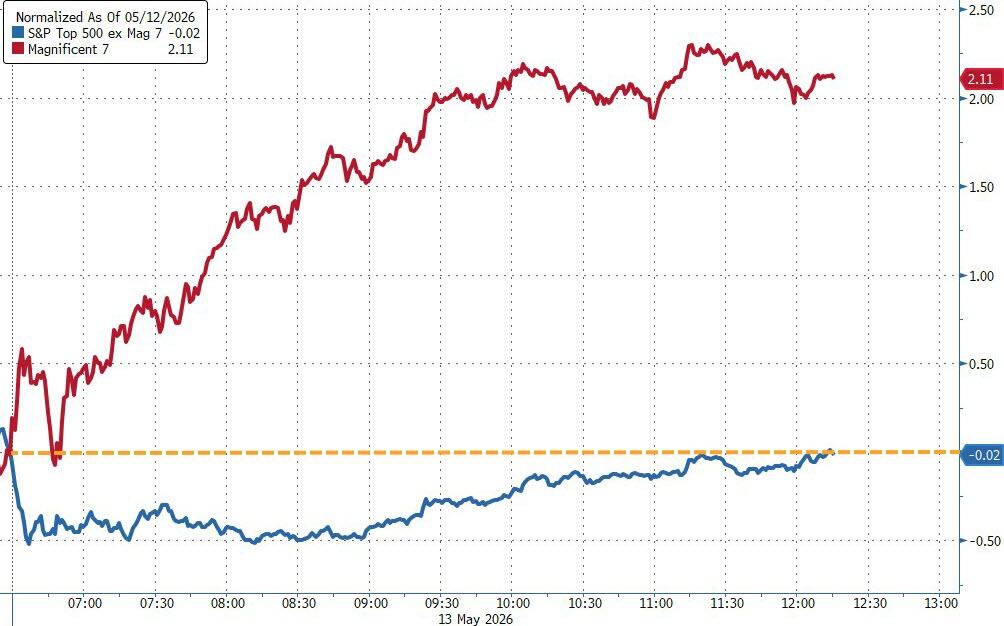

Big tech stocks also stood out, with the “Magnificent 7” once again crushing the rest of the S&P 500.

{kind=link}

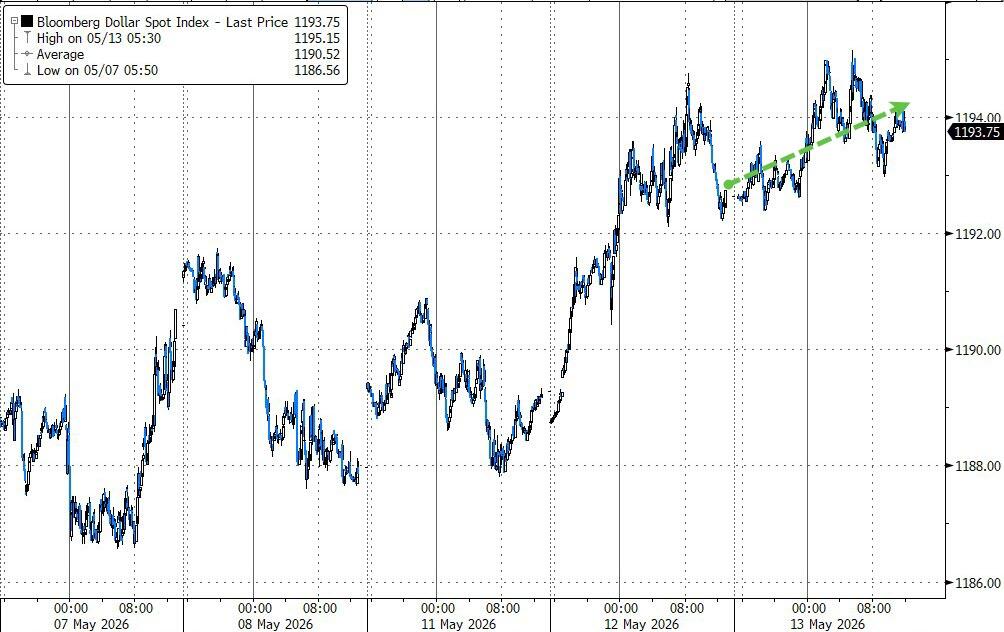

The dollar drifted slightly, while gold followed along and found support near $4,700.

{kind=link}

{kind=link}

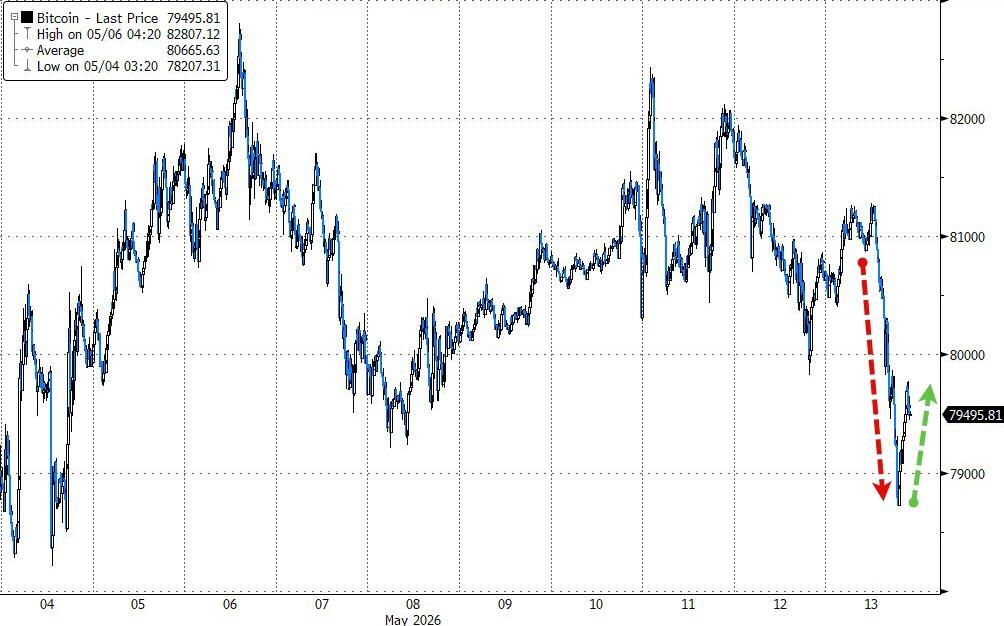

Silver stayed red‑hot, rising for a seventh straight session, and topping $89 for the first time in two months. Bitcoin pulled back but found solid footing around $79,000.

{kind=link}

{kind=link}

Inflation and global rates remain the main drivers of market action—but it’s really the speed of the move in bond yields that matters most. So, when does that finally start to hit stocks in a meaningful way?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Despite rising wholesale inflation and no encouraging headlines out of the Middle East, the major indexes managed to rebound from a weak open.

By the close, only the Dow fell short of getting back above its unchanged line, while the rest of the market stabilized.

Metals were mixed overall, with silver once again standing out as the only one to finish in the green.

Our TTIs split paths as well — the international TTI moved higher, while the domestic version slipped modestly.

This is how we closed 05/13/2026:

Domestic TTI: +5.31% above its M/A (prior close +5.77%)—Buy signal effective 5/20/25.

International TTI: +10.00% above its M/A (prior close +9.53%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli