ETF Tracker StatSheet

You can view the latest version here.

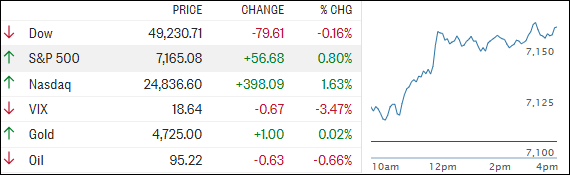

OPTIMISM WINS THE DAY AS TECH AND INTEL STEAL THE SHOW

[Chart courtesy of MarketWatch.com]

- Moving the market

The tech sector led the way this morning after traders got a hopeful signal that peace talks between the U.S. and Iran could soon take place in Pakistan.

Reports cited a Pakistani government official saying Iranian Foreign Minister Abbas Araghchi is expected to arrive in Islamabad on Friday evening, raising expectations that negotiations between the two sides may follow.

Oil prices, which had been rallying, lost some steam on the news.

That optimism comes on the heels of President Trump’s announcement Thursday that Israel and Lebanon agreed to extend their ceasefire by another three weeks, following meetings at the White House with senior U.S. officials.

Taken together, the headlines reinforced the idea—at least for now—that tensions may be cooling rather than escalating.

Given Thursday’s pullback from all‑time highs in both the S&P 500 and Nasdaq, Middle East developments are clearly still capable of moving markets. Even so, traders are trying to look past the geopolitical noise and refocus on corporate earnings.

Today, optimism won out. Stocks surged to fresh record highs as markets latched onto a new wave of “promising” headlines from the U.S., largely brushing aside Iran’s more cautious responses.

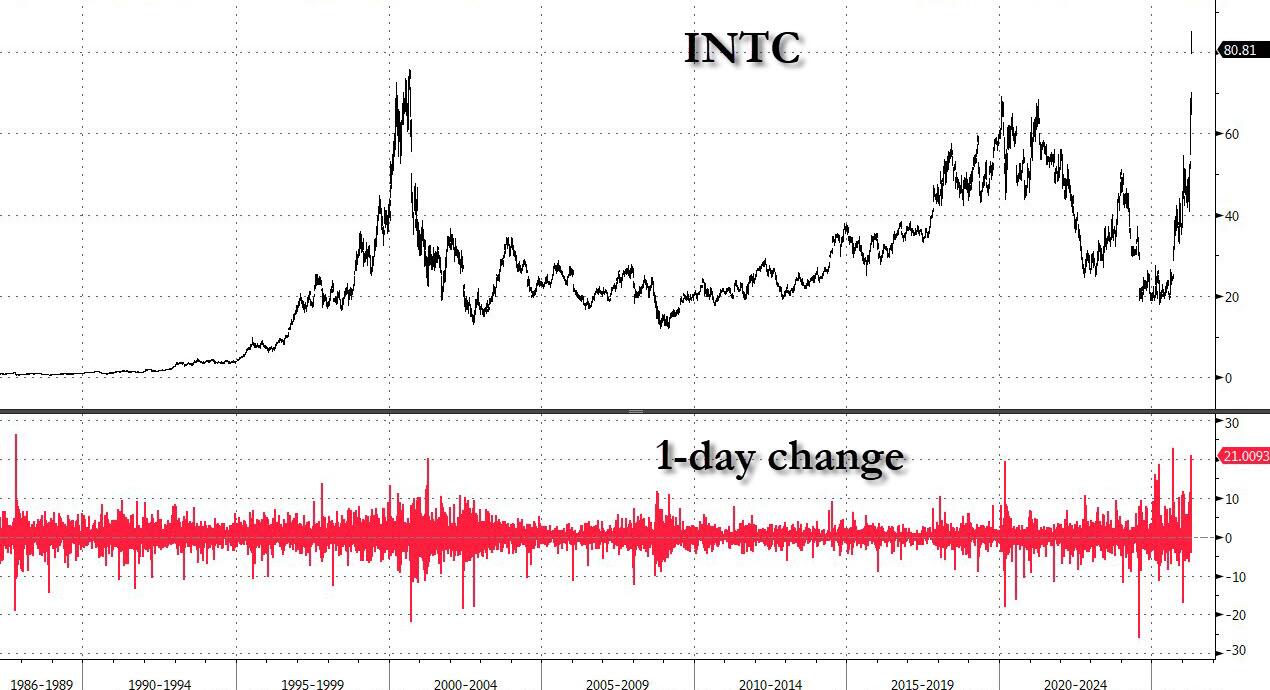

Earnings also played a major role. Intel delivered a blowout report, sending its stock up as much as 28% at one point—the biggest one‑day move since Black Monday in 1987—before settling back to a still‑impressive 21% gain. Along the way, Intel surpassed its prior record high from the peak of the dot‑com bubble.

{kind=link}

In other markets, bond yields fell after a Justice Department decision involving Powell appeared to clear a path for Kevin Warsh to become the next Fed chair, prompting traders to boost bets on future rate cuts.

Gold and silver ETFs moved modestly higher, while copper and Bitcoin largely treaded water.

With Middle East headlines still in play and next week shaping up as the busiest stretch of earnings season—with 36% of the S&P 500 reporting—traders now face a familiar question:

Can strong earnings and hopes of de‑escalation keep this rally going, or are markets getting ahead of themselves?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

The tech rally kept rolling, with the Nasdaq posting another winning session, followed closely by the S&P 500.

The broader market didn’t join the party, though. Our Domestic Trend Tracking Indicator slipped slightly, while the international TTI came off its highs as well.

Metal ETFs moved higher on the day, while Bitcoin largely went nowhere, treading water as risk appetite stayed focused on equities.

This is how we closed 04/24/2026:

Domestic TTI: +5.51% above its M/A (prior close +5.96%)—Buy signal effective 5/20/25.

International TTI: +7.38% above its M/A (prior close +7.54%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli