- Moving the market

The major indexes opened slightly higher after wrapping up a solid winning week on Wall Street, even as oil prices pushed up following President Trump’s rejection of Iran’s latest proposal to end the war.

Iran had sent a new counteroffer to U.S. negotiators that called for ending the conflict on all fronts and lifting sanctions on Tehran, according to semi‑official Tasnim news agency. Trump wasted no time responding, calling the proposal “TOTALLY UNACCEPTABLE!” in a Truth Social post.

Even so, many traders seem willing to look past the noise. The prevailing view is that, despite the war and the oil shock, the broader U.S. economy is still holding up better than most people expected.

That mindset showed up again today. Even after Trump later said the ceasefire deal was “on life support,” and despite rising oil prices and higher bond yields, stocks managed to grind out another round of modest gains. Small caps led the way, fueled by a sizeable short squeeze.

{kind=link}

{kind=link}

The S&P 500 logged its fifth consecutive intraday record high and its 13th intraday record this month, as one of the strongest earnings seasons in years continued to overpower the latest round of Middle East jawboning.

Leadership was broader than usual. The Magnificent Seven underperformed the S&P 493, the dollar edged slightly higher, and gold posted a modest gain.

{kind=link}

{kind=link}

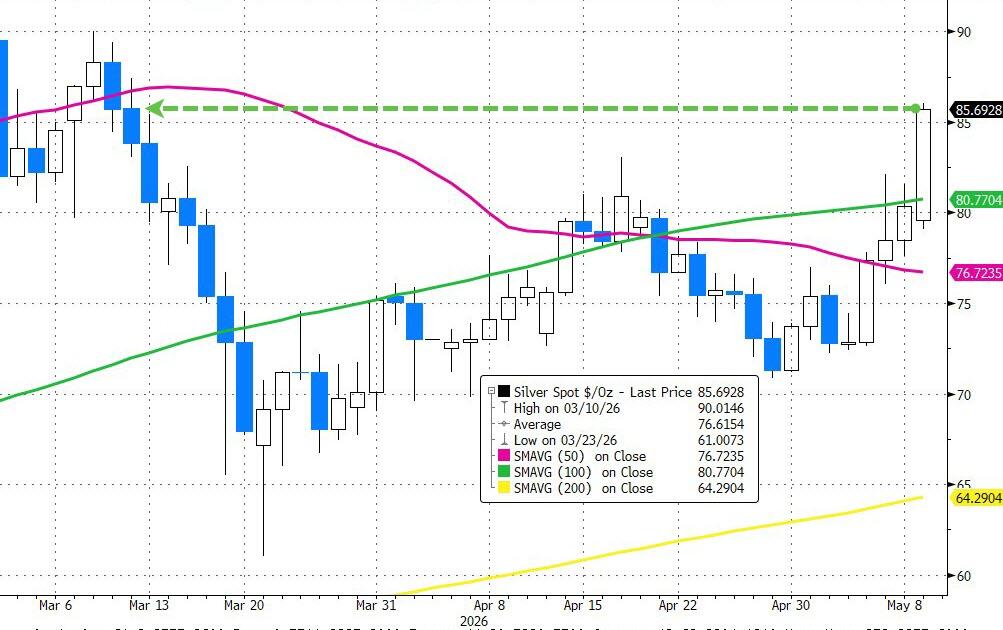

Silver stole the spotlight, extending its rally to a fifth straight day and jumping 6.8%, its highest level in two months. Bitcoin chopped around but eventually found its footing, closing above $82,000.

{kind=link}

{kind=link}

Once again, the market seemed largely disconnected from events on the ground in the Middle East. With both sides under pressure to strike a deal that still remains elusive, it’s hard not to wonder: how long will equities continue to look past the risks?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Early positive momentum carried through the session, lifting not just equities but the metals as well, with silver standing out as the top performer.

On the equity side, it was a tale of two markets: Consumer Discretionary funds took a beating, while Value ETFs continued to show impressive resilience and strength.

Our TTIs diverged. The domestic TTI largely treaded water, while the international TTI pushed higher, pointing to better momentum outside the U.S. for now.

This is how we closed 05/11/2026:

Domestic TTI: +5.86% above its M/A (prior close +5.92%)—Buy signal effective 5/20/25.

International TTI: +10.02% above its M/A (prior close +9.52%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli