- Moving the markets

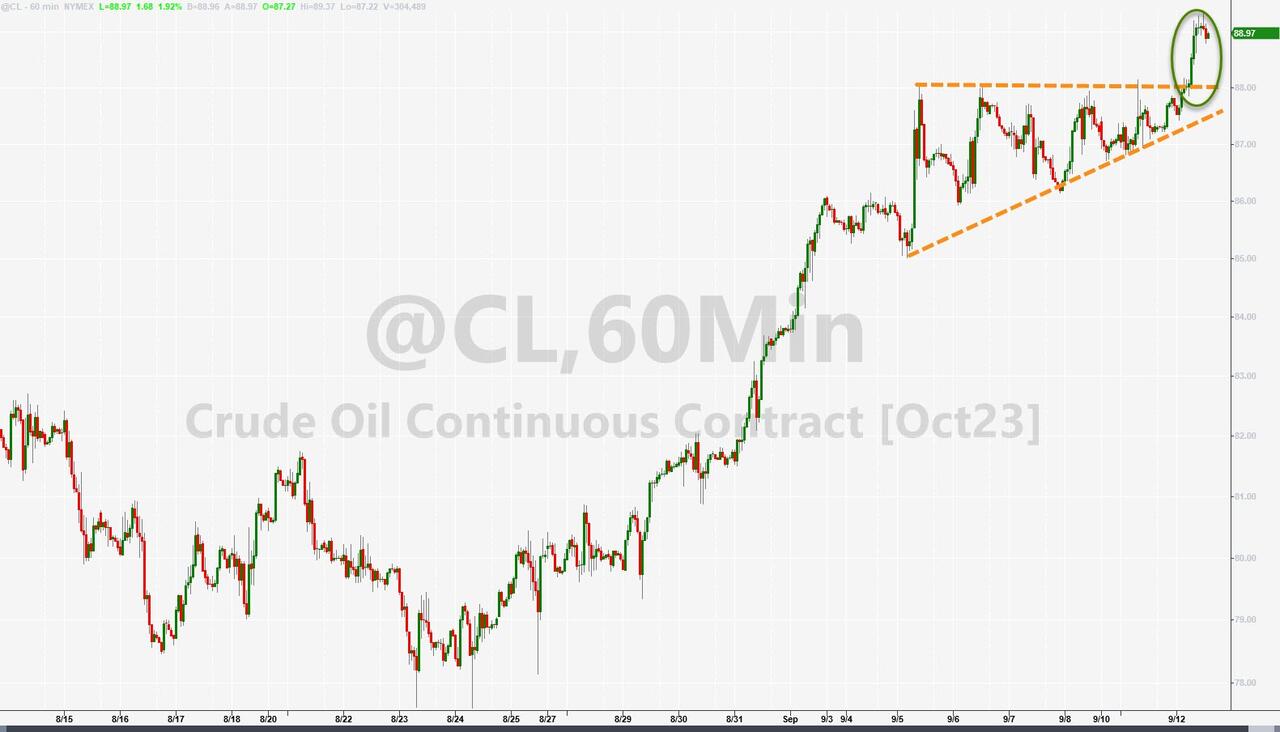

Oil prices soared to their highest level in seven years, making everyone wonder if they should invest in electric cars or bicycles. The rising cost of energy spooked the stock market, which fell for the second day in a row.

{kind=link}

The major indexes dipped below their 50-day moving averages, a sign of weakness in the market trend. Oracle was the biggest loser of the day, plunging 13% after disappointing investors with its revenue and guidance. The cloud computing giant faced stiff competition from other tech titans, such as Amazon, Alphabet and Microsoft, which also dropped.

{kind=link}

Apple fans were eagerly awaiting the launch of the new iPhone model, but the stock was down ahead of the event. Maybe they were hoping for a cheaper phone or a free charger.

{kind=link}

Investors were also nervous about the inflation data coming out later this week. The consumer price index (CPI) will be released tomorrow, followed by the producer price index (PPI) on Thursday. These reports measure the changes in the prices of goods and services and are closely watched by the Federal Reserve and the market.

High inflation could force the Fed to raise interest rates sooner than expected, which could hurt the economy and the stock market. Analysts had a lot to chew on this week, with a menu of economic reports to digest.

But if any of those reports come in much worse than expected, they might lose their appetite and throw up. That would not be good for the market either.

On the bright side, banks managed to crawl out of the hole they dug themselves into, with the banking index (KRE) rising slightly. However, they gave up some of their gains at the end of the day, showing a lack of confidence.

{kind=link}

Bond yields were mixed, with the 2-year yield climbing above 5%. The US dollar bounced around but ended up slightly higher. Gold slipped, as investors preferred cash over shiny metal.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

With all eyes on tomorrow’s CPI report, inflation expectations are surging. Does that mean a worse than expected CPI reading will ruin the party? Or will it be a non-event that will allow the market to resume its uptrend?

{kind=link}

Tune in tomorrow to find out!

2. “Buy” Cycle Suggestions

The current Buy cycle began on 12/1/2022, and I gave you some ETF tips based on my StatSheet back then. But if you joined me later, you might want to check out the latest StatSheet, which I update and post every Thursday at 6:30 pm PST.

You should also think about how much risk you can handle when picking your ETFs. If you are more cautious, you might want to go for the ones in the middle of the M-Index rankings. And if you don’t want to go all in, you can start with a 33% exposure and see how it goes.

We are in a crazy time, with the economy going downhill and some earnings taking a hit. That will eventually drag down stock prices too. So, in my advisor’s practice, we are looking for some value, growth and dividend ETFs that can weather the storm. And of course, gold is always a good friend.

Whatever you invest in, don’t forget to use a trailing sell stop of 8-12% to protect yourself from big losses.

3. Trend Tracking Indexes (TTIs)

The energy sector led the market gains, as oil prices surged to their highest level in seven years. However, the overall market sentiment was cautious, as investors awaited the release of the Consumer Price Index (CPI) data tomorrow.

The CPI measures the changes in the prices of goods and services and is a key indicator of inflation. High inflation could prompt the Federal Reserve to tighten its monetary policy sooner than expected, which could hurt the stock market. Therefore, trading volume was low, and most sectors closed lower.

Our TTIs also edged down slightly.

This is how we closed 09/12/2023:

Domestic TTI: +1.33% above its M/A (prior close +1.46%)—Buy signal effective 12/1/2022.

International TTI: +3.50% above its M/A (prior close +3.58%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli