[Chart courtesy of MarketWatch.com]

- Moving the markets

Traders had a lot on their plate on Monday: a flood of corporate earnings reports, rising bond yields, and simmering tensions in the Middle East. But they chose to focus on the positive and pushed stocks higher.

{kind=link}

The S&P 500 rose by about 1%, but it still faces a hurdle: the top of its downward trend channel that started in July. Could it break through this barrier and end the bear market rally? It needs another 0.75% boost to find out.

This week, 11% of the S&P 500 companies will report their earnings. Some big names include Johnson & Johnson, Bank of America, Netflix, and Tesla. Will they beat expectations or disappoint the market?

Wall Street traders are not relaxing yet. They know that volatility could spike by the end of the year, as bond yields and oil prices climb, inflation stays high, and conflict brews in the Middle East.

But they are also hopeful that earnings and the Fed will save the day. Powell will talk about interest rates and policy outlook on Thursday at the Economic Club in New York. Will he be dovish or hawkish? Will he taper its bond-buying program or keep it steady?

As for our Domestic Trend Tracking Index (TTI-section 3), it is still in bearish territory, meaning that the overall market trend is down. We are waiting for a signal to change our portfolio allocation.

In the meantime, trading in equities may be rangebound. The Middle East conflict is like a chess game that could turn violent at any moment. But earnings are like a ray of sunshine that could brighten up the market.

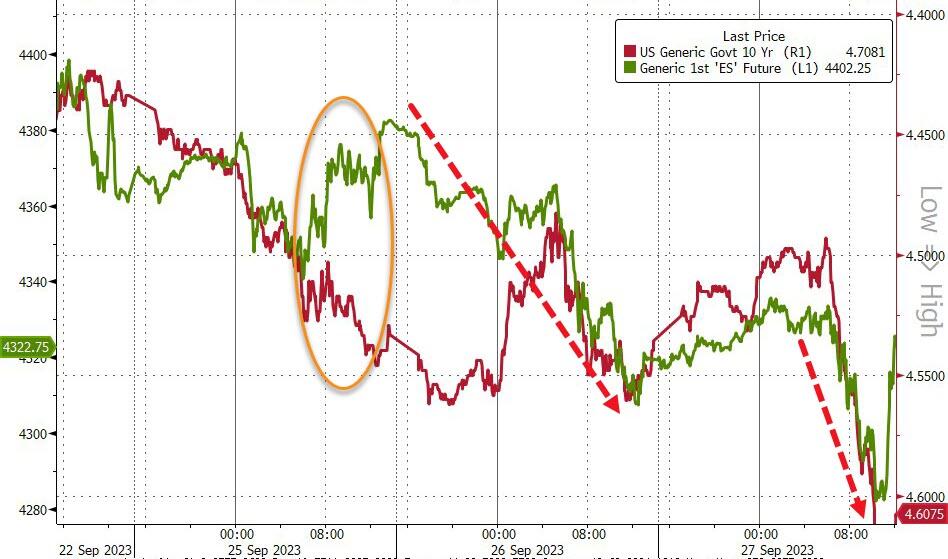

For now, traders are ignoring the dark clouds and enjoying the sunny day. They are driving equities higher, even as bond yields rise. As ZeroHedge showed in this chart, we have seen this movie before, and it did not have a happy ending.

{kind=link}

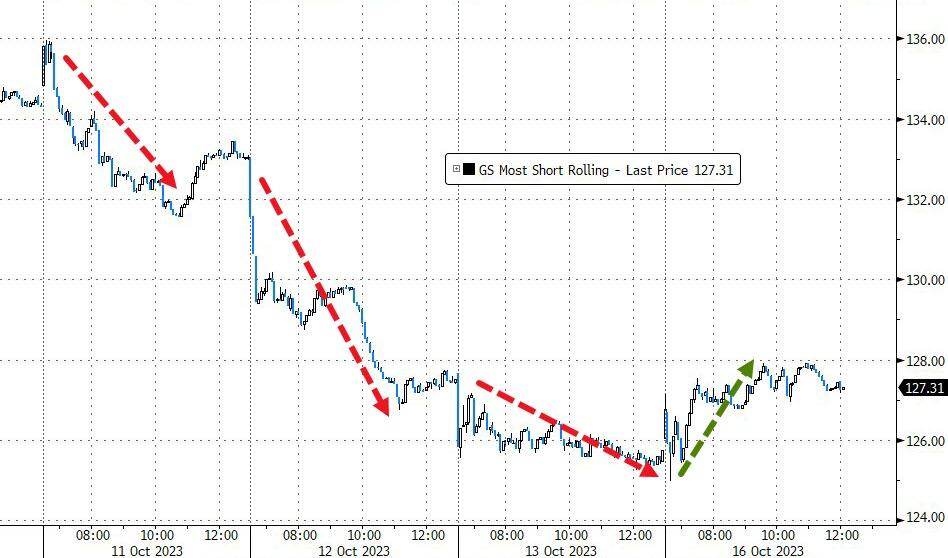

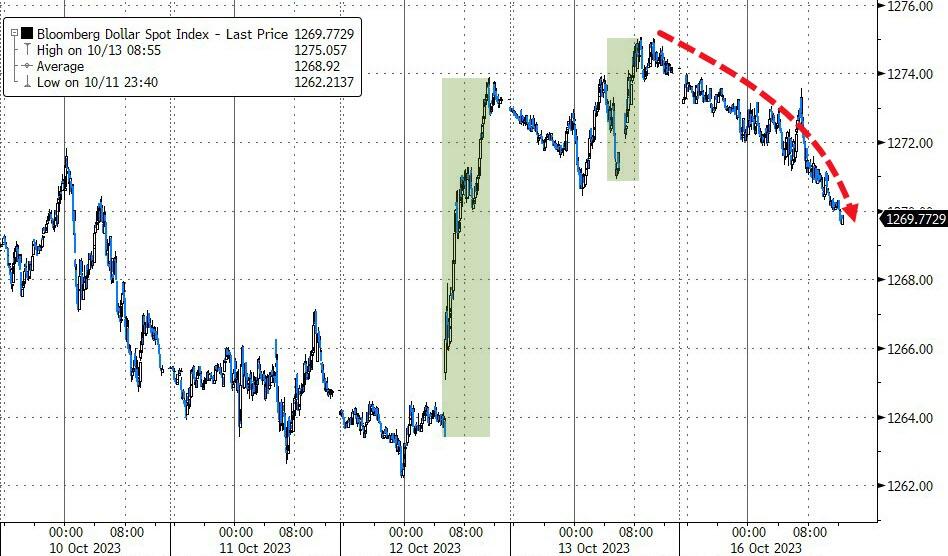

The short squeeze strategy finally worked today, after failing for three days. The dollar fell, crude oil slid, and gold paused after soaring last week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This week, we will also get some economic data on retail sales and housing. And we will hear from several Fed speakers, including Powell. Will they sing in harmony or discord?

2. “Buy” Cycle (12/1/22 to 9/21/2023)

The current Domestic Buy cycle began on December 1, 2022, and concluded on September 21, 2023, at which time we liquidated our holdings in “broadly diversified domestic ETFs and mutual funds”.

Our International TTI has now dipped firmly below its long-term trend line, thereby signaling the end of its current Buy cycle effective 10/3/23.

We have kept some selected sector funds. To make informed investment decisions based on your risk tolerance, you can refer to my Thursday StatSheet and Saturday’s “ETFs on the Cutline” report.

Considering the current turbulent times, it is prudent for conservative investors to remain in money market funds—not bond funds—on the sidelines.

3. Trend Tracking Indexes (TTIs)

Traders were optimistic today, despite the rising bond yields and the escalating tensions in the Middle East. However, they shrugged off the risk of higher borrowing costs and focused on the positive earnings reports from major companies. The war drums of the Middle East also did not dampen the market mood, as the US and its allies tried to resolve the conflict diplomatically.

Our Trend Tracking Indexes (TTIs) retreated slightly, but they are still in bearish territory, meaning that the overall market trend is downward. I will continue to monitor the situation and will adjust our portfolios once we return to a bullish environment.

This is how we closed 10/16/2023:

Domestic TTI: -2.20% below its M/A (prior close –3.40%)—Sell signal effective 9/22/2023.

International TTI: -0.58% below its M/A (prior close -1.31%)—Sell signal effective 10/3/2023.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli